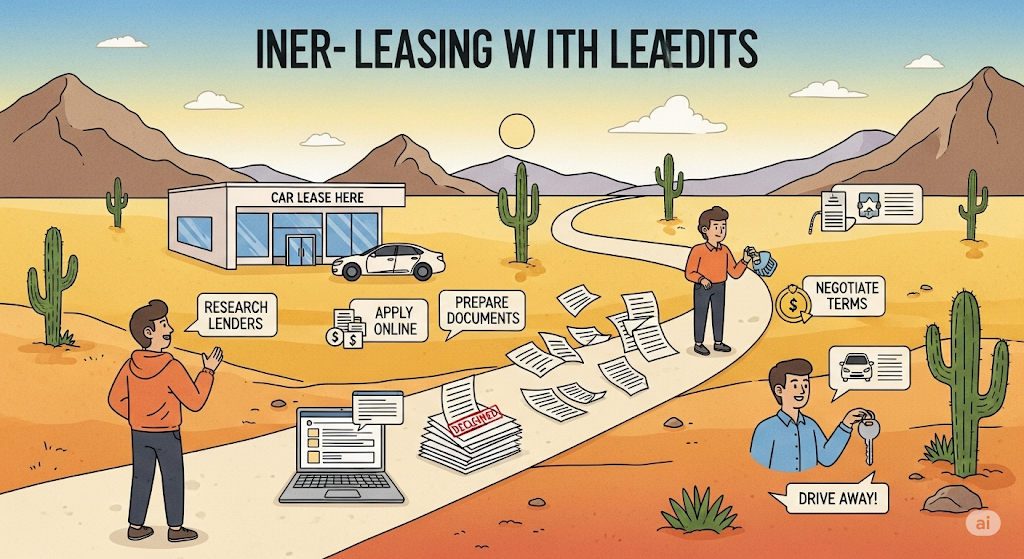

How to Lease a Car with Bad Credit: A Complete 2025 Guide

How to Lease a Car with Bad Credit: A Complete 2025 Guide Table of Contents Introduction If you’re struggling with a low credit score but still need reliable transportation, you may be wondering if leasing a car with bad credit is even possible. The short answer? Yes—but with a few hurdles. While many car leases […]

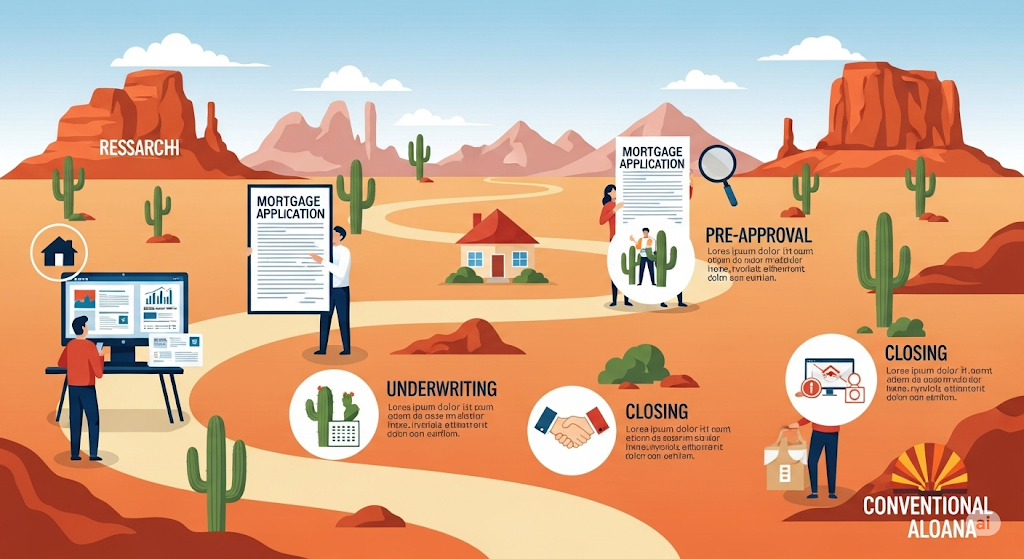

Conventional Loans in Arizona: What You Need to Know in 2024

If you’re thinking about buying a home in Arizona, chances are you’ve come across the term “conventional loan.” But what exactly is a conventional mortgage, and how does it work in the Grand Canyon State? In this comprehensive guide, we’ll explain how conventional loans in Arizona work, eligibility requirements, loan limits, pros and cons, and […]

