Payday Loans Los Angeles: The Complete 2025

Payday Loans Los Angeles is a city of ambition — a place where people come to chase dreams, make a living, and create their own version of success. But it’s also a city with some of the highest living costs in the nation. The average rent for a one-bedroom apartment in LA hovers around $2,500, gas prices are often among the most expensive in the U.S., and even a basic grocery run can feel like a luxury. Add to that the unpredictability of life — a blown tire on the 405, an unexpected visit to urgent care, a missed shift at work — and it’s easy to see how even hardworking Angelenos can find themselves short on cash before payday.

That’s where payday loans in Los Angeles come in. These short-term loans are designed to help residents bridge a temporary financial gap until their next paycheck arrives. They’re fast, accessible, and straightforward — but they also come with rules, costs, and responsibilities that every borrower should understand. In this in-depth guide, we’ll break down exactly what payday loans are, how they work in Los Angeles, the legal protections in place, the costs involved, their benefits and risks, and the smartest ways to use them so you can make informed decisions.

What Is a Payday Loan in Los Angeles?

In California, payday loans are officially known as “deferred deposit transactions.” It’s a technical name for a simple concept: you borrow a small amount of money — up to $300 — and agree to repay it in full, plus a fee, on your next payday. To do this, you write a post-dated check or authorize the lender to electronically withdraw the money from your checking account on the agreed date.

Unlike a personal loan from a bank, which might take days to process and require a strong credit history, payday loans are quick. Most people can apply in under 30 minutes and get the funds the same day or by the next business day. Approval usually depends more on proof of income than on your credit score, making them accessible to a wide range of borrowers, including those with less-than-perfect credit.

How Payday Loans Work in Los Angeles

The process starts when you visit a licensed payday lender — either a storefront in neighborhoods like Hollywood, Inglewood, or Echo Park, or an online lender licensed in California. You’ll provide identification, proof of income, and details of your active checking account. Once the lender verifies your information, they present a written contract that clearly states how much you’re borrowing, the fee you’ll pay, and the exact date your loan is due.

If you agree, you either walk out with cash or receive it via direct deposit. On your next payday — no more than 31 days later — the lender will cash the check you provided or make an electronic withdrawal for the full repayment amount. California law caps the maximum loan at $300 and limits the fee to $15 per $100 borrowed, so the most you can owe in fees is $45.

For example, if you borrow $200, you’ll repay $230 on your next payday. If you borrow $300, you’ll repay $345. It’s straightforward, but because the repayment period is so short, it’s crucial to make sure you can cover the full amount without falling short on other bills.

A Brief History of Payday Lending in California

Payday loans became legal in California in 1996 when the state passed the California Deferred Deposit Transaction Law. This law created strict rules to prevent predatory practices: a $300 maximum loan amount, a $15 per $100 maximum fee, and a ban on rollovers. These rules were designed to make payday loans a short-term, emergency-only option rather than a long-term debt trap.

In Los Angeles, these regulations are enforced by the California Department of Financial Protection & Innovation (DFPI). Licensed lenders must display their license and follow all state guidelines. If they don’t, they risk losing their license and facing legal action.

Why People in Los Angeles Use Payday Loans

The reasons vary, but they often come down to the same thing: life doesn’t wait for payday. A rideshare driver might need $150 to replace a flat tire so they can keep earning income. A single parent in Koreatown might be short on rent because their hours at work were cut unexpectedly. A freelance videographer might need $200 to rent equipment for a last-minute gig that could lead to bigger opportunities. In a city where timing can make or break your week, payday loans provide a fast way to cover a gap.

