Introduction: Why Payday Loans Matter in San Diego

San Diego is a city that blends the laid-back charm of the California coast with the bustling energy of a major metropolitan hub. Yet beneath the sunshine, scenic beaches, and thriving economy, the high cost of living can put immense financial pressure on residents. The median rent here is among the highest in the nation, utilities cost more than the national average, and unexpected expenses — from medical emergencies to urgent car repairs — can throw even the best-planned budget into chaos. In such moments, payday loans in San Diego present themselves as a quick, no-hassle way to bridge the gap until your next paycheck.

These loans are popular because of their speed. In many cases, you can walk into a lender’s office or apply online in the morning and have cash in your bank account before the day is over. But speed comes with a price. Payday loans are known for their steep fees and short repayment periods, which means they are best suited for emergencies and not as a long-term financial solution. By understanding the rules, costs, and alternatives, San Diego residents can make informed decisions that protect their financial health while addressing urgent needs.

Understanding Payday Loans in San Diego

A payday loan is a short-term, small-dollar loan intended to cover urgent expenses until your next paycheck. In San Diego, like the rest of California, payday loans are tightly regulated. The maximum amount you can borrow is $300, and the loan term cannot exceed 31 days. The repayment is typically due in one lump sum, either through a post-dated check you give to the lender or an automatic withdrawal from your bank account.

This type of loan is designed for speed and convenience. Lenders focus less on your credit history and more on proof of steady income, making payday loans accessible to those who may not qualify for traditional credit cards or personal loans. However, the accessibility can be a double-edged sword — it makes payday loans tempting even when other, more affordable options might be available. In a city where living expenses are high and incomes vary widely between industries, payday loans can seem like a financial lifeline, but they require careful planning to avoid debt traps.

How California Law Regulates Payday Loans

California’s payday loan industry is governed by the California Deferred Deposit Transaction Law, enforced by the Department of Financial Protection and Innovation (DFPI). This law sets strict limits to protect consumers from excessive debt. For example, the maximum loan amount is capped at $300, and lenders can charge no more than $15 for every $100 borrowed. That means the highest fee you can legally be charged is $45 on a $300 loan.

The law also prohibits loan rollovers. In other words, you can’t take out a new payday loan to pay off an existing one. This rule is designed to prevent borrowers from spiraling into cycles of debt. Additionally, California requires that all payday lenders be licensed, and borrowers can verify a lender’s license through the DFPI’s public database. If you find yourself unable to repay on time, the law grants you the right to request an extended payment plan with no extra fees, provided you make the request before your loan’s due date. These protections are essential for San Diegans to understand before signing any payday loan agreement.

The Real Costs You Should Know

While $45 in fees for a $300 loan might not sound alarming, it’s important to understand how that translates to an annual percentage rate (APR). Because the repayment period is typically two to four weeks, the APR can reach nearly 391%. This is significantly higher than most other forms of credit, including credit cards, personal loans, and even some cash advances from banks.

Consider this: if you take out multiple payday loans over the course of a year — say, one every month — the fees alone could easily add up to hundreds or even thousands of dollars. And because these loans require repayment in full on your next payday, failing to budget for repayment can lead to overdraft fees, late charges, or even collection actions. The convenience is real, but so is the cost, and understanding that balance is crucial for any borrower in San Diego.

Common Reasons San Diegans Use Payday Loans

San Diego residents turn to payday loans for a variety of urgent reasons. Housing costs are a major factor — missing rent or mortgage payments can lead to eviction or foreclosure, and payday loans can help bridge short-term gaps. Utility bills are another common driver, especially during peak summer months when electricity costs rise due to air conditioning use.

Vehicle repairs are also high on the list, as San Diego’s spread-out layout and limited public transportation options make reliable transportation essential. In addition, medical bills, especially for emergencies not fully covered by insurance, often push residents to seek quick cash solutions. Seasonal income fluctuations also play a role; workers in tourism, hospitality, and other cyclical industries may rely on payday loans to smooth out income gaps during slower periods.

