Introduction: Why “Guaranteed Approval” Payday Loans Appeal to Bad Credit Borrowers

For millions of Americans, Guaranteed Approval for bad credit score is like a financial scarlet letter. According to Experian’s 2023 Credit Report, over 16% of U.S. consumers have credit scores below 580 — meaning they’re considered very poor by traditional lending standards. For these borrowers, getting a personal loan or credit card is almost impossible.

This is where payday loans with “guaranteed approval” start to sound like a miracle. They promise fast cash, minimal requirements, and no judgment about past mistakes. Imagine this: you’ve got a utility bill due tomorrow, your car’s transmission just failed, and your bank account is barely in the double digits. A bank would take days — maybe weeks — to process a loan, but a payday lender is offering to deposit money in your account within hours.

Why they appeal to bad credit borrowers:

- Speed: Emergencies can’t wait for slow bank processes.

- Accessibility: Lenders focus more on income than credit scores.

- Convenience: Applications take minutes, not hours.

- Hope: The word “guaranteed” creates an emotional promise of certainty.

Example:

Maria, a single mother in El Paso, had her electricity shut-off notice in hand. Her credit score was 530 after a past bankruptcy. A storefront payday lender approved her for $350 within 20 minutes, saving her from days without power. While it solved her immediate crisis, the high repayment cost created stress later — something many borrowers don’t consider up front.

Understanding “Guaranteed Approval” Payday Loans

When payday lenders say guaranteed approval, they’re not actually promising 100% approval rates. U.S. lending laws require some level of applicant verification.

Instead, “guaranteed” typically means:

- High approval rates — 80–95% of applicants who meet basic requirements get approved.

- No traditional credit check — Bad credit is not a major barrier.

- Simple eligibility — Age, income, and bank account are the main factors.

Data:

A survey from the Community Financial Services Association of America (CFSA) found:

- 12 million Americans use payday loans annually.

- About 70% of borrowers have FICO scores under 640.

- 90% of approvals happen without a hard credit check.

Why lenders can approve more people:

Payday loans are secured by your paycheck, not by your credit history. The lender’s main concern is whether they can collect repayment directly from your bank account on your next payday.

Example:

James, a warehouse worker in Dallas with a history of late payments, applied online at 10 a.m. for a $500 payday loan. By 2 p.m., the money was in his checking account. The lender didn’t care about his 515 credit score — they only verified that he earned $1,800 a month and had an active bank account.

How Guaranteed Payday Loans Work for Bad Credit Borrowers

The process is straightforward, and that’s a big reason for their popularity.

Step-by-Step Process:

- Application – Can be completed online or at a storefront in 5–15 minutes.

- Verification – Lender checks your ID, proof of income, and bank account.

- Approval – Often instant if you meet criteria.

- Funding – Direct deposit or cash-in-hand within 24 hours.

- Repayment – Automatically withdrawn from your bank account on payday.

Loan Amounts:

Typically range from $100 to $1,000 depending on state laws. In Texas, there’s no cap on payday loan amounts — but the higher the loan, the bigger the fees.

Data Point:

In Texas, the average payday loan term is 14 days, and the average APR exceeds 400%, according to the Texas Office of Consumer Credit Commissioner.

Example:

Tanya, living in Houston with a credit score of 495, took out a $600 payday loan to cover emergency dental work. The loan fee was $90 for two weeks. When she couldn’t pay on time, she rolled it over — ending up paying $270 in fees over six weeks for the same $600 principal.

The Reality Behind “No Credit Check” Loans

No credit check sounds like a dream for bad credit borrowers, but there’s a nuance. Payday lenders skip hard pulls to major credit bureaus — meaning your score isn’t affected by applying — but they still check other databases.

What they check instead:

- Income consistency – Are you employed or have steady benefits?

- Bank account history – Do you have overdrafts or closed accounts?

- Loan history – They may use databases like Teletrack, Clarity, or DataX to see if you have unpaid payday loans elsewhere.

