Introduction to Payday Loans in Phoenix

Phoenix is one of the fastest-growing cities in the United States, with a diverse population and a cost of living that, while more affordable than in some states, has been steadily increasing. From unexpected car repairs to medical emergencies, many residents find themselves facing short-term financial gaps.

Payday loans in Phoenix have emerged as a popular — though often debated — solution for quick cash. Unlike traditional bank loans, payday loans are designed for speed and accessibility, allowing borrowers to receive funds within hours.

However, while these loans can be lifesavers in a financial pinch, they also come with high costs that require careful consideration. Think of them as an emergency fire extinguisher: helpful in urgent situations, but risky if overused.

How Payday Loans Work in Phoenix

The process is straightforward: a borrower writes a post-dated check or provides authorization for a direct debit, and in exchange, receives a short-term loan — typically $100 to $1,000 — due on their next payday. In Phoenix, most payday loans have terms of 14 to 31 days, making them ideal for short-term needs but less suited for long-term debt management.

Lenders often require proof of income, identification, and a checking account, but they rarely perform a full credit check, which is why they remain accessible even to borrowers with poor credit scores.

Life Example: Monica, a Phoenix resident, had her car break down two days before payday. With no savings on hand, she applied for a $400 payday loan online at 9 a.m. and had the funds deposited by noon — allowing her to pay for urgent repairs and still make it to work the next day.

Legal Status of Payday Loans in Arizona

Arizona has strict payday loan regulations compared to some other states. In fact, traditional payday lending was banned in Arizona in 2010, but short-term installment loans and title loans remain available under alternative lending laws.

This means that while you might not see “payday loans” advertised in the traditional sense, many lenders in Phoenix offer similar high-cost, short-term products under different names.

These loans can still carry high APRs — sometimes exceeding 200% — but they must comply with state lending caps and consumer protection rules. Borrowers should be aware of these nuances to avoid confusion or falling for misleading advertising.

Data Insight: According to the Arizona Attorney General’s Office, one of the most common complaints from consumers involves lenders disguising payday loans as “flex loans” to skirt state restrictions.

Eligibility Requirements for Phoenix Payday Loans

While Arizona law restricts traditional payday loans, alternative short-term lending options have relatively simple requirements. Most lenders will approve applications if the borrower:

- Is at least 18 years old

- Has proof of steady income (employment or benefits)

- Maintains an active checking account

- Provides valid government-issued identification

These minimal barriers mean that many Phoenix residents can access such loans, even if they have past bankruptcies or a low credit score. However, meeting eligibility criteria doesn’t mean borrowing is always the right choice. Responsible lenders will also evaluate the borrower’s ability to repay without jeopardizing essential living expenses.

Life Example: David, a part-time worker in Phoenix, qualified for a $500 short-term loan despite having a credit score of 540, simply because he had a consistent paycheck and an active bank account.

Online vs. Storefront Payday Loans in Phoenix

In Phoenix, borrowers can choose between walking into a physical lending store or applying online.

Storefront loans offer in-person service, instant check cashing, and the ability to ask questions face-to-face — useful for those unfamiliar with loan terms.

Online loans, on the other hand, offer the convenience of applying from home, 24/7 availability, and quick electronic funding. Each method has its pros and cons: storefront lenders may process cash payouts faster, while online lenders can sometimes approve loans outside normal banking hours.

Life Example: Lisa, who works two jobs, applied for an online payday-style loan during her lunch break. She uploaded her pay stubs, signed the e-contract, and had the funds in her account before she clocked out — all without stepping foot in a store.

