Mortgage Insurance with a VA Loan

A VA loan is a mortgage option available to veterans, active-duty service members, and some military spouses. These loans are provided by private lenders but are partially guaranteed by the Department of Veterans Affairs. This guarantee protects lenders and often allows them to provide more favorable terms, such as no down payment and no requirement for private mortgage insurance (PMI).

The Role of the Department of Veterans Affairs

The Department of Veterans Affairs plays a crucial role in facilitating VA loans. By providing a partial guarantee, the VA reduces the risk for lenders, encouraging them to offer competitive terms. This involvement not only makes homeownership more accessible for veterans but also helps stabilize the housing market by ensuring veterans have reliable access to credit.

Private Lenders and VA Loans

Although the VA backs these loans, they are actually issued by private lenders such as banks and mortgage companies. This means that while the VA sets certain standards and guarantees a portion of the loan, the specific terms and interest rates can vary depending on the lender. It’s essential for borrowers to shop around and compare offers from different lenders to secure the best deal.

The Unique Structure of VA Loans

VA loans are structured to provide maximum benefits to veterans. Unlike conventional loans, VA loans require no down payment, which can be a significant barrier for first-time homebuyers. The absence of PMI further reduces the cost of borrowing, allowing veterans to allocate their financial resources more effectively. This unique structure is designed to honor the service of veterans by facilitating their transition into civilian life with greater financial security.

Key Benefits of VA Loans

VA loans come with a range of benefits that can make homeownership more attainable for veterans.

No Down Payment

One of the most appealing features of a VA loan is the ability to purchase a home without a down payment. This is a significant advantage over conventional loans, which typically require a substantial upfront payment. For many veterans, saving for a down payment can be a hurdle to homeownership, and the VA loan eliminates this obstacle, enabling them to invest in a home sooner.

No Private Mortgage Insurance (PMI)

Conventional loans often impose PMI on borrowers who make a down payment of less than 20%. This insurance can add hundreds of dollars to monthly mortgage payments. However, with a VA loan, PMI is not required, thanks to the VA’s guarantee. This can result in substantial savings over the life of the loan, making homeownership more affordable for veterans.

Competitive Interest Rates

VA loans typically offer lower interest rates than conventional loans. This is partly due to the reduced risk for lenders, thanks to the VA’s backing. Lower interest rates mean lower monthly payments and less interest paid over the life of the loan, translating into significant savings. Veterans can benefit from these competitive rates, enhancing their financial stability.

Flexible Credit Requirements

VA loans are known for their more lenient credit requirements. While lenders may still have minimum credit score thresholds, they tend to be more accommodating compared to conventional loans. This flexibility makes it easier for veterans with less-than-perfect credit to qualify for a mortgage, providing them with an opportunity to build or rebuild their credit while securing a home.

Mortgage Insurance and VA Loans

Mortgage insurance is a common requirement for many loan types but not for VA loans.

What is Mortgage Insurance?

Mortgage insurance is a type of protection for lenders in case a borrower defaults on their loan. For most conventional loans with less than a 20% down payment, lenders require borrowers to pay for PMI. This insurance is designed to reduce the risk to lenders, but it adds an extra cost to the borrower.

The Cost of Mortgage Insurance

The cost of PMI can vary depending on the size of the loan and the down payment amount. Typically, PMI costs range from 0.3% to 1.5% of the original loan amount per year. This can add a significant amount to the monthly mortgage payment. Over time, these additional costs can accumulate, making the overall cost of homeownership more expensive for borrowers.

Why VA Loans Don’t Require Mortgage Insurance

VA loans are unique because they don’t require mortgage insurance, thanks to the VA’s partial guarantee of the loan. This guarantee reduces the risk for lenders, allowing them to offer loans without the need for PMI. Consequently, VA borrowers can enjoy lower monthly payments without the added cost of insurance.