Why this matters:

If you already have multiple payday loans outstanding, some lenders will reject your application despite advertising “guaranteed approval.”

Statistic:

A 2022 CFPB study found that 1 in 5 payday loan applications are denied due to active unpaid loans in these databases — even when the applicant meets income requirements.

Example:

Robert in Austin thought “no credit check” meant no checks at all. He was denied because a database showed an unpaid $300 payday loan from 8 months ago — proving “guaranteed” is not absolute.

Costs & APRs: The Price of Guaranteed Payday Loans

Payday loans are notorious for high costs, especially for bad credit borrowers who may be considered higher risk.

Typical Fee Structure:

- $15–$20 fee per $100 borrowed (varies by state).

- Short repayment terms — usually 14–30 days.

Calculation:

- Borrow $500

- $15 fee per $100 = $75 fee

- Total repayment: $575 in 14 days

- APR: 391%

Data Point:

According to the CFPB, 80% of payday loans are rolled over or followed by another loan within 14 days — meaning borrowers often pay more in fees than the loan amount.

Example:

Karen in San Antonio borrowed $400 to fix her water heater. She couldn’t repay it on time, rolled it over twice, and ended up paying $180 in fees — nearly half the original loan — without reducing the principal.

Eligibility Criteria Even with Bad Credit

Even if your credit score is low, payday loan lenders still require certain minimum qualifications. The difference is, these requirements are far less strict compared to banks or credit unions.

Standard Eligibility Requirements:

- Age: Must be 18 or older (some states require 19).

- Proof of Income: Pay stubs, bank statements, or benefits statements (e.g., Social Security, disability, unemployment).

- Active Bank Account: Checking account in your name to deposit funds and withdraw repayments.

- Valid Contact Information: A working phone number and email address.

- Residency: Must reside in the state where you are applying.

Data Insight:

According to a Pew Charitable Trusts report, 80% of payday loan borrowers are employed full-time, but 58% live paycheck to paycheck — which means a steady income doesn’t always mean financial stability.

Life Example:

Samuel, a part-time restaurant worker in Phoenix, was approved for a $350 payday loan despite having a 510 credit score. The key? He showed proof of regular income from two jobs and had a valid checking account.

Advantages of Guaranteed Payday Loans for Bad Credit

While the risks are high, there are undeniable reasons why borrowers choose payday loans.

Why Borrowers Choose Them:

- Speed: Approval and funding often occur the same day.

- Accessibility: Even borrowers with bankruptcy or foreclosure in their history can qualify.

- Simplicity: No complicated paperwork or lengthy applications.

- No Collateral: You don’t risk losing property like in title loans.

- Privacy: Online applications keep the process discreet.

Data Insight:

CFSA research shows 42% of payday loan borrowers use the funds for emergency expenses like car repairs or medical bills, while 38% use them for recurring bills such as rent and utilities.

Example:

Claire, a single mother in Houston, faced an urgent $250 daycare bill. With her 520 credit score, a personal loan wasn’t possible. A payday loan gave her immediate relief, avoiding daycare service suspension.

Risks & Downsides to Consider

Before rushing to apply, you must fully understand the potential pitfalls.

Primary Risks:

- High APRs: Often exceeding 300–500% annually.

- Debt Trap Potential: Rolling over loans leads to mounting fees.

- Overdraft Fees: Automatic withdrawals can cause bank overdrafts.

- Short Repayment Terms: Usually 14–30 days, leaving little room to recover.

Data Insight:

The Consumer Financial Protection Bureau found that 70% of payday loan borrowers take out a second loan within a month, and 1 in 5 default on their payday loan.

Example:

Alex in Dallas borrowed $500 for urgent car repairs but couldn’t repay on time. After two rollovers, he owed $850 — $350 more than the original loan amount.

Avoiding Payday Loan Scams

Bad credit borrowers are prime targets for fraudulent lenders because they’re desperate for approval.

Signs of a Scam:

- Requests for upfront payments before loan disbursement.