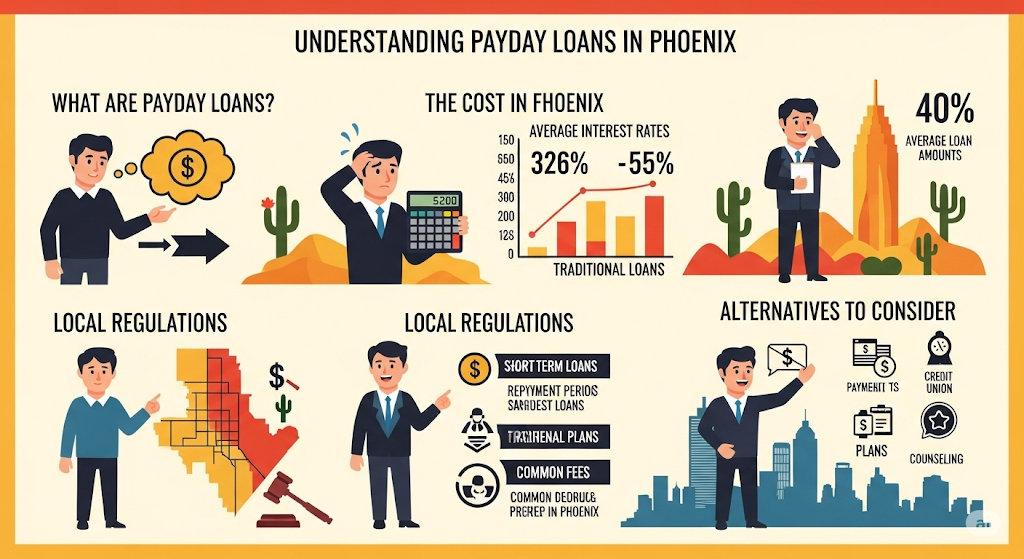

Understanding the Cost of Payday Loans in Phoenix

When considering a payday loan in Phoenix, the first factor to examine is the total cost — not just the loan amount. In Arizona, payday loans are regulated under state law, which imposes certain limits on fees, but borrowers can still face high annual percentage rates (APRs) when converted from short-term fees.

For example, a $15 fee on a $100 loan for two weeks may seem small, but when calculated over a year, it equates to an APR of nearly 391%.

In practice, many Phoenix residents underestimate the long-term financial implications. While the loan might provide instant relief for emergencies like medical bills or urgent car repairs, the repayment structure can trap borrowers in cycles of debt if they’re not careful. Understanding these costs in real terms — and comparing them with alternatives like personal loans from credit unions — is essential for making an informed decision.

Life Example: Maria, a waitress in downtown Phoenix, took out a $300 payday loan to cover a surprise utility bill. She repaid it in two weeks with a $45 fee. While this seemed manageable, she repeated the process twice in the same month due to ongoing expenses, ultimately paying $135 in fees for $300 borrowed.

State Regulations and Borrower Protections in Arizona

Arizona has specific laws designed to protect payday loan borrowers, though loopholes can still lead to high costs. The state’s Consumer Lender Law governs payday lending, limiting the loan amount to $2,500 and regulating the maximum fees lenders can charge. Additionally, lenders must clearly disclose all costs before you sign the agreement, giving borrowers the opportunity to compare offers.

Borrowers also benefit from the right to a repayment plan if they cannot pay on time, provided they request it before defaulting. However, these protections only apply to licensed lenders operating in Arizona. This means that Phoenix residents should be cautious about online payday lenders based out-of-state, as they may not adhere to Arizona’s rules.

Life Example: Jason, a Phoenix resident, avoided paying illegal rollover fees when he discovered the lender was not licensed in Arizona. By reporting the company to the Arizona Department of Financial Institutions, he was able to cancel the loan without penalty.

Common Reasons Phoenix Residents Turn to Payday Loans

In Phoenix, payday loans are often sought for pressing financial needs when traditional lending isn’t an option. While every borrower’s situation is unique, certain patterns emerge:

- Emergency Medical Bills: Without insurance or with high deductibles, unexpected medical expenses push many toward fast cash solutions.

- Car Repairs: Phoenix’s sprawling geography means owning a car is essential. A broken transmission or flat tire can disrupt both work and family responsibilities.