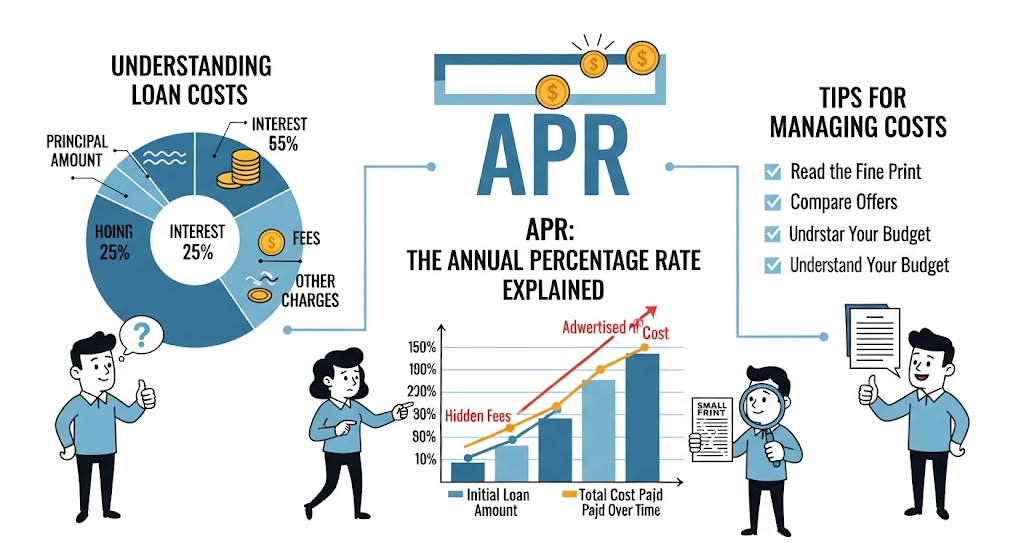

The Costs and the APR Reality

Payday loans in Los Angeles are expensive compared to other forms of credit. The $15 per $100 fee might not sound bad until you annualize it. A $45 fee on a $300 loan over a two-week period works out to an APR of about 460%. That’s why they’re best for one-time emergencies you can repay quickly, not for ongoing expenses or chronic cash shortages.

Still, if the alternative is a $75 late fee on rent or a $100 utility reconnection charge, the math can work in your favor — as long as repayment is certain.

How to Apply for a Payday Loan in LA

Applying for a payday loan in Los Angeles is relatively simple. You need three things: proof of income (like a pay stub or bank statement), a government-issued ID, and an active checking account. Some lenders may also ask for proof of residency. The application can be completed in person at a storefront or online. In many cases, online applications can be approved within an hour, and funds can be deposited the same day if you apply early enough.

What Happens If You Can’t Repay on Time

California law prohibits lenders from rolling over your payday loan, but that doesn’t mean you’re off the hook if you can’t pay on time. If your check bounces or your account lacks sufficient funds, you could face overdraft fees from your bank and potential collection efforts from the lender. Your credit score could also be affected if the debt goes to collections. That’s why it’s critical to borrow only what you’re sure you can repay.

Payday Loan Myths in Los Angeles

Many people believe payday loans are illegal in California — they’re not. Others think you can borrow as much as you need — you can’t, the cap is $300. Some believe all payday lenders are predatory — while some operate unethically, licensed lenders must follow strict state laws. Understanding these facts can help you avoid both misinformation and unnecessary risk.

Alternatives to Payday Loans in LA

Before you take out a payday loan, consider whether you have other options. Credit unions sometimes offer Payday Alternative Loans (PALs) with lower fees and longer repayment terms. Installment loans let you spread payments out over several months. If your emergency is utility-related, LADWP and SoCalGas offer payment plans. Nonprofits like 211 LA County can connect you to emergency assistance programs, and some employers offer paycheck advances.

Payday Loans vs. Other Short-Term Credit

Compared to credit cards, payday loans can be faster to get if your credit is poor, but the cost per dollar borrowed is usually higher. Compared to overdraft protection, they can be cheaper if you avoid multiple overdraft fees. Compared to installment loans, payday loans are smaller, faster, and simpler, but with a shorter repayment term and higher cost.

The Rise of Online Payday Loans in Los Angeles

More Angelenos are turning to online payday loans for convenience. Licensed California lenders can process applications 24/7 and fund loans electronically. But this convenience comes with a warning: some online lenders are based out-of-state and aren’t bound by California law. Always check a lender’s DFPI license before sharing your personal information.

Smart Strategies for Using Payday Loans

If you decide a payday loan is the right move, have a repayment plan in place before you borrow. As soon as you get paid, set aside the loan amount plus the fee. Cut back on non-essential expenses until it’s repaid. Avoid back-to-back borrowing, as this can lead to a cycle of debt. And always use a licensed lender — never an unverified online source.

Future Trends in Payday Lending for LA

Technology is changing payday lending. Some fintech companies are exploring paycheck advance models with lower fees, while others are integrating payday loans into mobile banking apps. Regulatory changes are possible in the coming years, with discussions around raising loan caps, adjusting fees, or introducing more consumer-friendly products. For now, the California framework remains one of the strictest in the country, balancing access with consumer protection.

