Felony level credit card theft occurs when the value of the stolen goods or services exceeds a certain threshold, often $1,000 or more, depending on state or federal laws. This type of crime involves knowingly using counterfeit, stolen, or fraudulently obtained credit cards to acquire money or property. It is classified as a felony because of the significant financial harm and legal consequences involved.

The severity of felony charges often results in harsher penalties, including imprisonment, hefty fines, and restitution requirements. Credit card theft at this level can be prosecuted either at the state or federal level, with interstate or international cases typically treated as federal offenses, which carry the possibility of longer prison terms.

Understanding what constitutes felony credit card theft helps clarify why these cases are taken seriously by the legal system. Being aware of the distinctions between misdemeanor and felony charges can influence defense strategies and potential outcomes.

Definition of Felony Level Credit Card Theft

Felony level credit card theft involves serious offenses that typically exceed a specific monetary threshold or involve aggravating factors such as interstate commerce or repeated offenses. It is distinguished by the severity of the crime and the resulting legal consequences, which are more severe than misdemeanors.

Felony Versus Misdemeanor Credit Card Offenses

The distinction between felony and misdemeanor credit card offenses often depends on the amount involved and the jurisdiction. Generally, theft of credit cards or fraudulent use under a certain limit is classified as a misdemeanor, while offenses exceeding thresholds—commonly $950 or $1,000—are felonies.

Felony charges also arise if the fraud involves government benefits, interstate or international commerce, or if it is tied to other crimes like identity theft. Felony convictions carry harsher penalties, including longer imprisonment terms, higher fines, and lasting impacts such as difficulty obtaining housing and employment.

Elements of Felony Credit Card Theft

To prove felony credit card theft, prosecutors must show intent to defraud using a stolen or counterfeit card. This includes unauthorized possession, use, or transfer of credit card information to obtain money, goods, or services.

Key elements include:

- Knowing use of a stolen or fraudulent card

- Value of property or services obtained exceeding felony limits

- Intent to deceive or cause financial loss

These elements must be clearly demonstrated for felony-level charges to apply, differentiating them from lesser offenses where intent or value may be lower.

Common Legal Terminology in Credit Card Cases

Terms commonly encountered in felony credit card theft cases include:

- Credit Card Abuse: Unauthorized use of a card or account to obtain goods or funds.

- Grand Theft: Theft exceeding a specified value, qualifying as a felony.

- Identity Theft: Using another’s personal information, often linked with credit card fraud.

- Restitution: Court-ordered repayment to victims for financial losses caused by the crime.

Understanding these terms helps clarify the charges and potential consequences associated with credit card abuse charges, especially for first-time offenders facing felony-level accusations.

How Felony Credit Card Theft Is Committed

Felony credit card theft involves stealing or using credit card information in ways that surpass minor infractions in value or method. These crimes can be carried out through both physical and digital means, often involving sophisticated tools or organized efforts. The stolen data is then exploited through various fraudulent uses or altered to deceive institutions and individuals.

Physical Versus Digital Theft Methods

Physical theft includes stealing actual credit cards from wallets, mailboxes, or retail locations. Skimming devices attached to ATMs or gas pumps capture card data during legitimate transactions. These stolen cards or details then serve as the basis for further fraudulent activity.

Digital methods have grown more complex. Hackers harvest credit card information by breaching databases or purchasing data on credit card dump sites. These online markets trade stolen card numbers, expiration dates, and security codes, often enabling organized crime operations. Cybercriminals also use proxies bought with stolen cards to mask their IP addresses and commit fraud anonymously.

Phishing attacks trick victims into revealing their credit card details, which are then exploited. These digital techniques allow thieves to execute transactions remotely without physical possession of the card.

Use of Stolen Credit Cards and Information

Once credit card data is stolen, it is commonly used to make unauthorized purchases, withdraw cash, or purchase goods that can be resold easily. Sophisticated criminals may exploit soft declined versus hard declined credit card in sales knowledge to understand when transactions will be accepted or rejected, thereby reducing their chances of immediate detection.