Car Loan After Bankruptcy: How to Rebuild and Get Back on the Road

Filing for bankruptcy is a major financial decision—and one that can significantly impact your credit profile. But it’s not the end of your financial journey. In fact, many people find that they can qualify for a car loan surprisingly soon after bankruptcy, especially with the right strategy. Whether you’re coming out of Chapter 7 or […]

Best Instant Loan Apps in UAE (2024 Guide)

Best Instant Loan Apps in UAE (2024 Guide) Best Instant Loan Apps in UAE (2024 Guide) The demand for quick, hassle-free financial assistance has grown rapidly in the UAE. Whether it’s for unexpected medical bills, travel plans, or temporary cash shortages, instant loan apps in the UAE offer a fast and convenient solution. These apps […]

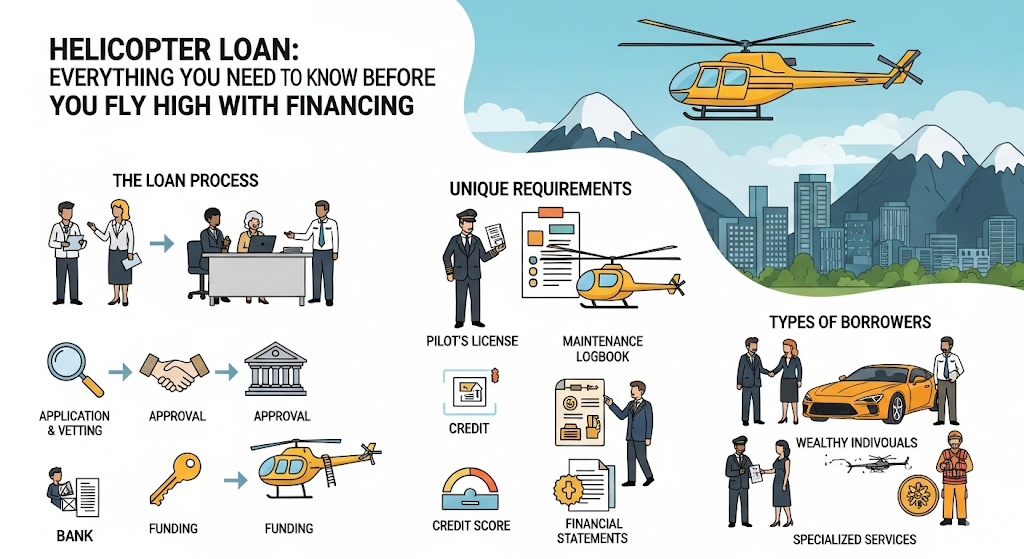

Helicopter Loan: Everything You Need to Know Before You Fly High with Financing

Table of Contents 1. Introduction Helicopters are no longer just for military or billionaires. With increased availability and varied models, private individuals, corporations, medical institutions, and law enforcement agencies are increasingly turning to helicopters for both leisure and work purposes. However, helicopters come with a hefty price tag. That’s where helicopter loans come into play. […]

