Is a Home Equity Loan a Second Mortgage?

When you’re a homeowner, your house isn’t just a place to live—it’s also a significant financial asset. Owning property can be a powerful tool for financial planning and wealth accumulation. You might have heard terms like “home equity loan” or “second mortgage” tossed around, especially if you’re considering borrowing against your home. But what do these terms mean, and are they the same thing?

In this article, we’ll delve into the differences and similarities between home equity loans and second mortgages, how they function, and how they might benefit you.

Understanding Home Equity

Before diving into loans and mortgages, it’s essential to understand what home equity is. Home equity represents the portion of your property that you truly “own.” It’s a valuable asset that grows over time as you pay down your mortgage and your property’s value appreciates.

Calculating Home Equity

Home equity is calculated by subtracting the amount you owe on your mortgage from the current market value of your home. This simple equation gives you an insight into your financial stake in the property. For instance, if your home is worth $300,000 and you still owe $200,000 on your mortgage, your home equity is $100,000.

Building Home Equity

Building home equity can occur in several ways. Primarily, it increases as you make regular mortgage payments, reducing the principal balance. Additionally, any appreciation in property value contributes to an increase in equity, driven by factors like local real estate market trends and improvements made to the property.

Utilizing Home Equity

This equity serves as a significant resource, particularly when funds are required for major expenses such as home renovations, education, or debt consolidation. Grasping how to utilize this asset can offer financial flexibility, enabling you to meet both anticipated and unforeseen financial requirements.

What is a Home Equity Loan?

A home equity loan allows you to borrow a lump sum of money against the equity in your home. It operates much like a standard loan—you receive a large sum upfront and then pay it back over time with interest. Understanding its mechanics can help you assess whether it aligns with your financial goals.

Key Features of Home Equity Loans

Home equity loans come with several defining features that make them distinct financial instruments:

- Fixed Interest Rates: Most home equity loans come with a fixed interest rate, meaning your monthly payments remain consistent throughout the loan’s term. This stability can be advantageous for budgeting and long-term financial planning.

- Set Repayment Period: You typically have a set period, often ranging from 5 to 30 years, to repay the loan. This structured timeline provides a clear framework for financial commitment, allowing you to plan accordingly.

- Lump Sum Payment: You receive the entire loan amount at once, making it ideal for large expenses. This can be particularly beneficial when funding substantial projects or consolidating high-interest debts.

Advantages of Home Equity Loans

Home equity loans can be a practical option if you need a predictable payment plan and a specific amount of money. They offer the advantage of clear financial terms and conditions, which can be reassuring for borrowers looking for certainty in their financial transactions.

Considerations Before Taking a Home Equity Loan

While they offer benefits, it’s crucial to assess your ability to meet the financial obligations associated with a home equity loan. Evaluating your income stability, existing debts, and future financial commitments is vital to ensure that taking on this additional debt aligns with your broader financial strategy.

Is a Home Equity Loan a Second Mortgage?

Yes, a home equity loan is indeed considered a second mortgage. Understanding this classification helps clarify how these financial products fit into the broader landscape of home financing.

What is a Second Mortgage?

A second mortgage is any loan taken out on a property that’s already mortgaged. When you take out your initial loan to buy a home, that’s your first mortgage. Any subsequent loan secured against your home’s equity is a second mortgage.

Why Home Equity Loans Are Second Mortgages

Since a home equity loan uses your home as collateral and is secondary to your first mortgage, it falls under the category of a second mortgage. This secondary position in the hierarchy of claims means that in the event of a foreclosure, the first mortgage gets priority for repayment.

Risks and Considerations for Second Mortgages

It’s important to note that a second mortgage, including a home equity loan, poses a higher risk to lenders than a first mortgage. If you default, the first mortgage gets paid off first, and the second mortgage is paid afterward from any remaining funds. This increased risk often results in higher interest rates compared to primary mortgages.