Many instances involve testing small transaction amounts before proceeding to larger purchases. Another approach is using stolen credentials to buy proxy with credit card to obfuscate the origin of transactions, complicating investigations.

Merchants and banks may rely on credit card reconciliation software to identify inconsistencies in purchases or account activity, but fraudsters continuously evolve their methods to bypass these controls.

Forgery, Fraud, and Related Crimes

Forgery plays a role when thieves alter physical cards or create fake cards using stolen information. They might duplicate card magnetic strips or embed counterfeit chips to deceive payment terminals.

Fraud extends beyond simple unauthorized use. Identity theft often accompanies credit card theft, where criminals impersonate victims to open new accounts or take out loans.

Related crimes include the use of social engineering tactics to gain further access, and sometimes burglary or hacking to obtain card details. Theft over a certain monetary threshold typically elevates the offense to felony, especially if it involves government programs or interstate transactions.

Credit card theft may also coincide with other criminal activities, like money laundering using cards bought from dump sites or manipulated through proxy servers to cover tracks.

Legal Criteria and Thresholds for Felony Charges

Felony-level credit card theft is determined by specific legal standards that focus on the value of stolen property and certain aggravating factors. These standards vary by state, with each jurisdiction setting distinct monetary thresholds and statutes guiding prosecution.

Monetary Value Requirements

The central factor for felony credit card theft is the total value of the fraud or stolen goods charged to the card. Most states set a minimum dollar amount that, when exceeded, elevates the offense to a felony. For example, in many states, theft involving amounts over $1,000 to $2,500 qualifies as felony theft.

Because inflation impacts these thresholds, some jurisdictions, such as Georgia, have ongoing discussions about adjusting the monetary level to reflect economic changes. The statute of limitations for credit card debt in Georgia varies but often affects the time frame for prosecuting such cases.

If the fraudulent charges fall below the state’s threshold, charges may be filed as misdemeanors instead, carrying lighter penalties.

Aggravating Factors in Felony Charges

Certain conditions can escalate credit card theft to a felony regardless of the monetary value. These factors include using stolen cards repeatedly, impersonating another person, or exploiting vulnerable victims.

Crimes committed with burglary tools or involving large-scale schemes often result in felony charges. Prosecutors might also consider the offender’s criminal history when deciding the level of the charge.

In some cases, specific crimes such as the “good sportsman charge” on a credit card, which involves unauthorized use for sporting or recreational events, could affect the severity of charges depending on state laws.

Relevant Statutes by State

Each state enforces credit card theft laws differently, with unique statutes specifying theft definitions, penalties, and thresholds. For example, Georgia’s statutes outline penalties for credit card fraud and theft under its criminal code, often tied to property value and intent.

Other states have distinct guidelines reflecting local policies and economic conditions. Legal practitioners must consult state-specific laws to understand the exact felony theft criteria.

Cases like Christell White Paterson’s have highlighted how individual circumstances and regional statutes influence credit card theft charges and prosecution outcomes. This underscores the importance of knowing state laws precisely.

Consequences and Sentencing for Felony Credit Card Theft

Felony credit card theft involves serious legal consequences that vary by jurisdiction but usually include prison time, fines, and financial restitution. The impact can extend beyond sentencing to affect credit records and future employment opportunities.

Range of Sentences and Penalties

Felony credit card theft penalties typically range from several years to up to 20 years in prison. The specific sentence depends on factors like the amount stolen, prior convictions, and whether the crime involved interstate commerce or large-scale fraud. Some states set mandatory minimum sentences.

Fines for felony offenses can range from thousands to tens of thousands of dollars. In federal cases, sentences can be harsher, especially when the stolen value exceeds $1,000. Jail time combined with fines is common, and courts often impose probation after release.

Restitution and Fines

Victims must be reimbursed for their losses, so courts usually order defendants to pay restitution. This can cover the full amount stolen, along with additional fees related to investigation and legal costs.

Credit card companies and banks rarely place liens on a defendant’s house directly. However, unpaid fines or restitution may lead to civil judgments, which could result in liens or wage garnishments to recoup funds.