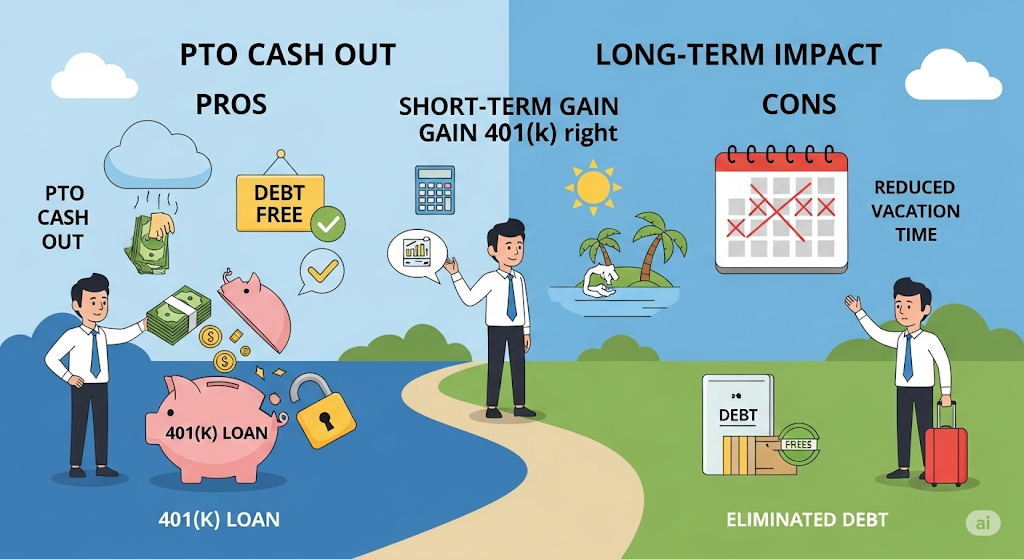

Can You Cash Out PTO to Pay Off a 401(k) Loan? Your Complete 2025 Guide

Can You Cash Out PTO to Pay Off a 401(k) Loan? Your Complete 2025 Can You Cash Out PTO to Pay Off a 401(k) Loan. Your Complete 2025 Guide Feeling overwhelmed by your 401(k) loan payments? Many working professionals wonder if they can cash out accrued PTO (paid time off) to cover that loan and […]

Heter ISKA Loans: A Complete Guide for Faith-Based Financing

Heter ISKA Loans: A Complete Guide Table of Contents 1. Introduction In times of financial stress, some people turn to quick-fix lending solutions such as title loans. Among these, a “discount title loan” might sound like a more affordable version—but what does that really mean? Are you getting a deal, or just dressing up a […]

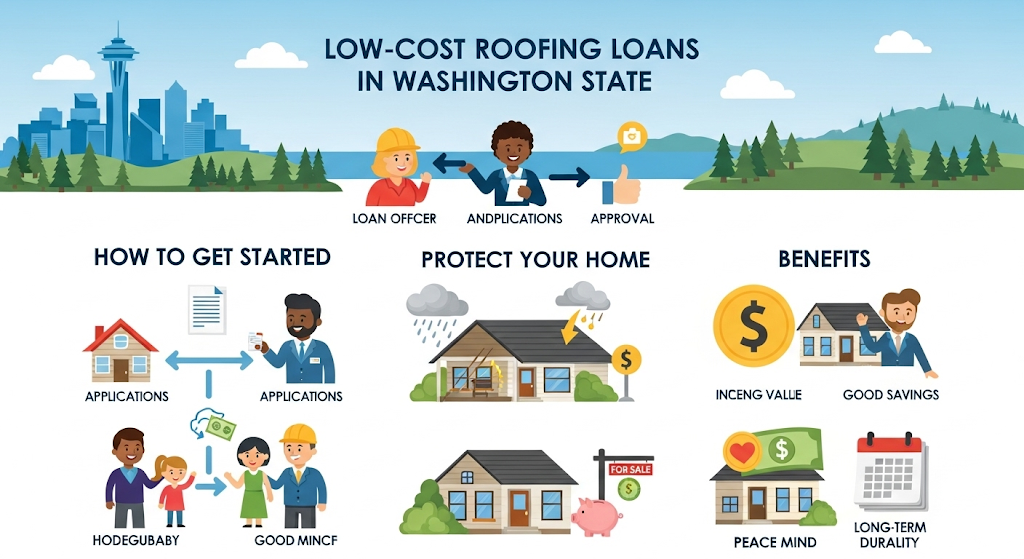

Low-Cost Roofing Loans in Washington State: How to Protect Your Home Without Breaking the Bank

Introduction Low-Cost Roofing Loans in Washington State Is your roof aged, damaged, or leaking—but your wallet can’t handle a full cash payment? Good news: Washington State offers multiple low-cost loan and grant solutions to help homeowners finance roof repairs or replacements affordably, even if you have limited savings or poor credit. In this all‑inclusive 2025 […]

Discount Title Loan: Everything You Need to Know Before You Borrow

Table of Contents 1. Introduction In times of financial stress, some people turn to quick-fix lending solutions such as title loans. Among these, a “discount title loan” might sound like a more affordable version—but what does that really mean? Are you getting a deal, or just dressing up a high-risk loan in a friendlier name? […]

Auto Bankruptcy Loan

Auto Bankruptcy Loan: Auto Bankruptcy Loan Facing bankruptcy—whether Chapter 7 or Chapter 13—is stressful, especially when you still need a reliable vehicle. But here’s the good news: you can still get an auto loan after bankruptcy, even with less-than-perfect credit. By understanding your options, smart strategies, and realistic expectations, you can rebuild credit, minimize costs, […]