The Financial Impact of No Mortgage Insurance

The absence of PMI can have a significant financial impact on VA loan borrowers. Without the added insurance cost, borrowers can allocate more of their budget toward other financial goals, such as saving for retirement or investing in home improvements. This financial flexibility is one of the reasons why VA loans are so popular among eligible veterans and service members.

VA Loan Rates

VA loan rates can vary based on several factors, including the lender, your credit score, and the overall financial climate. However, VA loans generally offer some of the most competitive rates available.

Factors Influencing VA Loan Rates

Several factors can influence the interest rates on VA loans, impacting the overall cost of borrowing.

Credit Score

While VA loans are more forgiving when it comes to credit scores, having a higher score can still help you secure a better interest rate. Lenders use credit scores as an indicator of financial reliability, and a higher score can result in lower interest rates. Veterans are encouraged to maintain good credit practices to take full advantage of the competitive rates offered by VA loans.

Loan Duration

The term of your loan can affect the rate. Typically, shorter loan terms come with lower interest rates. This is because shorter loans pose less risk to lenders and result in a faster return on investment. Borrowers should weigh the benefits of lower rates against the higher monthly payments that shorter terms may require.

Market Conditions

Economic factors and market conditions can influence mortgage rates. It’s important to keep an eye on these trends when considering a VA loan. Interest rates can fluctuate based on changes in the economy, inflation rates, and the Federal Reserve’s monetary policy. Staying informed about market conditions can help borrowers time their loan applications to secure the best rates available.

Lender Policies

Different lenders may offer different rates, so it’s wise to shop around and compare offers. Each lender may have unique policies and rate structures, which can impact the overall cost of the loan. Veterans should consider obtaining quotes from multiple lenders to ensure they receive the most favorable terms for their VA loan.

Comparing VA Loan Rates

When comparing VA loan rates, borrowers should consider not only the interest rate but also the overall cost of the loan, including any fees and closing costs. It’s crucial to evaluate the annual percentage rate (APR), which provides a more comprehensive picture of the loan’s cost. Taking the time to compare offers can lead to substantial savings over the life of the loan.

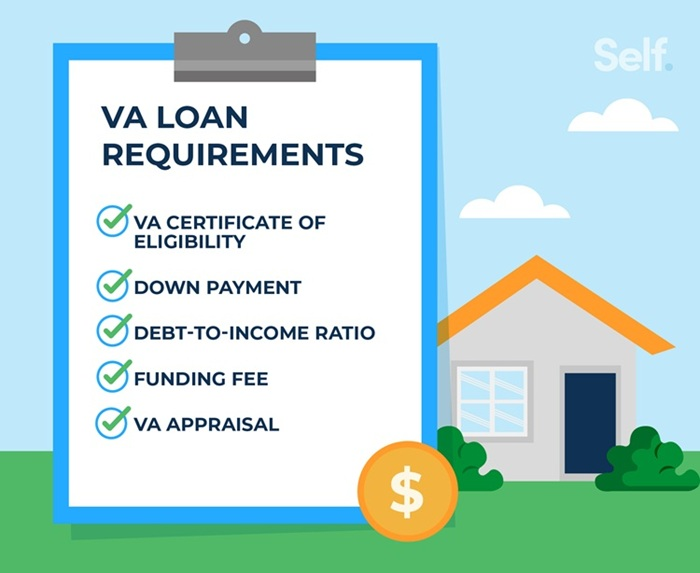

VA Loan Requirements

To qualify for a VA loan, you must meet certain eligibility criteria set by the Department of Veterans Affairs.

Basic Eligibility Requirements

VA loans have specific eligibility requirements that potential borrowers must meet.

Service Requirements

You must be a veteran, active-duty service member, or part of the National Guard or Reserves. The length of your service or service commitment, duty status, and character of service determine your eligibility. These requirements ensure that the benefits of VA loans are extended to those who have served honorably and meet the necessary service criteria.