- Rent and Utility Payments: High summer electricity bills due to air conditioning often create urgent cash flow gaps.

- Unexpected Travel: Family emergencies, especially for those with relatives outside Arizona, lead to unplanned trips and associated costs.

Life Example: In July, when temperatures soared past 110°F, Tanya faced a $450 utility bill. Without enough savings and fearing power disconnection, she took out a $500 payday loan, planning to repay it after her next paycheck.

The Role of Online Payday Lenders in Phoenix

While brick-and-mortar payday loan stores are still common across Phoenix, the rise of online lenders has transformed the borrowing landscape. Digital payday loans offer quick applications, instant approval decisions, and direct deposit — all without requiring a physical visit.

However, online convenience comes with risks. Some lenders operate from outside Arizona and ignore state regulations, charging exorbitant rates or using aggressive collection tactics. Others may lack proper encryption, risking the security of borrowers’ personal and banking information.

Life Example: Luis applied for a payday loan through a flashy online ad promising “guaranteed approval.” Within minutes, he was approved for $300, but the lender charged $90 in fees for two weeks. Worse, the company attempted unauthorized withdrawals from his account, forcing him to close it.

How Payday Loans Impact Phoenix’s Local Economy

Although payday loans can provide short-term relief for individuals, they have a broader economic effect on Phoenix communities. Every dollar paid in loan fees is a dollar not spent in local businesses. Over time, this reduces the economic vitality of neighborhoods, especially in areas where payday loan stores are heavily concentrated.

According to community finance advocates, millions of dollars leave the Phoenix economy each year due to payday loan interest and fees. This outflow disproportionately affects low-income households, who often cycle through loans multiple times a year. Efforts by local nonprofits to promote financial literacy aim to counteract this drain by helping residents explore safer borrowing options.

Life Example: In West Phoenix, a neighborhood with several payday loan storefronts saw a drop in small business sales. Community surveys revealed that many residents were diverting discretionary spending to cover recurring loan repayments rather than supporting local shops and restaurants.

Understanding Payday Loan Rollovers in Phoenix

One of the biggest traps borrowers in Phoenix fall into is the rollover cycle — when a payday loan is extended or replaced with another because the borrower can’t pay it back in full. While it might feel like a short-term fix, the financial consequences can be steep.

Every rollover adds new fees, which in turn increase the total cost of borrowing. Arizona law limits certain rollover practices, but creative lender tactics, like refinancing as a “new loan,” still catch many consumers off guard. Imagine taking a $400 loan and rolling it over twice;

Instead of paying back just $400 plus one fee, you could end up paying $200 or more in extra charges, without making a dent in the principal. This is why financial experts in Phoenix warn borrowers to avoid rollovers unless absolutely unavoidable, and even then, to have a concrete repayment strategy in place.