Fines imposed can vary widely, from $1,000 to over $25,000, depending on jurisdiction and case severity. Failure to pay fines and restitution may result in extended probation or additional penalties.

Collateral Effects on Credit and Employment

A felony conviction for credit card theft severely damages credit scores and financial trustworthiness. The criminal record itself is accessible to employers, making it difficult to obtain jobs in finance, retail, or positions requiring background checks.

Lenders might deny credit applications due to the theft record, limiting future financial opportunities. Certain professions legally bar individuals with felony convictions, which restricts career advancement and income potential.

Even after sentences are served, enduring damage to reputation and credit can last for years. This hidden cost is often overlooked but poses a substantial barrier to rehabilitation.

Investigation and Criminal Prosecution Process

The investigation into felony-level credit card theft involves detailed evidence collection and cooperation between multiple parties. Law enforcement agencies and credit card companies work together to identify offenders. The prosecution focuses on establishing intent, scope, and financial impact, while defense strategies often challenge the evidence or procedures used.

Evidence Gathering in Credit Card Theft Cases

Evidence in these cases usually includes transaction records, surveillance footage, and electronic data logs. Investigators look for unauthorized purchases or unusual patterns tied to the suspect’s identity. They also obtain bank statements and communication records to track fraudulent activity.

Physical evidence, such as stolen cards or devices used in cloning, may be seized. Digital forensics often plays a key role, uncovering deleted or hidden data on computers and phones.

Establishing a clear connection between the accused and the fraudulent acts is crucial for prosecution.

Roles of Law Enforcement and Credit Card Companies

Law enforcement, including the FBI for interstate or international cases, leads the criminal investigation. They gather evidence, interview witnesses, and coordinate with prosecutors.

Credit card companies conduct internal fraud investigations. They track disputed charges, flag suspicious transactions, and provide records to authorities. Their cooperation is essential in tracing stolen funds and validating claims.

Together, these entities share information to build a comprehensive case. This partnership strengthens the likelihood of successful prosecution.

Defense Strategies Against Felony Charges

Defense attorneys may question the legitimacy of evidence, such as challenging the authenticity of transaction data or surveillance footage. They might argue mistaken identity or question whether authorization was given.

Procedural errors during the investigation, like unlawful searches or failure to follow proper chain-of-custody protocols, can be grounds to suppress evidence.

In some cases, defendants seek reduced charges or alternative sentences by negotiating based on the offender’s history and the fraud’s financial scale.

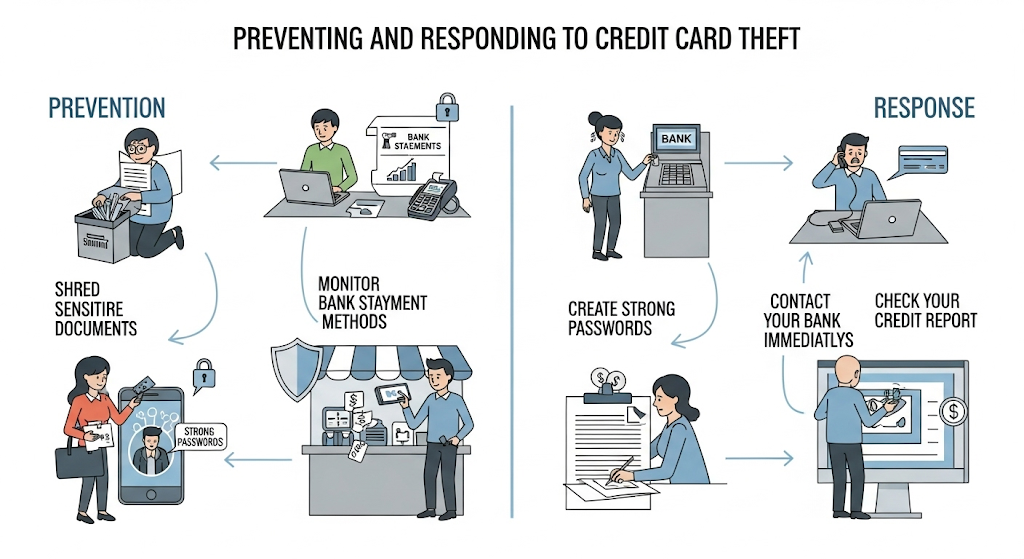

Preventing and Responding to Credit Card Theft

Effective prevention and timely response reduce the risks and consequences of credit card theft. Securing cards properly, quick reporting of compromised cards, and following recovery steps are essential actions to protect finances and credit.