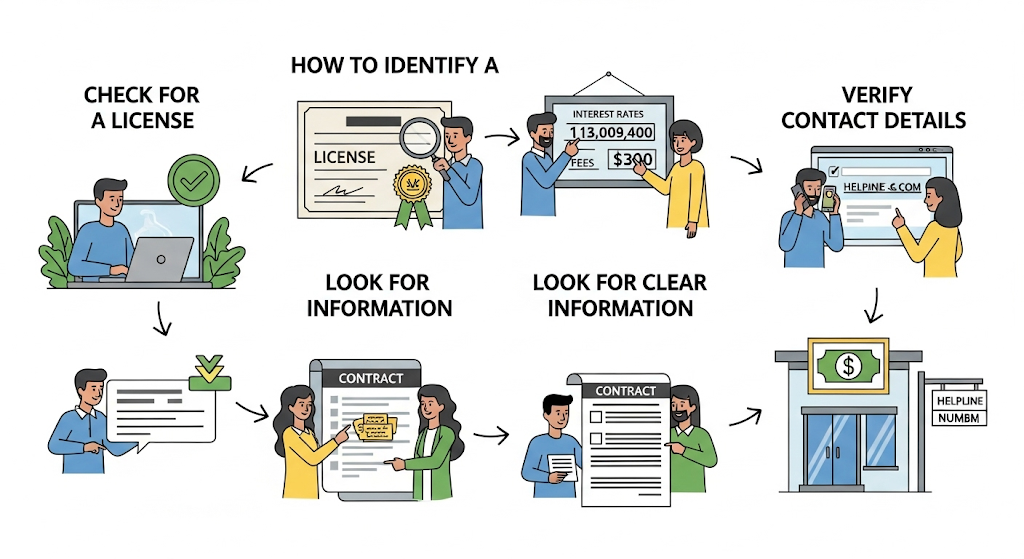

How to Spot a Licensed Payday Lender

In a city the size of San Diego, payday lenders are easy to find — but not all of them operate legally. California law requires every payday lender to be licensed by the DFPI. Before doing business, you should check the lender’s license on the DFPI’s official website. A legitimate lender will display their license number prominently in their office or on their website.

Working with an unlicensed lender can be risky. These operators may charge illegal fees, skirt repayment plan requirements, or even engage in aggressive collection tactics. By sticking with licensed lenders, you not only ensure compliance with state laws but also gain access to consumer protections that can make a huge difference if repayment becomes difficult.

The Application Process: Step-by-Step

Applying for a payday loan in San Diego is designed to be quick and straightforward. You’ll need to provide proof of income, a valid government-issued ID, and an active checking account. Most lenders will approve your application within minutes, and you can receive funds the same day via cash, check, or direct deposit.

Repayment is typically handled through a post-dated check or automatic withdrawal from your bank account. This automatic repayment method is convenient but can lead to overdraft fees if your account doesn’t have enough funds on the due date. That’s why it’s crucial to borrow only what you can comfortably repay.

The Risks of Defaulting on a Payday Loan

Failing to repay a payday loan in San Diego can have serious consequences. Lenders may attempt to withdraw funds from your bank account multiple times, leading to overdraft fees. If the loan remains unpaid, it can be sent to collections, damaging your credit score even though payday loans aren’t typically reported to credit bureaus.

Defaulting can also result in legal action, though this is less common. The best way to avoid these risks is to have a clear repayment plan before you borrow and to communicate with your lender if repayment problems arise.

Comparing Payday Loans with Other Credit Options

While payday loans are known for their speed and ease of access, they’re far from the only short-term credit option available in San Diego. Credit union payday alternative loans (PALs), for example, allow borrowers to access up to $2,000 with repayment terms of one to 12 months and far lower fees than payday loans. These loans often require membership in the credit union, but many local institutions make joining quick and affordable.

Personal installment loans from banks or online lenders also offer a viable alternative. These loans generally carry lower interest rates, especially for borrowers with fair or good credit, and allow repayment over several months or years. While the application process may take longer than a payday loan, the cost savings can be substantial. For example, a $1,000 personal loan with a 25% APR over 12 months will cost significantly less in interest than rolling over payday loans multiple times to cover the same expense.

Even credit cards — often criticized for high interest rates — can be a better choice for short-term borrowing if you can pay off the balance quickly. Many cards offer introductory 0% APR periods, which can give you breathing room without accruing interest. The key difference between these options and payday loans lies in the repayment structure: alternatives allow gradual repayment, making them less likely to trigger the debt cycle that payday loans can cause.

Statistics About Payday Loans in San Diego

Data from the California Department of Financial Protection & Innovation shows that San Diego County saw over 2.2 million payday loans issued in the last reporting year. The average loan amount was $275, just under the state maximum of $300. Nearly 50% of borrowers took out four or more loans within a 12-month period, a strong indicator of repeat borrowing patterns.

A closer look at borrower demographics reveals that payday loan use is highest among residents earning less than $40,000 annually. In San Diego, where the median household income is around $89,000, this means payday loans disproportionately affect lower-income households. Additionally, the majority of payday loans are used for essential expenses rather than discretionary spending. Housing-related costs, utility bills, and transportation needs rank as the top three reasons for borrowing.