Payday Loan Statistics and Market Insights in Los Angeles

When we talk about payday loans in Los Angeles, we’re not discussing a small, niche financial product — this is a billion-dollar segment of California’s short-term lending market. According to California Department of Financial Protection & Innovation (DFPI) data, payday lenders issued over 10 million payday loans statewide in the most recent reporting year, with Los Angeles County accounting for nearly 25% of all transactions. That’s roughly 2.5 million loans in LA County alone.

Average Loan Amounts

In Los Angeles, the average payday loan amount is between $250 and $275, just shy of the state’s legal $300 cap. Statewide data shows:

- 68% of borrowers take the maximum $300 loan.

- 22% borrow between $200–$299.

- Less than 10% borrow under $200.

This means the vast majority of loans are at the upper limit, maximizing the $15 per $100 fee allowed under California law.

Annual Percentage Rate (APR) Snapshot

California caps payday loan fees at $15 per $100, but because the term is short — typically 14 days — the APR is much higher:

- $100 loan → $15 fee → ~391% APR

- $200 loan → $30 fee → ~391% APR

- $300 loan → $45 fee → ~391% APR

This rate doesn’t change with the loan size, which makes payday lending one of the most expensive forms of short-term credit available in LA.

Borrower Demographics in Los Angeles

DFPI data reveals a diverse borrower base in the Los Angeles area:

- 54% of payday loan borrowers are women.

- 46% are men.

- The largest age group is 25–44 years old (58% of borrowers).

- Approximately 40% of payday loan users in LA have household incomes under $30,000/year.

Interestingly, payday loans are not exclusive to unemployed individuals — over 80% of borrowers report having full-time or part-time employment at the time of borrowing.

Default and Repayment Trends

While payday loans are designed for quick repayment, not all borrowers manage to repay on time:

- 7% of LA payday loans go into default each year.

- Of these defaults, about 60% are sent to collections.

- Repeat borrowing is common — nearly 50% of LA borrowers take out 4 or more payday loans in a single year, despite the state’s ban on rollovers.

This shows that while payday loans can solve an immediate cash flow issue, they can also lead to repeated usage patterns.

In-Store vs. Online Applications

The payday loan market in Los Angeles has shifted significantly toward digital channels:

- 2015: ~80% of loans were issued in-store.

- 2024: ~55% are now issued online or via mobile apps.

- Younger borrowers (ages 18–34) are twice as likely to use online payday lenders compared to older borrowers.

This digital shift has increased speed and accessibility, but it has also raised concerns about out-of-state lenders attempting to bypass California’s $300 cap and fee limits.

Economic Impact in Los Angeles

The payday loan industry has a measurable economic footprint in LA County:

- Generates over $200 million in annual fee revenue.

- Employs thousands across retail locations, call centers, and back-office operations.

- Plays a role in preventing utility shutoffs, late rent penalties, and job loss for borrowers who use the funds to maintain essential services.

However, high fees mean a large portion of borrower income is funneled out of the community — critics argue that this reduces local economic stability in low-income neighborhoods.

Regulatory Enforcement

The DFPI actively enforces California payday lending laws in Los Angeles:

- In the last year, over 40 enforcement actions were taken against unlicensed lenders.

- More than $2 million in illegal fees were refunded to California borrowers.

- Several online lenders were ordered to cease operations in the state for charging above the legal limits.

This underscores the importance of verifying lender licensing before borrowing.

Year-Over-Year Loan Volume Changes

From 2020 to 2023, the volume of payday loans in Los Angeles saw notable fluctuations:

- 2020: Loan volume dropped by ~25% due to pandemic stimulus payments.

- 2021: Volume began rising again as emergency aid expired.

- 2022–2023: Demand surged, especially in Q4, due to inflation and rising rent costs.

Current trends suggest payday loan usage in LA could continue to rise if wages don’t keep pace with cost-of-living increases.

The Bottom Line

Payday loans in Los Angeles can be a useful tool when you’re facing a short-term cash crunch. They’re fast, accessible, and straightforward — but they’re also expensive if misused. The key is to borrow only when necessary, understand the costs, and have a repayment plan in place before you sign the agreement.