Proper Security Measures for Cards and Accounts

Protecting debit and credit cards starts with strict control over physical cards. Cards should never be shared or left unattended. Using strong, unique passwords and enabling two-factor authentication on bank and credit accounts adds extra security layers.

Debit cards typically require a PIN for transactions, adding protection against unauthorized use. Keeping this PIN confidential is necessary to prevent theft.

It is advisable to regularly monitor account statements and transaction alerts. Many banks offer immediate alerts for suspicious activity, helping catch fraud early.

Lastly, avoid using unsecured public Wi-Fi for financial transactions. Instead, choose private networks or secure VPNs for online banking.

Reporting Stolen or Compromised Cards

Once a card is lost or suspected compromised, the owner must immediately contact the card issuer or bank. Prompt reporting limits unauthorized charges and liability.

Most banks provide 24/7 fraud hotlines and may block the account quickly upon notification. Cardholders often receive a replacement card with a new number.

It’s also important to file a police report if theft is involved and notify credit bureaus to prevent identity misuse.

Keeping records of the report and communication assists in disputing fraudulent charges if necessary.

Recovery Steps for Victims

Victims of credit card theft should review their account activity thoroughly to identify unauthorized transactions. Promptly disputing incorrect charges with the card issuer is critical.

They should also consider placing a fraud alert or credit freeze on their credit reports to prevent further misuse.

Changing all related passwords and PINs tied to accounts is a necessary step to secure access.

Finally, victims must stay informed about the progress of investigations and maintain contact with the bank until the issue is resolved.

Related Financial and Credit Topics

Credit card theft at the felony level intersects with several financial and credit issues individuals and businesses face. Understanding abuses, management practices, and debit card usage provides context for safeguarding credit and avoiding costly errors.

Understanding Credit Card Abuse and Fraudulent Charges

Credit card abuse typically involves unauthorized use or manipulation of credit cards to make fraudulent purchases or obtain credit. Crimes like using stolen cards or generating fake cards fall under felony credit card theft, carrying severe penalties.

Common fraudulent charges appearing on statements, such as “Acqra charge,” “Blossom Up charge,” or “Towson CMF charge,” often confuse cardholders. These charges may indicate fraud, billing errors, or legitimate vendors unfamiliar to the consumer.

Issues such as “JPMCB Card Services” on a credit report usually denote servicing or management of a card account. Identifying unfamiliar or suspicious charges quickly is essential to minimize fraud losses. Users should monitor accounts frequently and report discrepancies.

Business and Personal Credit Card Management

Managing credit cards for business and personal use requires clear separation to avoid legal and tax complications. For example, credit union business credit cards provide tailored features like expense tracking and higher limits suitable for company use.

Using a business debit card for personal use can complicate accounting, invite audit risks, and may violate cardholder agreements. Proper policies and monitoring must be in place.

With charges such as “Corporate Filings LLC charge” appearing on credit cards, business owners should verify the legitimacy of such transactions. Proper recordkeeping ensures quick resolution in case of disputes.

Debit Card Security and Usage

Debit cards, including Shazam debit cards or US debit vs Visa debit varieties, differ primarily in networks and acceptance but both access funds directly from checking accounts. Security around these cards affects real-time balances rather than credit limits.

A pinless debit card allows transactions without a PIN for low-value purchases but may increase fraud risk. Also, bypassing the PIN, though controversial, can sometimes lead to unauthorized transactions.

Understanding electronic debit card features, including the Bank of Bhutan International debit card, highlights differences like currency conversions and ATM access globally.

Common problems include chip malfunction on debit card, which can prevent in-store chip reading and necessitates use of magstripe or contactless methods.