Another notable trend is the growing role of online lending. More than half of payday loans in San Diego are now issued through online platforms, a sharp increase from just 30% in 2018. While this shift offers convenience, it also raises concerns about unlicensed lenders operating from outside California and charging illegal fees. This makes consumer education and license verification more important than ever.

The Rise of Online Payday Lending

The digital transformation has touched nearly every industry, and payday lending is no exception. In San Diego, online payday loans now account for the majority of transactions. Borrowers are drawn to the convenience: you can apply from home or even on your phone, get approval within minutes, and receive funds directly into your bank account, sometimes within hours.

However, the convenience of online lending comes with new risks. Many online lenders are based out of state or even overseas, placing them beyond the reach of California’s consumer protection laws. These lenders may charge fees well above the legal maximum, impose aggressive repayment terms, or ignore your right to an extended payment plan.

To stay safe, San Diego residents should limit their online borrowing to lenders licensed by the DFPI. Licensed online lenders are required to follow the same rules as storefront operations, including fee caps and prohibitions on rollovers. Verifying licensing is quick and can save you from predatory practices that could worsen your financial situation.

Strategies to Borrow Responsibly

If you decide that a payday loan is your best or only option, it’s critical to approach the process with a clear strategy. Start by borrowing the smallest amount necessary to cover your emergency. Every additional dollar borrowed increases your fee, and in a high-cost loan like a payday advance, that cost adds up quickly.

Plan your repayment before you take the loan. Review your upcoming paychecks, existing bills, and any other financial obligations to ensure you’ll have enough left over to cover the loan in full. If you anticipate difficulty, ask for an extended payment plan upfront. California law guarantees your right to such a plan without additional fees, as long as you request it before the due date.

Lastly, limit payday loans to true emergencies. Building even a small emergency savings fund — $500 to $1,000 — can help you avoid payday loans entirely. While this may be challenging in San Diego’s high-cost environment, setting aside small amounts consistently can make a significant difference over time.

Alternatives for Military Families in San Diego

San Diego is home to one of the largest concentrations of military personnel in the country, with major bases like Naval Base San Diego and Marine Corps Air Station Miramar. While payday loans may seem like an easy fix for unexpected expenses, active-duty service members and their families have special protections under federal law.

The Military Lending Act (MLA) caps the annual percentage rate on most loans to 36% for active-duty members and their dependents. This cap applies to payday loans, vehicle title loans, and certain installment loans. Many military-focused credit unions and on-base financial institutions also offer low-interest emergency loans that can serve as safer alternatives.

Service members are encouraged to seek assistance from resources like the Navy-Marine Corps Relief Society, which provides interest-free loans and grants for emergencies. Using these resources can help military families avoid the high costs and potential pitfalls of payday loans while still addressing urgent financial needs.

How Payday Loans Affect Your Credit in San Diego

One of the most misunderstood aspects of payday loans is how they impact your credit profile. In most cases, payday lenders in San Diego do not report your on-time payments to the three major credit bureaus — Equifax, Experian, and TransUnion. This means that even if you repay your loan in full and on time, it will not boost your credit score the way responsible use of a credit card or installment loan might.

However, if you default on a payday loan and the debt is sent to a collections agency, that collection account will almost certainly be reported to the credit bureaus. Collections entries can significantly lower your credit score and remain on your report for up to seven years. This can make it more difficult to qualify for other credit products, secure favorable interest rates, or even pass tenant background checks when renting an apartment in San Diego’s competitive housing market.

In short, payday loans are largely credit-neutral if handled properly but can be extremely damaging if left unpaid. Borrowers looking to improve their credit should consider alternative products, like secured credit cards or credit-builder loans, that both provide needed funds and contribute positively to their credit history.

Payday Loan Scams to Avoid in San Diego

Unfortunately, the popularity of payday loans has also given rise to scams targeting vulnerable borrowers. In San Diego, these scams often take the form of fake online lenders who promise quick approval and no credit checks. They may ask for upfront fees, personal banking information, or even copies of identification — all of which can be used for identity theft.

One common tactic involves posing as a legitimate lender and requesting a “processing fee” before releasing the loan. Legitimate payday lenders in California never require upfront payments; all fees are deducted from the loan amount or paid upon repayment. Another scam variation involves aggressive “debt collectors” who claim you owe money on a payday loan you never took out. These scammers often use threats of arrest or lawsuits to pressure victims into paying.

