Can You Cash Out PTO to Pay Off a 401(k) Loan? Your Complete 2025

Can You Cash Out PTO to Pay Off a 401(k) Loan. Your Complete 2025 Guide Feeling overwhelmed by your 401(k) loan payments? Many working professionals wonder if they can cash out accrued PTO (paid time off) to cover that loan and reduce financial stress. It sounds like a smart shortcut—but is it really a smart strategy?

In this in-depth guide, we’ll explore every angle:

- IRS rules around PTO cash‑out

- How 401(k) loans work and their hidden costs

- Tax implications, risks, and constructive receipt concerns

- Real‑world scenarios where it might (or might not) make sense

- Safer alternatives and smart financial habits to rebuild retirement security

By the end, you’ll know exactly whether cashing PTO to pay off a 401(k) loan is a clever move—or a costly decision.

1. How 401(k) Loans Really Work

- The IRS allows borrowing up to 50% of your vested balance or $50,000, whichever is lower. Repayment typically must occur within five years unless used for a primary residence purchase.

- Interest is repaid to your own account, making it seem attractive—but you’re missing out on returns your money could have earned.

- Notably, if you leave your job, any remaining balance is treated as a taxable distribution—and often a 10% early withdrawal penalty if you’re under 59½.

- Pros: No credit check, easy funds access, and you “pay interest to yourself.”

- Cons: Loss of investment compounding, possible double taxation, and risk of penalties if terms aren’t met.

2. What You Need to Know About Cashing Out PTO in 2025

- Some employers allow PTO cash‑out at resignation, partial payout each year, or under hardship conditions—but each plan differs.

- IRS rules require written, irrevocable election before the year the PTO is earned to avoid triggering “constructive receipt” and premature taxation.

- Without proper structuring, just being eligible to cash PTO—even if you don’t—can lead to taxable income under IRS doctrine.

- Make sure you understand how your employer’s policy handles taxes, and ensure compliance to avoid unintended tax liabilities.

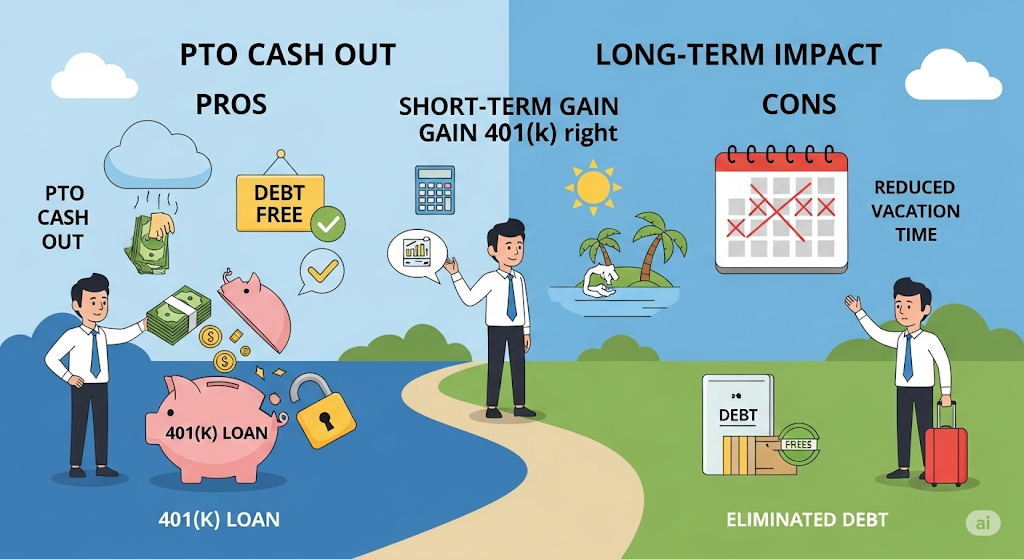

3. Why You Might Consider Using PTO to Pay Off a 401(k) Loan

✅ Benefits

- Provides a lump sum you could immediately apply to loan principal.

- Helps avoid extended interest payments and speeds up repayment.

- Clears emotional and financial burden quickly.

⚠️ Risks

- You’ll forgo future compounding growth on your PTO earnings.

- The cash-out amount is likely taxed just like regular wages.