Debit card transactions typically reflect immediate withdrawals from available funds, not accounts receivable or credit extensions. This distinction affects cash flow and budgeting.

Users with special accounts, such as HSAs, must know if they can withdraw cash from HSA debit card or whether use is restricted to qualified medical expenses.

Jurisdiction-Specific Considerations

Felony-level credit card theft cases vary significantly depending on the jurisdiction where the offense occurs. The distinct frameworks of federal and state laws impact both prosecution and sentencing. Specific legal precedents also guide how courts interpret and apply these laws.

State and Federal Laws Affecting Prosecution

State jurisdictions typically handle credit card theft cases where the offense is confined within one state. Penalties vary by state, often influenced by the dollar amount stolen. For example, Oregon classifies credit card theft severity based on loss value, which affects sentencing length.

Federal jurisdiction applies when the crime crosses state lines or involves federal institutions. Cases involving large-scale fraud, such as those targeting national banking systems or using interstate communication, usually fall under federal law. The prosecution can leverage broader investigative tools, leading to more severe penalties.

Businesses using lines of credit, like those with Tennessee bank business lines or guidance line of credit providers, may experience distinct impacts if fraud involves their accounts, influencing whether federal authorities intervene.

Notable Cases and Precedents

Several landmark cases have shaped the prosecution of felony-level credit card theft. Courts often rely on precedents that clarify jurisdiction, emphasizing either the crime’s geographical span or its impact on federal interests. These rulings confirm that interstate fraud or exploitation of federal financial systems elevates cases to federal courts.

State courts have set precedents defining felony thresholds based on monetary loss and intent. For example, Oregon courts have converted what might be a misdemeanor offense into felony charges when the value exceeds statutory limits. Similarly, federal courts have reinforced the importance of coordinated efforts between state and federal agencies for prosecution.

These legal benchmarks influence how credit card theft involving business lines of credit or corporate tax payments is addressed. They underscore the importance of jurisdiction in determining legal strategies and outcomes.

Financial Recovery and Support Options

Recovering from felony level credit card theft requires a structured approach to repair credit damage, manage outstanding payments, and access legal resources. Practical financial tools and targeted assistance programs can help individuals regain control over their financial health.

Credit Repair After Theft

Credit repair begins with disputing fraudulent charges and clearing unauthorized debts from credit reports. Victims need to contact all three major credit bureaus—Equifax, Experian, and TransUnion—to place fraud alerts or credit freezes to prevent further damage.

It is crucial to obtain copies of credit reports regularly and document communication with creditors. Using services like unsecured business lines of credit or real estate lines of credit may require clean credit records, so swift action is necessary to restore creditworthiness.

Victims should also consider professional credit repair agencies that specialize in identity theft cases to assist with complex disputes. Monitoring credit scores and open accounts helps prevent new fraudulent activities from taking root.

Payment Assistance and Repayment Plans

Managing outstanding debts after credit card theft often involves negotiating payment assistance or repayment plans with creditors. Many lenders offer automatic payment pools or structured plans tailored to the borrower’s financial situation.

For example, repayment options may include extended installment plans or reduced settlement amounts. In certain cases, specialized assistance such as orthodontist payment plans or root canal dentist Seattle payment plans may also be available for medical expenses affected by credit issues.

Homeowners with access to home equity loans in 2nd position (like in Daly City) or construction lines of credit might use these funds to settle debts quickly. Comparing HELOC rates in Wichita, KS, or home equity loan rates in Virginia can inform the decision to tap such resources responsibly.

Legal Aid and Advocacy Resources

Legal support is essential to navigate the complexities of felony credit card theft cases. Victims can reach out to organizations like the Financial Crime Resource Center for assistance with recovery and understanding their rights.

Legal aid may include help filing police reports, disputing fraudulent charges, and pursuing restitution from perpetrators. Advocacy groups often provide guidance on federal and state laws that define credit card theft and fraud, helping victims identify appropriate prosecutions.

Professional legal counsel can clarify implications related to federal statutes like 18 USC § 1029 and assist with navigating the filing of claims. Victims should also explore local resources that help with identity theft lawsuits or victim compensation programs.