At DollarDay, we connect you to licensed, reputable lenders who follow California’s consumer protection laws. Whether you need $200 for a car repair in Hollywood, $150 for rent in Boyle Heights, or $300 to cover a utility bill in Santa Monica, we help you find safe, legal, and fast payday loan options — so you can solve today’s problem without creating tomorrow’s.

FAQ for Los Angeles Borrowers

1. What are payday loans and how do they work in Los Angeles, California?

A payday loan in Los Angeles is a short-term cash advance that helps cover expenses until your next paycheck. You borrow a small amount—usually $100 to $300—and repay it plus fees on your next payday. Applications are fast, with minimal documentation required, and many lenders offer same-day funding. California law regulates payday loans, including limits on loan amounts and fees. These loans are ideal for emergencies but should be used responsibly due to higher costs.

2. Can I get a payday loan in Los Angeles with bad credit?

Yes. Many Los Angeles payday lenders do not require good credit for approval. Instead, they focus on your income, employment status, and ability to repay. This makes them an option for people with poor or limited credit history. While bad credit won’t usually stop you from getting approved, you still need to meet other basic requirements, such as having a steady source of income and an active checking account, to qualify for a payday loan.

3. How fast can I get cash from a payday loan in Los Angeles?

If you apply in person at a Los Angeles payday loan store, you can often walk out with cash the same day. Online applications may also be approved quickly, with funds deposited into your bank account within one business day. The speed depends on when you apply, your bank’s processing times, and how quickly you provide required documents. Applying early in the day increases the chances of getting your money fast for urgent expenses.

4. What documents do I need for a payday loan in Los Angeles?

Most payday lenders in Los Angeles require a government-issued photo ID, proof of income (like a recent pay stub or bank statement), and an active checking account. Some may ask for proof of address, such as a utility bill. These documents help verify your identity and ability to repay. Having them ready before applying speeds up approval. Whether applying online or in person, the documentation process is generally simple and takes only a few minutes.

5. Are payday loans legal in Los Angeles, California?

Yes. Payday loans are legal in Los Angeles and regulated under California state law. The maximum loan amount allowed is $300, and the maximum fee is 15% of the loan amount. Lenders must clearly disclose all costs and cannot charge additional fees beyond what the law allows. Borrowers should work with licensed lenders registered with the California Department of Financial Protection and Innovation (DFPI) to ensure they are getting a fair and legal loan.

6. What is the maximum payday loan amount in Los Angeles?

In Los Angeles, California law caps payday loans at $300. While this amount may seem small, it is designed to help cover short-term needs until your next paycheck. The fee limit is 15% of the loan amount, so borrowing the maximum $300 will cost you $45 in fees, for a total repayment of $345. If you need more than $300, you may need to consider installment loans or other financial alternatives with longer repayment terms.

7. How do I apply for a payday loan online in Los Angeles?

Applying for an online payday loan in Los Angeles is simple. Visit the lender’s website, fill out the application with your personal and employment details, and upload any required documents. Once approved, funds are deposited into your checking account—often by the next business day. Online applications are convenient if you can’t visit a store. Make sure the lender is licensed in California and displays clear, transparent loan terms before submitting your application.

8. Can I get same-day approval for payday loans in Los Angeles?

Yes. Many payday lenders in Los Angeles offer same-day approvals, especially for in-store applications. If you apply early with all required documents, you can often leave with cash in hand within minutes. Online lenders may also approve applications quickly, but actual funding might take until the next business day. Choosing a lender with same-day cash services is ideal if you need money urgently for unexpected expenses or emergency bills.

9. Do Los Angeles payday lenders check my credit score?

Most payday lenders in Los Angeles do not conduct hard credit checks, so your credit score usually won’t affect approval. Instead, they focus on verifying your income and ability to repay the loan. While a poor credit history is not typically a barrier, failing to repay could result in collections activity, which can hurt your credit score. Payday loans can help those with bad credit, but they should be repaid on time to avoid long-term consequences.

10. What are the fees for payday loans in Los Angeles?

In Los Angeles, California law caps payday loan fees at 15% of the loan amount. For example, if you borrow $200, the fee is $30, making your total repayment $230. While this may seem manageable, the equivalent APR is high due to the short repayment term. Lenders must disclose all fees upfront, and no additional charges are allowed beyond what state law permits. Always read the loan agreement carefully before signing to avoid surprises.