- If your employer mismanages the PTO policy, it may trigger IRS penalties or misreporting.

- You still lose investment growth from cashing PTO rather than keeping the loan balance intact.

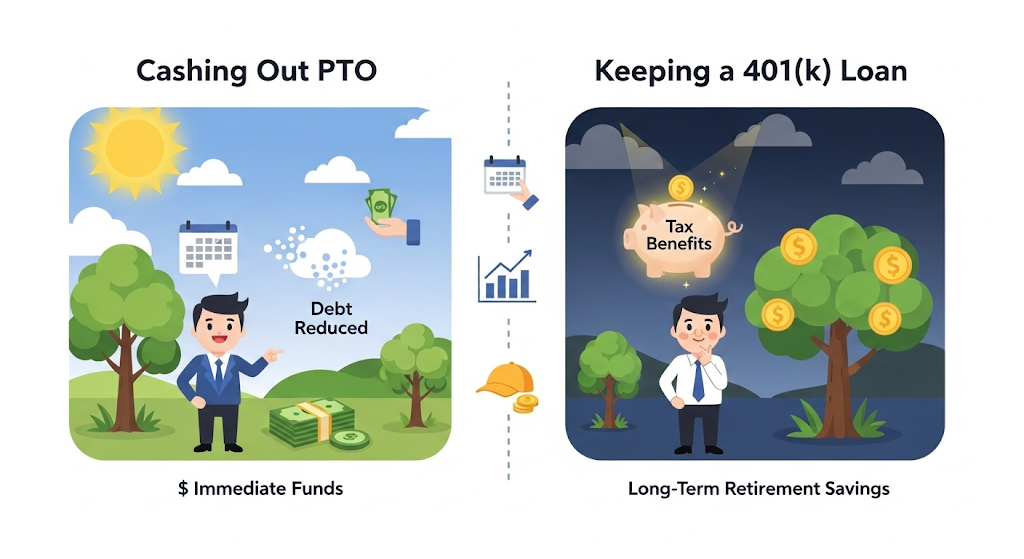

4. Comparison: Cashing Out PTO vs. Keeping the 401(k) Loan

| Option | Pros | Cons |

|---|---|---|

| Cashing out PTO | Quick influx of cash, easier to repay loan | Taxed as income, reduces PTO balance, forgiveness rare |

| Continue paying 401(k) loan | Interest paid to yourself, preserves PTO | Missed investment growth, limited cash liquidity |

| Alternative funding sources | Avoid tapping retirement or PTO | May involve interest or credit qualifying |

5. Real-World Scenarios & Emotional Triggers

Scenario 1: Single Parent Needing Relief

“I was late on payments and stressed about default. Cashed PTO to wipe out the loan—felt immediate relief.”

Scenario 2: Career Transitioner Without Emergency Fund

“With a new job lined up, I opted to cash out PTO to close the loan before payroll changed. Peace of mind worth the tax hit.”

While both people found relief, they sacrificed long-term savings and may have reduced future PTO or emergency time.

6. Alternatives to Cashing PTO

Before you tap PTO:

- Consider emergency savings or personal lines of credit for flexibility.

- Explore a personal loan or hardship distribution if eligible by IRS standards.

- Negotiate with your employer or loan administrator for temporary payment relief or adjusted installment schedules.

- Use budgeting tools to reduce spending and accelerate repayment from regular income—avoiding tapping either PTO or retirement.

7. Tax & Legal Considerations to Watch

- Tax Withholding: PTO cash-out is typically taxed like wages—subject to payroll tax, income tax.

- Constructive Receipt: If policy allows cash-out anytime, even without you requesting, you may be taxed regardless.

- Plan Election: Proper elections must be made before the PTO is earned to avoid IRS penalties. Employers must design policies carefully to remain compliant.

- 401(k) Loan Default: If repaid using PTO and leaving job, ensure loan is fully satisfied to avoid distribution penalties and taxes.

8. Expert Tips for a Safer Strategy

- Confirm your PTO cash-out policy and election windows well in advance.

- Estimate taxes and net payout before deciding—don’t assume full value.

- Pay off 401(k) loan in full if you leave your employer to avoid default penalties.

- If you’re under 59½ and consider hardship withdrawal instead, verify it qualifies under 401(k) regulations.