To protect yourself, always verify that the lender is licensed with the California Department of Financial Protection & Innovation. Avoid lenders who cannot provide a license number or whose terms seem too good to be true. In the world of payday lending, if it sounds too easy or too cheap, it probably is.

The Future of Payday Lending in San Diego

The payday lending landscape in San Diego is evolving rapidly, shaped by changes in technology, state regulation, and consumer preferences. As more borrowers move online, licensed lenders are adapting with faster application processes, mobile-friendly platforms, and instant funding options. At the same time, California regulators are monitoring the industry closely, considering measures that could further lower borrowing costs or expand loan alternatives for low-income residents.

Financial technology (fintech) companies are also entering the space with innovative solutions like earned wage access (EWA) programs, which allow workers to withdraw a portion of their earned wages before payday. These programs, offered by some San Diego employers, can provide a low-cost or even free alternative to payday loans, helping employees avoid high-interest debt altogether.

Looking ahead, the focus is likely to shift toward increased transparency, lower fees, and the integration of financial education into loan services. For San Diego residents, staying informed about these changes will be key to making smarter borrowing decisions in the years to come.

Conclusion: Making Smart Choices with Payday Loans in San Diego

Payday loans in San Diego offer a unique mix of advantages and risks. On the one hand, they provide fast, accessible cash to residents facing urgent financial needs, often without the credit checks or lengthy approval processes required by traditional lenders. On the other hand, their high costs, short repayment terms, and potential for debt cycles make them a tool that must be used with extreme caution.

By understanding California’s strict payday lending laws, verifying lender licenses, and being aware of both the benefits and dangers, you can protect yourself from predatory practices. Exploring alternatives — from credit union payday alternative loans to earned wage access programs — can also save you money and reduce stress.

In a high-cost city like San Diego, financial emergencies are almost inevitable. What matters most is how you respond when they arise. With the right knowledge, a clear repayment plan, and a willingness to consider lower-cost options, you can navigate short-term financial challenges without jeopardizing your long-term stability. Payday loans may be a part of your financial toolkit, but they should never be the whole toolbox.

FAQs :Payday Loans in San Diego

1. Are payday loans legal in San Diego?

Yes, payday loans are legal in San Diego under California law. Licensed lenders can offer loans up to $300 with a maximum fee of $15 per $100 borrowed. Loan terms cannot exceed 31 days, and rollovers are prohibited to protect consumers from excessive debt.

2. How much can I borrow with a payday loan in San Diego?

California law caps payday loans at $300. This amount includes the loan principal and the lender’s fee. For example, if you borrow the maximum, the lender may deduct their fee upfront, so the cash you receive will be slightly less than $300.

3. Do payday lenders in San Diego check credit?

Most payday lenders in San Diego do not run a full credit check. Instead, they focus on proof of income, a valid ID, and an active checking account. This makes payday loans accessible to borrowers with poor or limited credit histories.

4. What happens if I can’t repay my payday loan on time?

If you can’t repay on time, your lender may attempt to withdraw funds from your bank account, causing overdraft fees. You can request an extended payment plan before the due date without extra charges under California law, helping avoid default and further penalties.

5. How quickly can I get a payday loan in San Diego?

In most cases, you can receive funds the same day you apply. Many storefront lenders disburse cash immediately, while online lenders may deposit funds into your bank account within 24 hours, depending on the time of application and your bank’s policies.

6. Are online payday loans safe in San Diego?

Online payday loans are safe if the lender is licensed in California. You can verify a lender’s license on the California Department of Financial Protection & Innovation website. Avoid unlicensed online lenders, as they may charge illegal fees or engage in aggressive collection practices.

7. Can payday loans in San Diego improve my credit score?

Generally, no. Payday loans are not reported to credit bureaus if repaid on time. However, if the loan goes unpaid and is sent to collections, it will likely appear on your credit report and negatively impact your score for up to seven years.

8. Are there cheaper alternatives to payday loans in San Diego?

Yes. Alternatives include credit union payday alternative loans, personal installment loans, credit cards, and earned wage access programs. These options often offer lower interest rates, longer repayment periods, and a reduced risk of falling into a debt cycle compared to payday loans.

9. What fees can payday lenders in San Diego charge?

Lenders can charge a maximum of $15 per $100 borrowed. For example, on a $300 loan, the maximum fee is $45. This fee structure results in a high APR, often exceeding 391%, making payday loans one of the most expensive forms of credit.

10. How can I verify a payday lender’s license in San Diego?

Visit the California DFPI website and use their license search tool to confirm the lender’s legitimacy. Licensed lenders are required to display their license number in-store and online. Verifying this helps ensure you are dealing with a regulated, legal lender.