11. Can I repay my Los Angeles payday loan early without penalties?

Yes. In California, you can repay a payday loan early without any prepayment penalties. This can save you money, as you’ll pay only the original fee and no additional charges. If you have the funds to repay before your due date, doing so is a smart choice. Early repayment reduces the risk of late fees, bounced payments, or collection actions. Always confirm your lender’s policy, but reputable lenders encourage early payoff to maintain good customer relationships.

12. What happens if I can’t repay my payday loan on time in Los Angeles?

If you cannot repay your payday loan in Los Angeles on time, you may face additional charges, collections, and possible bank account debits. California does not allow rollovers, so you’ll need to repay the full balance or work out a payment plan with your lender. Some lenders may offer extended payment arrangements at no extra cost. Failing to repay could impact your financial standing, so it’s best to communicate with your lender before the due date.

13. Are there alternatives to payday loans in Los Angeles?

Yes. Alternatives include personal installment loans, credit union payday alternative loans (PALs), credit card cash advances, or borrowing from friends or family. Some nonprofit organizations in Los Angeles also provide emergency assistance for bills, rent, or utilities. While payday loans are quick, these alternatives often come with lower fees and more flexible repayment terms. If you qualify, a credit union PAL can offer small loans at a fraction of the cost of traditional payday lending.

14. Do I need a bank account to get a payday loan in Los Angeles?

In most cases, yes. Payday lenders in Los Angeles require an active checking account to deposit your loan and collect repayment. Online lenders, in particular, rely on electronic transfers. Some in-store lenders may offer cash payouts, but they still often require bank account details for security and repayment tracking. Having a bank account also helps speed up the approval process. Check with your lender if you’re unsure about their specific account requirements.

15. How many payday loans can I have at the same time in Los Angeles?

In California, you can only have one payday loan at a time, regardless of the lender. This law helps prevent borrowers from taking on multiple high-cost loans that can quickly lead to financial trouble. Once you repay your current loan, you may be eligible for another. Attempting to take out multiple payday loans at once could result in denial or legal issues. Responsible borrowing is essential to avoid getting caught in a debt cycle.

16. Are there licensed payday loan stores in downtown Los Angeles?

Yes. Downtown Los Angeles has many licensed payday loan stores offering walk-in applications and same-day cash. Locations are often near public transportation hubs for convenience. To ensure you’re dealing with a legitimate lender, verify that the business is licensed by the California Department of Financial Protection and Innovation (DFPI). Licensed lenders follow state laws regarding fees, loan amounts, and repayment terms, protecting you from unregulated or predatory lending practices.

17. Can I roll over a payday loan in Los Angeles?

No. California law prohibits payday loan rollovers. This means you cannot extend your due date by paying only the fee; you must repay the entire balance when it’s due. However, some lenders may allow you to enter into an extended payment plan without additional charges if you’re unable to repay on time. This consumer protection measure is designed to prevent borrowers from falling into a cycle of debt caused by repeated rollovers.

18. What are the pros and cons of payday loans in Los Angeles?

Pros include fast approval, minimal documentation, and access to funds for people with poor credit. They’re ideal for urgent financial needs. Cons include high fees, small loan amounts, and short repayment terms. California’s $300 cap and 15% fee limit reduce risks compared to some states, but payday loans can still be expensive. Borrowers should weigh these factors and explore alternatives before committing to ensure they choose the best option for their financial situation.

19. How do I find a trustworthy payday lender in Los Angeles?

Look for lenders licensed by the California Department of Financial Protection and Innovation (DFPI). Check reviews online, verify the business address, and confirm that fees and terms are clearly disclosed. Avoid lenders that pressure you to borrow more than you need or refuse to provide written agreements. A trustworthy lender will be transparent, follow state laws, and provide responsive customer service both in person and online. Licensing and clear terms are key signs of credibility.

20. Is it better to get a payday loan online or in-person in Los Angeles?

Both options have advantages. Online payday loans in Los Angeles offer convenience and allow you to apply anytime, with funds deposited into your bank account. In-person loans provide same-day cash and personal assistance from staff. The choice depends on your needs—online loans are ideal if you prefer speed and privacy, while in-person loans work well if you need immediate cash or have questions. In either case, choose a licensed California lender for safety.