How to Take Money Out

Your 401(k) retirement plan is a powerful tool for building long-term financial security. But what happens if you need to access that money before retirement—or you’re ready to withdraw during retirement? Whether you’re facing an emergency, changing jobs, or hitting retirement age, understanding how to take money out of your 401(k) is essential.

This comprehensive 3,000-word guide explains everything you need to know about withdrawing from your 401(k)—rules, taxes, penalties, exceptions, and strategies for minimizing losses.

Chapter 1: Understanding the 401(k) Basics

1.1 What Is a 401(k)?

A 401(k) is a tax-advantaged retirement savings account offered by many employers. Employees contribute pre-tax income, and some employers offer matching contributions.

1.2 Types of 401(k)s

- Traditional 401(k): Pre-tax contributions, taxed upon withdrawal

- Roth 401(k): After-tax contributions, withdrawals are tax-free

Chapter 2: When Can You Withdraw Money?

2.1 Age 59½ Rule

You can withdraw without penalty once you reach age 59½, but taxes still apply for traditional 401(k)s.

2.2 Required Minimum Distributions (RMDs)

At age 73, you must start taking RMDs from a traditional 401(k)—Roth 401(k)s don’t require RMDs during your lifetime (as of 2024).

2.3 Early Withdrawals (Before 59½)

Withdrawals before 59½ are generally subject to a 10% penalty, plus regular income tax—unless you qualify for an exception.

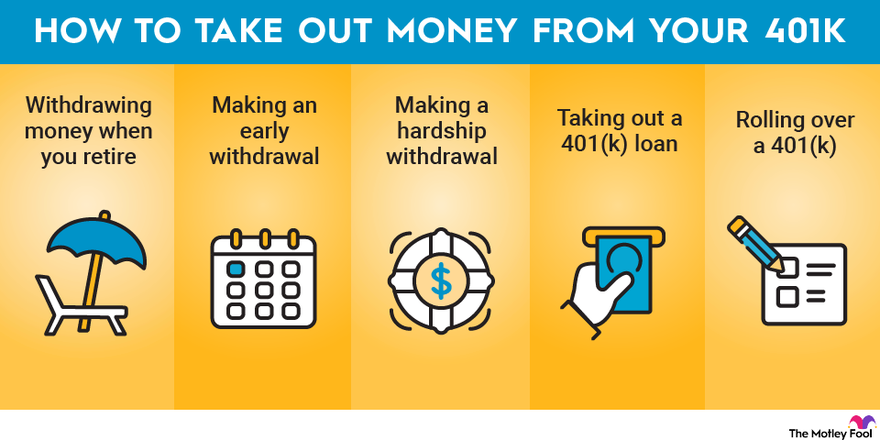

Chapter 3: How to Withdraw Money From a 401(k)

3.1 Lump-Sum Distribution

Take all the money out at once. Pros: Fast access. Cons: Large tax bill, potential for a higher tax bracket.

3.2 Partial Withdrawals

Take only what you need. This minimizes taxes and allows your remaining balance to continue growing.

3.3 Periodic Distributions

Set up regular monthly, quarterly, or annual withdrawals. Great for retirement income planning.

3.4 401(k) Loans vs. Withdrawals

- Loan: Borrow from your balance and repay it with interest

- Withdrawal: Permanent removal of funds

Chapter 4: Tax Implications

4.1 Traditional 401(k)

Withdrawals are taxed as ordinary income. Taking out a large amount could bump you into a higher tax bracket.

4.2 Roth 401(k)

- Qualified withdrawals (age 59½ and account held for 5+ years) are tax-free

- Non-qualified withdrawals may incur taxes on earnings

4.3 State Taxes

Some states don’t tax retirement withdrawals (e.g., Florida, Texas), while others do.

Chapter 5: Penalties for Early Withdrawal

5.1 Standard 10% Early Withdrawal Penalty

Withdraw before age 59½ and pay a 10% penalty + income tax.

5.2 Exceptions to the Penalty

You may avoid the penalty (but not taxes) in cases of:

- Permanent disability

- Medical expenses exceeding 7.5% of AGI

- Birth or adoption (up to $5,000)

- Separation from service after age 55 (age 50 for public safety employees)

- IRS levy

Chapter 6: Taking a 401(k) Loan Instead

6.1 How Loans Work

You borrow from your account (up to $50,000 or 50% of balance) and repay with interest over 5 years.

6.2 Pros of a 401(k) Loan

- No taxes or penalties

- Low interest rates (paid to yourself)

6.3 Cons

- Miss out on market gains

- Repayment is mandatory—default triggers taxes and penalties

Chapter 7: What Happens When You Change Jobs?

7.1 Leave the 401(k) With Your Old Employer

- Still grows tax-deferred

- Limited access and control

7.2 Roll Over to an IRA

- Keeps tax advantages

- More investment options

- Avoids immediate taxation

7.3 Roll Over to New Employer’s 401(k)

- Consolidate accounts

- Maintain employer protections

7.4 Cash Out (Not Recommended)

- Subject to taxes and penalties

- Reduces retirement savings significantly

Chapter 8: Strategic Withdrawal Planning

8.1 Withdraw Only What You Need

Helps minimize taxes and keeps your money growing.

8.2 Consider Tax Brackets

Plan withdrawals during low-income years to save on taxes.

8.3 Combine with Roth Conversions

Convert portions of your traditional 401(k) to a Roth IRA in lower-income years.

Chapter 9: Special Circumstances

9.1 COVID-19 Related Withdrawals (CARES Act)

In 2020, penalty-free withdrawals up to $100,000 were allowed with repayment options—no longer in effect, but important historically.

9.2 Divorce and QDROs

- A Qualified Domestic Relations Order allows splitting a 401(k) in divorce

- Recipient spouse may roll over or cash out their share

9.3 Inheritance of a 401(k)

- Rules differ for spouses vs. non-spouses

- Non-spouses often must withdraw funds within 10 years

Chapter 10: Tips to Protect Your Retirement Funds

10.1 Avoid Early Withdrawals

Exhaust other options (emergency savings, personal loans) first

10.2 Keep Beneficiaries Updated

Prevents legal confusion or delays

10.3 Use a Financial Advisor

Tax rules and strategies can be complex; professional help can maximize outcomes

Conclusion

Taking money out of a 401(k) isn’t as simple as withdrawing from a checking account. It’s governed by strict tax rules, penalties, and long-term implications. In general, early withdrawals should be avoided unless absolutely necessary.

If you’re nearing retirement, consider tax-efficient withdrawal strategies. If you’re in an emergency, explore 401(k) loans or penalty exceptions before cashing out. And if you’re changing jobs, rolling your 401(k) into an IRA is often the smartest move.

Your 401(k) is your future—protect it wisely.

Keywords for SEO: how to take money out of 401k, 401k early withdrawal rules, 401k taxes and penalties, 401k loan vs withdrawal, rollover 401k to IRA, 401k withdrawal after 59.5