- No verifiable physical address or license number.

- High-pressure tactics urging immediate commitment.

- Communication only via unsecured channels (e.g., personal email, social media).

How to Protect Yourself:

- Verify the lender with your state’s regulatory agency.

- Use the CFPB lender database to confirm legitimacy.

- Avoid lenders that refuse to provide a written loan agreement.

Example:

Lori in San Diego received an email promising “guaranteed $1,000 loan” with no documents required — only a $50 processing fee upfront. She paid, but never received the loan.

Online vs Storefront Guaranteed Payday Loans

Payday loans come in two main forms — online and storefront — each with unique advantages and drawbacks.

Online Payday Loans

- Pros:

- Apply 24/7 from anywhere.

- Fast digital approval.

- No need to visit a physical location.

- Cons:

- Potential for unlicensed lenders.

- Risk of data breaches if not secure.

Storefront Payday Loans

- Pros:

- Face-to-face customer service.

- Immediate cash payout.

- Easier to verify legitimacy.

- Cons:

- Limited business hours.

- Travel required.

Data Insight:

A 2023 LendingTree survey found 62% of payday loan borrowers now choose online lenders for convenience, but 38% still prefer storefronts for the personal interaction.

Example:

Juan in El Paso chose an online payday lender for a $300 loan while working a night shift. His friend Maria preferred a local storefront because she wanted to discuss repayment options in person.

Alternatives to Guaranteed Payday Loans for Bad Credit Borrowers

Even if payday loans seem like the fastest option, there are often safer and more affordable alternatives that bad credit borrowers can explore.

Common Alternatives:

- Credit Union Payday Alternative Loans (PALs): Offered at APRs under 28%, with terms up to 6 months.

- Small Personal Loans: Some online lenders offer small loans ($500–$1,000) with flexible repayment plans.

- Borrowing from Friends/Family: Interest-free and avoids fees (but requires trust).

- Negotiating with Bill Collectors: Many utility companies and medical providers offer payment plans without interest.

- Side Income: Gig work or selling unused items to raise quick funds.

Data Insight:

The National Credit Union Administration reported in 2022 that borrowers using PALs saved an average of $360 annually compared to payday loan customers.

Example:

Derrick in Atlanta avoided a $450 payday loan by joining a local credit union and taking out a PAL for the same amount. His total cost over two months was just $15 in fees.

When a Payday Loan Makes Sense — and When to Avoid It

Payday loans aren’t inherently “bad” — the problem is in how and when they’re used.

When They Make Sense:

- True Emergencies: Medical bills, urgent car repairs, preventing eviction.

- Short-Term Cash Gap: When you’re certain you can repay on your next payday.

When to Avoid:

- Covering non-essential purchases like vacations or luxury items.

- Repaying another payday loan — this leads to a dangerous rollover cycle.

- When you don’t have a repayment plan in place.

Data Insight:

A CFPB study showed that borrowers using payday loans for recurring expenses were three times more likely to default than those using them for one-time emergencies.

Example:

Anita in Tampa took a $300 payday loan to replace a broken refrigerator — a genuine necessity. She repaid it in two weeks without issues. In contrast, her cousin used a payday loan for a concert trip and struggled for months to pay it back.

Borrow Responsibly with Bad Credit

Having bad credit doesn’t mean you can’t manage debt wisely — it just means you have to be extra cautious.

Responsible Borrowing Tips:

- Borrow Only What You Need: If your bill is $400, don’t take $600 just because you can.

- Have a Repayment Plan: Mark your payday on the calendar and budget for it.

- Avoid Multiple Loans: Stacking payday loans increases the risk of default.

- Communicate with Your Lender: If you foresee repayment issues, ask about extensions or repayment plans.

Data Insight:

The Pew Charitable Trusts found that 81% of payday loan borrowers would have preferred an installment plan to repay the loan in smaller, affordable payments.

Example:

Paul in Oklahoma kept his payday loan cycle under control by never borrowing more than his upcoming paycheck’s extra margin after bills.