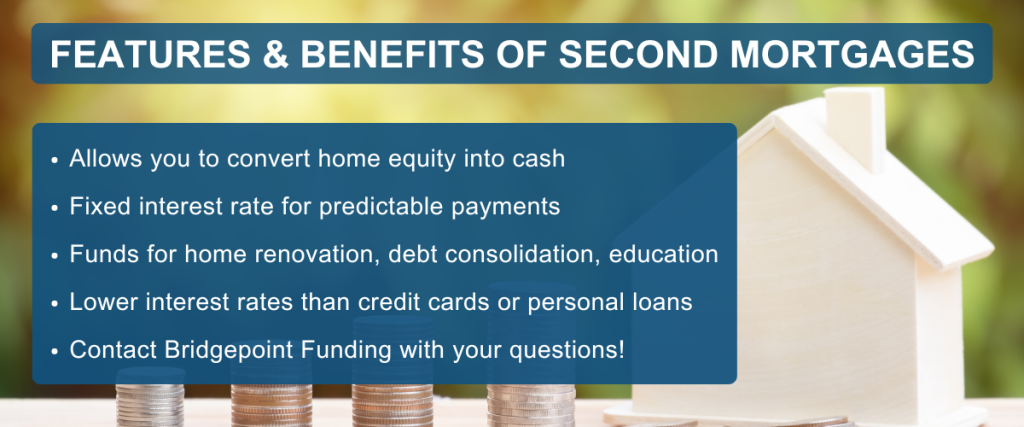

Benefits of Home Equity Loans as Second Mortgages

Home equity loans offer several benefits, especially when used wisely. Leveraging these advantages can enhance your financial strategy and provide valuable resources for major expenses.

Access to Large Sums of Money

Home equity loans provide access to a significant amount of money based on your home’s equity, which can be especially useful for major expenses. This can include home renovations, medical expenses, or significant life events like weddings or educational funding.

Predictable Payments

With fixed interest rates, home equity loans offer the advantage of predictable monthly payments, helping you manage your budget better. This stability is particularly beneficial for individuals seeking long-term financial predictability.

Potential Tax Benefits

In some cases, the interest paid on home equity loans may be tax-deductible, particularly if the loan is used to improve your home. However, it’s crucial to consult a tax advisor to understand your specific situation. This potential deduction can enhance the financial appeal of a home equity loan.

Strategic Financial Planning

Using a home equity loan strategically can be part of a broader financial plan, allowing you to allocate resources efficiently. Whether you’re consolidating high-interest debt or investing in property improvements, these loans can be a tool for achieving financial objectives.

Risks Associated with Home Equity Loans

While home equity loans have advantages, they also come with risks. Understanding these risks is crucial for making informed financial decisions and avoiding potential pitfalls.

Risk of Foreclosure

Since your home is collateral for the loan, failing to make payments could result in foreclosure. This severe consequence underscores the importance of ensuring you can afford the loan payments before proceeding. It’s vital to maintain a realistic view of your financial capabilities.

Increasing Debt

Taking out a home equity loan increases your overall debt. It’s crucial to use the funds wisely and avoid borrowing more than you can repay. Carefully consider the necessity and utility of the expenses you plan to cover with the loan to prevent financial strain.

Fees and Closing Costs

Just like your initial mortgage, home equity loans may come with fees and closing costs. These can add up, so it’s important to factor them into your decision. Understanding the full financial implications, including these additional costs, helps in making an informed choice.

Impact on Long-term Financial Health

Taking on additional debt can have long-term implications for your financial health, affecting your credit score and future borrowing capacity. Thoroughly assessing these potential impacts is essential for maintaining a balanced financial portfolio.

Alternatives to Home Equity Loans

If a home equity loan doesn’t seem like the right fit, there are alternatives that might suit your financial needs better. Exploring these options can provide flexibility and align with your financial goals.

Home Equity Line of Credit (HELOC)

A HELOC is similar to a home equity loan but operates more like a credit card. You can borrow against your home equity up to a certain limit and pay interest only on the amount you borrow. This option offers flexibility for ongoing expenses, making it suitable for projects with variable costs.

Cash-Out Refinance

This involves refinancing your existing mortgage for more than you owe and taking the difference in cash. It’s a way to access your home equity without taking out a separate loan. This approach can consolidate your debt under one mortgage, potentially at a lower interest rate.

Personal Loans

For those who prefer not to use their home as collateral, personal loans offer an unsecured alternative. While they typically have higher interest rates, they do not put your home at risk, providing peace of mind for borrowers concerned about asset security.

Reverse Mortgage

For homeowners aged 62 or older, a reverse mortgage allows you to convert part of your home equity into cash without selling your home. This option can provide financial relief for retirees looking to supplement their income without incurring monthly payments.

Conclusion

Home equity loans are indeed a form of second mortgage, providing a way to tap into your home’s value for significant expenses. While they offer benefits like predictable payments and potential tax advantages, they also come with risks, including the possibility of foreclosure.

Carefully consider your financial situation, the purpose of the loan, and explore alternatives before deciding. Whether you choose a home equity loan or another option, understanding these financial tools can help you make informed decisions that align with your financial goals. Making the right choice involves balancing immediate needs with long-term financial health, ensuring your decisions support your overarching financial strategy.