Certificate of Eligibility (COE)

To prove your eligibility, you’ll need a COE from the VA. This document confirms to the lender that you qualify for a VA-backed loan. Obtaining a COE is a crucial step in the VA loan process, and it can be requested through the VA’s eBenefits portal or by submitting a request form to the VA. Lenders often assist borrowers in obtaining this document.

Income and Credit

While the VA doesn’t set a minimum credit score, lenders typically have their own requirements. Additionally, you must have a stable income and meet the lender’s debt-to-income ratio guidelines. These financial criteria ensure that borrowers can afford their mortgage payments and maintain financial stability throughout the loan term.

The VA Funding Fee

Although VA loans don’t require mortgage insurance, there is a VA funding fee. This one-time fee helps to offset the cost of the VA loan program and is required for most borrowers. The amount of the fee varies based on factors such as your down payment and whether you’ve used a VA loan before.

Purpose of the VA Funding Fee

The VA funding fee is designed to reduce the burden on taxpayers by helping fund the VA loan program. It ensures that veterans continue to benefit from favorable loan terms without imposing additional costs on the general public. This fee is a small price to pay for the numerous advantages that VA loans offer.

Calculating the VA Funding Fee

The VA funding fee is calculated as a percentage of the loan amount and can vary depending on the borrower’s circumstances. Factors such as military category, down payment amount, and whether it’s a first-time or subsequent use of a VA loan can influence the fee. Understanding how this fee is calculated can help borrowers plan their finances and anticipate the overall cost of their loan.

Exemptions from the VA Funding Fee

Certain veterans may be exempt from paying the VA funding fee. Veterans receiving disability compensation for a service-connected disability, surviving spouses of veterans who died in service or from a service-connected disability, and certain other individuals may qualify for an exemption. It’s important for eligible borrowers to explore these exemptions to minimize their loan costs.

Is a VA Loan Right for You?

Deciding whether a VA loan is the best option depends on your personal circumstances. Here are some considerations:

Cost Savings

If avoiding a down payment and PMI is important to you, a VA loan could be an excellent choice. The financial benefits of a VA loan can significantly reduce the upfront and ongoing costs of homeownership, making it a cost-effective option for eligible borrowers. Evaluating your financial situation and long-term goals can help you determine if the cost savings associated with a VA loan align with your needs.

Flexibility

VA loans offer flexibility in terms of credit requirements and down payments, which can be beneficial for many borrowers. This flexibility allows veterans with varying financial backgrounds to access homeownership opportunities that might otherwise be out of reach. Considering your credit history and financial circumstances can help you assess whether a VA loan’s flexibility meets your needs.

Long-Term Plans

Consider your long-term plans and whether you’ll stay in the home long enough to benefit from a VA loan’s advantages. VA loans are ideal for those planning to remain in their homes for an extended period, as the cost savings and favorable terms become more pronounced over time. Assessing your future plans and housing needs can guide your decision on whether a VA loan aligns with your long-term objectives.

Exploring Alternatives

While VA loans offer numerous benefits, it’s important to explore alternative mortgage options to ensure you’re making the best decision for your circumstances. Conventional loans, FHA loans, and other mortgage products may offer different advantages based on your financial profile. Consulting with a mortgage professional can provide valuable insights into the best mortgage option for your needs.

Conclusion

VA loans offer numerous benefits, including the absence of mortgage insurance, which can lead to significant savings. By understanding the requirements and benefits of a VA loan, you can make an informed decision about whether it’s the right mortgage option for you.

If you’re eligible, a VA loan can be a powerful tool in your journey to homeownership, offering competitive rates, no PMI, and flexible terms that make purchasing a home more accessible. These advantages not only honor the service of veterans but also provide them with the financial resources to achieve their homeownership dreams.

As always, it’s important to do your research and consider speaking with a financial advisor or mortgage professional to explore all your options and find the best solution for your needs. An informed decision can lead to long-term financial stability and the realization of your homeownership goals.