The Role of State Laws in “Guaranteed Approval” Loans

Where you live dramatically impacts your payday loan terms. Some states cap fees, while others allow almost unlimited charges.

Examples of State Regulations:

- Texas: No cap on APR, but lenders must disclose full cost.

- California: Loans up to $300 have a maximum fee of $45.

- New York: Payday loans are effectively banned.

Data Insight:

According to the National Conference of State Legislatures (NCSL), 12 states have outright bans on payday lending, while 32 states permit them with various restrictions.

Example:

Angela moved from Nevada (where she could get $500 payday loans) to New York, where payday loans are prohibited. She had to explore alternative financial options.

Understanding the Debt Cycle and How to Break Free

One of the biggest dangers with payday loans is the debt cycle — repeatedly borrowing to pay off previous loans.

Why the Cycle Happens:

- Short repayment terms drain your paycheck.

- High fees make it hard to repay in full.

- Lack of savings forces reborrowing.

How to Break the Cycle:

- Stop Rollovers: Pay off your current loan and don’t renew it.

- Seek Credit Counseling: Nonprofit agencies can negotiate with lenders.

- Build an Emergency Fund: Even $20 per paycheck adds up.

- Switch to Lower-Cost Credit: Use installment loans or PALs instead.

Data Insight:

The CFPB reports that 80% of payday loans are reborrowed within two weeks, and 50% are part of a sequence at least 10 loans long.

Example:

Rosa in Miami broke her payday loan cycle by consolidating three small loans into a single installment loan with a credit union, lowering her APR from 391% to 18%.

How Lenders Market “Guaranteed Approval” to Bad Credit Borrowers

Lenders often use the phrase “guaranteed approval” as a marketing hook — but in reality, no legitimate lender can promise approval without any conditions. What they mean is that they have flexible criteria and don’t heavily rely on credit scores.

Marketing Tactics to Watch For:

- Highlighting “No Credit Check” to attract borrowers with poor scores.

- Promoting “instant approval” to imply speed over scrutiny.

- Using testimonials that focus on getting cash the same day.

Data Insight:

A 2023 FTC report found that over 65% of “guaranteed loan” ads online were from unlicensed or offshore lenders, many of which violated U.S. lending laws.

Example:

Victor saw a “100% Guaranteed Loan” ad on social media and applied — only to find he was required to send a $75 “processing fee” upfront. It was a scam.

The Psychology Behind Choosing Payday Loans with Bad Credit

For borrowers facing urgent bills, the stress of the situation can cloud financial judgment. Payday loans appeal because they offer immediate relief, even if the long-term costs are high.

Why People Choose Them:

- Urgency Bias: Acting quickly to solve an immediate problem.

- Optimism Bias: Believing they’ll repay easily next payday.

- Avoidance: Not wanting to face embarrassment at a bank.

Data Insight:

The American Psychological Association found that 72% of adults feel stressed about money at least some of the time, and high stress correlates with quick, high-cost borrowing decisions.

Example:

Karen in Detroit chose a payday loan to cover her utility bill, convinced she’d repay it in two weeks — but unexpected medical expenses delayed her payment, triggering fees.