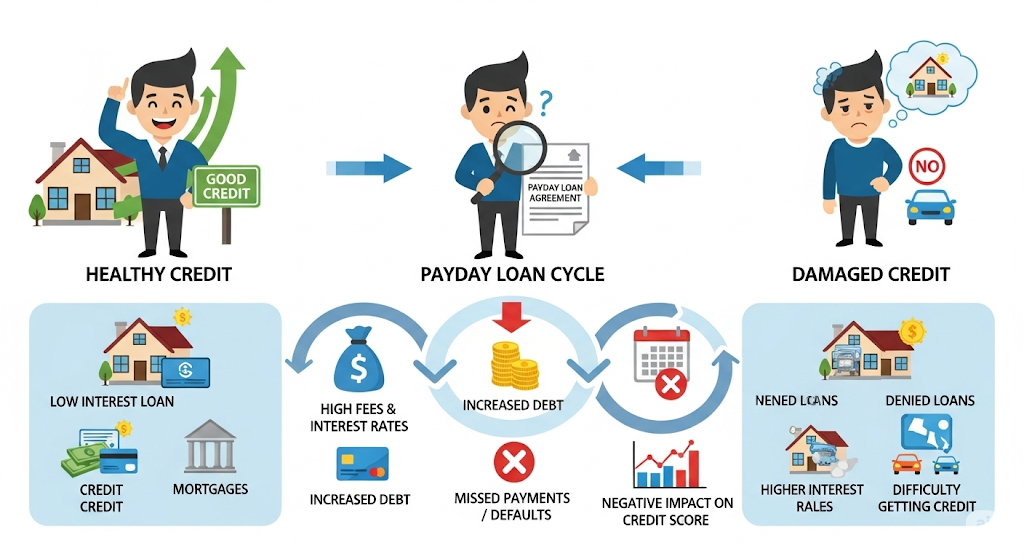

Payday Loans and the Impact on Credit Health

In Phoenix, payday loans rarely improve your credit score because most lenders do not report on-time payments to the major credit bureaus. However, missed payments can do serious harm if the debt is sold to collections. A single default can lower your credit score by 50–100 points, making it harder to qualify for car loans, mortgages, or even rental agreements. This hidden risk often catches borrowers by surprise.

For example, one Phoenix resident, after losing his job, defaulted on a $300 payday loan. Within weeks, a collection agency was calling daily, and his credit score dropped so much that he couldn’t qualify for an affordable auto loan, forcing him to buy an older, unreliable vehicle. This ripple effect shows why even a “small” payday loan must be handled with caution.

The Rise of Online Payday Loans in Phoenix

Digital technology has transformed payday lending in Phoenix. Instead of walking into a storefront on Camelback Road or Van Buren Street, borrowers can now apply from their phones and receive funds in their bank account within hours. While this convenience is a major selling point, it also means loans are easier to obtain impulsively.

The lack of face-to-face interaction often reduces the perceived seriousness of the debt, leading to overborrowing. For instance, a Phoenix gig worker might take out an online loan at 11 PM after an unexpectedly low earnings day — something they may have reconsidered had they been required to meet with a lender in person. The 24/7 availability of online loans is both a lifeline and a potential hazard.

Seasonal Demand for Payday Loans in Phoenix

Certain times of year see noticeable spikes in payday loan usage in Phoenix — particularly in late summer when utility bills climb past $300 for many households due to extreme heat, and in December during the holiday season. The pressure to cover higher bills or buy gifts pushes many residents to seek quick-cash solutions.

One Phoenix mother, for example, used a $500 payday loan in August to keep her air conditioning running after an unexpectedly high electricity bill. While it solved the immediate problem, the repayment — due in two weeks — clashed with her back-to-school expenses, forcing her into a second loan. These seasonal trends show how environmental and cultural factors can directly impact borrowing habits in the Valley.

Alternatives That Phoenix Borrowers Should Consider

Although payday loans are fast, they aren’t the only option in Phoenix. Credit unions like Desert Financial and Arizona Federal offer small-dollar loans at much lower rates, and many local nonprofits provide emergency cash assistance for rent, utilities, and groceries.

Churches and community centers sometimes have benevolence funds available for urgent needs. Even negotiating with utility companies or landlords can yield payment extensions without added interest.

Consider the case of a Phoenix Uber driver whose car broke down; instead of taking a payday loan, he applied for an emergency loan through his credit union and secured $600 at a 12% APR — saving hundreds compared to a high-interest payday loan. Exploring these alternatives can prevent short-term financial relief from becoming a long-term debt burden.

Payday Loan Regulations in Phoenix: What Borrowers Must Know

Arizona’s state laws heavily influence payday lending in Phoenix, and understanding these rules can help borrowers avoid unnecessary penalties. While some payday loan practices are restricted, loopholes allow similar short-term, high-interest products to remain available under different names, such as “title loans” or “flex loans.”