- Resume contributions ASAP after completing the loan to rebuild retirement momentum.

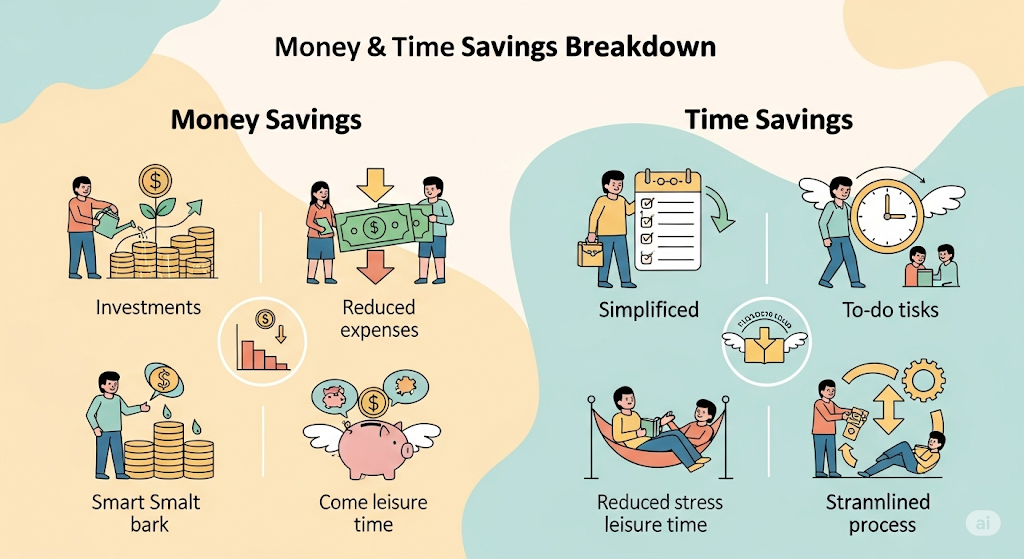

9. Money & Time Savings Breakdown

Example Scenario:

- Outstanding loan: $5,000

- PTO payout amount: $6,000 gross

- Expected tax/withholdings (~25%) = $1,500

- Net payment = $4,500 (short by $500)

This leaves a shortfall and extinguishes most of your PTO balance—check that you still have vacation available if needed later.

🔟 FAQs: Cashing PTO to Pay Off 401(k) Loan

- Can I legally cash out PTO to pay 401(k) loans?

Depends on your employer’s policy and proper IRS election timelines. - Will cashing out PTO trigger income tax?

Yes—it is taxed as wage income with applicable withholding. - Can unused PTO generate tax liability even if not paid out?

Under “constructive receipt,” yes, if your policy provides unrestricted access. - Is it better to take a loan or hardship withdrawal?

Loans avoid penalties if repaid. Withdrawals are taxed, typically non-repaid, and reserved for emergencies. - What happens if I leave the job after using PTO to clear a 401(k) loan?

If paid fully before exit, you reduce risk. Ensure documentation proves loan is closed. - Are there better alternatives to using PTO?

Yes—consider personal loans, budgeting, support from employer, or emergency savings. - What investment growth am I losing?

The PTO cash net is not invested, and loan repayment interest you pay yourself is less than market returns. - Will my credit score be affected by this strategy?

Neither PTO cash-out nor 401(k) loan affects credit directly. - Can I still make 401(k) contributions while repaying the loan?

That depends on plan rules; some plans restrict contributions during an outstanding loan. - Should I consult a financial advisor?

Absolutely—especially to weigh long-term retirement goals, tax impact, and compare alternatives.

10. Final Thoughts

Cashing out PTO to pay off a 401(k) loan can bring short-term relief—but it comes with real trade-offs:

- Tax implications

- Lost PTO for personal time

- Missed compound growth on retirement funds

Use this strategy only if you:

- Fully understand your employer’s policy

- Have calculated tax impact

- Know the loan will be closed in full before job changes

- Have weighed safer alternatives

Smart planning matters. Focus on rebuilding credit, replenishing PTO, and restoring contributions once the loan is gone. Your future self will thank you.

Need a personal calculator or payoff plan? I can help create a downloadable worksheet or referral to a retirement-savvy financial planner.