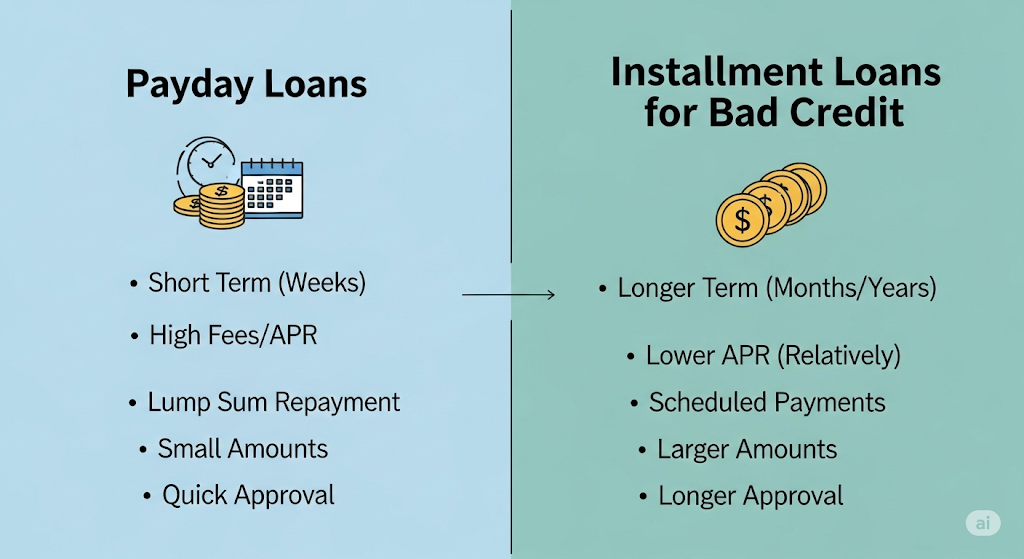

Comparing Payday Loans to Installment Loans for Bad Credit

Both payday and installment loans are available to bad credit borrowers, but their repayment structures are very different.

Payday Loans:

- Lump sum repayment in 14–30 days.

- Higher APRs (300–500%+).

- Best for one-time emergencies.

Installment Loans:

- Monthly payments over 3–24 months.

- APRs vary (18–99%).

- Better for larger amounts.

Data Insight:

Pew Research shows borrowers are 4x less likely to default on installment loans compared to payday loans because payments are spread out.

Example:

Luis in Phoenix switched from payday loans to a $1,000 installment loan with a 12-month term, lowering his monthly burden from $450 in one lump sum to $95 per month.

The Role of Technology in Guaranteed Payday Loan Approvals

Fintech innovations are reshaping payday lending, especially for bad credit borrowers.

Advances in Technology:

- AI Underwriting: Evaluates income stability rather than credit score.

- Bank Account Verification APIs: Approves loans instantly after checking deposits.

- Mobile Lending Apps: Enable 24/7 applications and funding.

Data Insight:

According to the Online Lenders Alliance, over 60% of payday loan applications in 2023 were completed entirely on mobile devices.

Example:

Maya in Los Angeles applied through a mobile lender app at midnight and had $300 in her bank account by 9 a.m. the next morning.

Conclusion: Borrowing Smart with Bad Credit

A payday loan with “guaranteed approval” might seem like the fastest fix when your credit score is low, but it’s rarely without conditions — and it comes with risks.

Key Takeaways:

- Verify lenders before applying.

- Borrow only what you can repay in full.

- Explore alternatives like PALs or installment loans.

- Use payday loans as a last resort, not a routine habit.

Smart borrowing today means protecting your financial future tomorrow.

Frequently Asked Questions (FAQs)

1. Are payday loans really guaranteed for bad credit?

No legitimate lender can guarantee approval. “Guaranteed” usually means relaxed criteria.

2. Do payday loans check credit scores?

Many do soft checks or skip traditional credit scoring, focusing on income instead.

3. What’s the average APR for payday loans?

Typically between 300–500% APR.

4. How fast can I get the money?

Often within the same business day or even hours for online loans.

5. Can I get a payday loan without a bank account?

Most lenders require a checking account for deposits and repayments.

6. What happens if I can’t repay on time?

You’ll face rollover fees, additional interest, and potential collection actions.

7. Are online payday loans safe?

Only if the lender is licensed in your state and uses secure encryption.

8. What’s the difference between payday and installment loans?

Payday loans are due in a lump sum, while installment loans have monthly payments.

9. Can payday loans help my credit score?

Usually no, as most lenders don’t report on-time payments to credit bureaus.

10. Are there alternatives for bad credit borrowers?

Yes — PALs, installment loans, credit builder loans, and borrowing from friends/family.