For example, while a traditional payday loan might have a set repayment date, a flex loan could function like a line of credit, but with comparable fees and risks. This creates a regulatory gray area where borrowers may believe they’re getting a safer option, only to face similar debt traps.

Phoenix residents need to carefully read all loan agreements, paying attention to APR disclosures, repayment schedules, and any mention of automatic withdrawals from bank accounts. Consumer protection agencies, such as the Arizona Attorney General’s Office, provide free resources and complaint channels for those who suspect predatory lending practices.

How Payday Loans Affect Phoenix’s Low-Income Communities

The impact of payday loans in Phoenix disproportionately affects low-income neighborhoods, where access to traditional banking services is often limited. In these communities, payday loan storefronts cluster in high-density areas, offering easy access but at a high cost.

Data from community financial studies shows that in certain Phoenix ZIP codes, more than 25% of households have used payday or title loans within the last three years.

A real-life example is South Phoenix, where local nonprofits report that residents often juggle multiple high-interest loans while trying to meet basic living expenses. The cycle is compounded when borrowers use one loan to pay off another, leaving little room for financial recovery.

Breaking this cycle often requires targeted intervention, such as financial literacy workshops, debt counseling, and alternative credit-building programs tailored to these communities.

Emergency Scenarios That Lead to Payday Loan Usage in Phoenix

Many Phoenix residents turn to payday loans only when faced with urgent, unavoidable expenses. This includes emergency medical bills, last-minute travel for family emergencies, or urgent car repairs that, if left unresolved, could jeopardize employment.

Consider a Phoenix construction worker whose truck broke down unexpectedly — without a vehicle, he couldn’t get to job sites. A payday loan of $600 allowed him to make repairs within 24 hours, ensuring he didn’t lose work. However, the high repayment amount two weeks later created new financial strain.

These scenarios highlight the double-edged nature of payday loans: they can solve immediate problems but create longer-term challenges if not managed strategically. Having an emergency savings fund or access to low-interest alternatives can reduce reliance on these loans during crises.

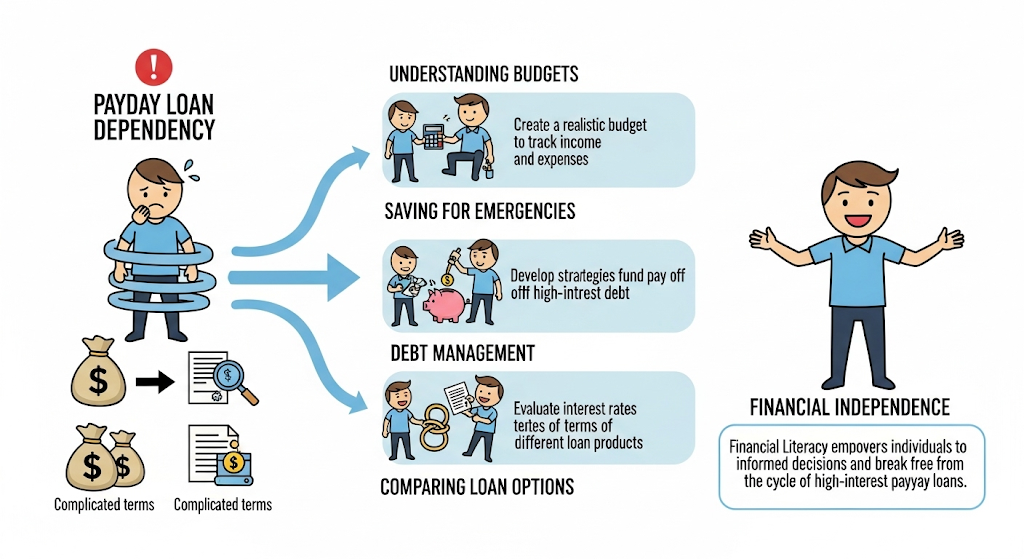

The Role of Financial Literacy in Reducing Payday Loan Dependency

In Phoenix, financial literacy programs have shown measurable success in reducing payday loan usage. When residents understand how interest rates compound, how credit scores work, and what alternatives exist, they are less likely to fall into high-cost debt traps.

For instance, one local nonprofit partnered with Phoenix community colleges to offer free evening classes on budgeting, debt repayment, and banking options. Participants reported a 40% drop in payday loan use within a year.

Real-life testimonies include parents who shifted from using payday loans for school supplies to setting up small, automatic savings transfers from their paychecks. This demonstrates that education isn’t just about awareness — it’s about building confidence to choose better financial tools.

The Future of Payday Lending in Phoenix

The payday loan industry in Phoenix is evolving alongside technology and changing regulations. The rise of fintech alternatives — such as earned wage access apps, peer-to-peer lending platforms, and AI-powered credit evaluations — could gradually reduce demand for traditional payday loans.

At the same time, political momentum for tighter consumer protection laws may further restrict high-interest lending in Arizona. If these trends continue, the next decade could see a significant shift toward more affordable, transparent short-term lending products in Phoenix.

However, until such changes fully take root, payday loans will likely remain a go-to option for many residents facing urgent cash needs. Borrowers who stay informed about their rights, explore alternatives, and plan repayment strategies will be best positioned to navigate this changing financial landscape without falling into costly debt cycles.

Frequently Asked Questions: Payday Loans in Phoenix

1. Are payday loans legal in Phoenix, Arizona?

Payday loans, in the traditional sense, are largely restricted in Arizona due to interest rate caps. However, lenders still offer similar high-cost short-term products like title loans and flex loans. These loans often carry APRs exceeding 100%, so it’s important to read the fine print and understand the total repayment cost.

2. How quickly can I get a payday loan in Phoenix?

Most payday loan alternatives in Phoenix can be approved within minutes and funded the same day. Online lenders may deposit funds into your bank account in as little as one business day, while some storefront lenders provide cash immediately after approval.

3. What’s the maximum amount I can borrow?

Loan limits depend on the lender and type of loan. Payday loan-style products in Phoenix usually range from $100 to $2,500, but larger title loans may exceed that. Always borrow only what you can repay without sacrificing essential expenses like rent or utilities.

4. What happens if I can’t repay on time?

Failing to repay on time can result in additional fees, increased interest, and potential legal action. Some lenders may also withdraw funds directly from your bank account, leading to overdraft fees. Communicating with your lender before missing a payment can sometimes help you arrange an extension or alternative repayment plan.

5. Do payday loans in Phoenix require a credit check?

Many short-term lenders in Phoenix advertise “no credit check” loans, meaning they focus more on income verification than credit history. However, your repayment behavior may still be reported to credit bureaus, affecting your credit score if payments are missed.

6. What are safer alternatives to payday loans in Phoenix?

Consider credit union small-dollar loans, personal loans from online lenders, borrowing from friends or family, or using earned wage access apps. Nonprofits in Phoenix also offer emergency assistance programs for qualified residents.

7. Can I get a payday loan online in Phoenix?

Yes, online lenders operate statewide, offering similar services to physical storefronts. The benefit is convenience, but borrowers should verify that the lender is licensed in Arizona and operates within state lending laws.

8. How can I avoid payday loan scams in Phoenix?

Stick to licensed lenders, check for physical office addresses, and avoid lenders who demand upfront fees or pressure you to sign quickly. The Arizona Attorney General’s website lists approved lenders and consumer alerts.

9. Are there nonprofit organizations that can help with payday loan debt?

Yes, groups like Take Charge America and local Phoenix credit counseling agencies offer debt management programs, budget coaching, and negotiation with lenders to reduce interest and fees.

10. Will paying off my payday loan early save me money?

In most cases, yes. Many payday loan contracts calculate fees based on the length of the borrowing term, so paying early can reduce the total cost. Always check your loan agreement to confirm if early repayment penalties apply.