Introduction — Why This Question Matters for Every Borrower

Is a Payday Loan Installment or Revolving are one of the most controversial forms of short-term lending in the United States. Many people see them as a quick financial lifeline during emergencies — but very few truly understand how they work in comparison to other loan types like installment loans or revolving credit.

This lack of understanding often leads to unexpected costs, repayment struggles, and long-term debt cycles. In fact, according to the Consumer Financial Protection Bureau (CFPB), over 80% of payday loans are rolled over or renewed within two weeks, meaning borrowers often end up paying far more than they borrowed.

Why this matters:

- Choosing the wrong loan type can cost hundreds in extra fees.

- The repayment structure directly impacts your ability to manage debt.

- Certain loan types help build credit — payday loans generally do not.

Sarah, a Sacramento resident, borrowed $300 through a payday loan thinking it would work like her old personal loan. Instead of monthly payments, the lender demanded $345 two weeks later. She couldn’t pay, so she rolled it over twice, eventually paying $135 in fees — without reducing the original $300 debt

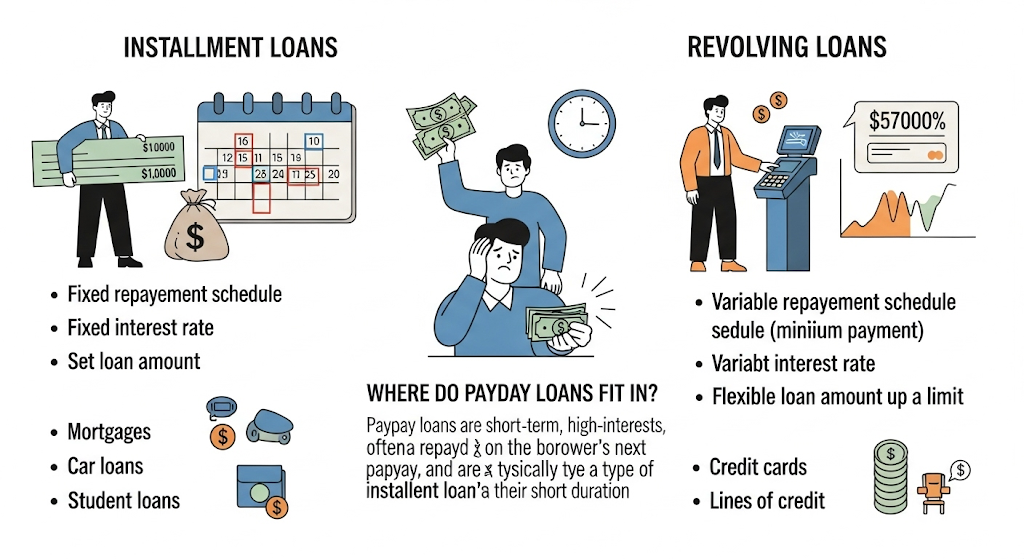

What Is an Installment Loan?

Definition and Core Features

An installment loan is a fixed-term borrowing arrangement where you receive a lump sum upfront and repay it in equal, scheduled payments over months or years.

Key features include:

- Fixed repayment schedule — same due date each month

- Predictable monthly amount — helps with budgeting

- Combination of principal and interest in every payment

Common examples:

- Auto loans

- Mortgages

- Personal loans

- Student loans

Why Installment Loans Are Popular

Installment loans are preferred for large purchases or debt consolidation because they allow you to spread payments over time while locking in an interest rate.

Advantages:

- Lower interest rates than payday loans (typically 6–36% APR)

- Potential to improve credit score (if reported to credit bureaus)

- Flexible loan amounts ranging from a few hundred to tens of thousands

Disadvantages:

- Requires better credit or collateral for approval

- Not ideal for extremely small, urgent borrowing needs

Real-Life Installment Loan Example

If you borrow $5,000 at a 10% APR for 24 months:

- Monthly payment: $230.72

- Total interest paid: $537.28

- Total amount repaid: $5,537.28

Compared to payday loans, this is far more affordable for the same principal amount, even if it takes longer to repay.

What Is Revolving Credit?

Definition and Structure

Revolving credit is a type of borrowing where you have a set credit limit and can borrow, repay, and borrow again — as long as you stay within that limit.

Examples:

- Credit cards

- Home Equity Lines of Credit (HELOCs)

- Store charge cards

How Revolving Credit Works

Let’s say you have a $2,000 credit card limit:

- Spend $500 → Remaining limit is $1,500

- Repay $300 → New available credit is $1,800

This ongoing access to funds makes revolving credit ideal for ongoing or unpredictable expenses.

Pros:

- Flexible borrowing

- Only pay interest on the amount used

- Can build credit history

Cons:

- Can lead to overspending

- High interest rates if balances aren’t paid in full (average U.S. credit card APR is around 20–25%)

Revolving Credit in Action

Mark uses a credit card for emergencies instead of payday loans. When his car needed a $600 repair, he paid with the card. He repaid $200 each month, paying $18 in interest over three months — far cheaper than the $105 in fees he would have paid with a payday loan for the same amount.

Where Payday Loans Fit in the Picture

Payday Loans — A Unique Category

Payday loans are neither installment loans nor revolving credit. They are short-term, lump-sum repayment loans intended to be repaid by your next paycheck.

Typical payday loan terms:

- Loan size: $100–$1,000 (varies by state)

- Repayment term: 14–31 days

- Average APR: 300–500% (sometimes higher)

- Repayment method: Post-dated check or automatic bank withdrawal

The High Cost of Payday Loans

Because the repayment period is so short, payday lenders charge a flat fee per $100 borrowed (usually $15–$20). While this might seem small, it translates into triple-digit APRs.

Example:

Borrow $500 → $75 fee → 14-day term

APR calculation: (($75 ÷ $500) × (365 ÷ 14)) × 100 ≈ 391% APR

Why People Confuse Payday Loans With Installment Loans

Some lenders now market “installment payday loans” that allow repayment over 2–6 months. While these mimic installment loan structures, they still have:

- Much higher APRs than traditional installment loans

- Shorter terms

- Stricter repayment schedules

Data Snapshot — U.S. Payday Loan Usage

According to the Pew Charitable Trusts and the Consumer Financial Protection Bureau:

- 12 million Americans use payday loans annually

- The average borrower takes out 8 payday loans per year

- The average loan amount is $375, but the average fees paid per borrower annually are $520

- Over 80% of payday loans are rolled over or followed by another loan within 14 days

Comparing Payday Loans, Installment Loans, and Revolving Credit

Understanding the differences between these loan types is critical because it shapes repayment strategy, cost, and long-term financial health. Payday loans, installment loans, and revolving credit each serve different borrower needs, but their structures can lead to vastly different outcomes.

Payday loans require a single lump-sum repayment within a short period — typically two to four weeks. This rigid repayment model means that if you miss the due date, you incur additional fees or may roll the loan over, leading to a costly debt spiral.

Installment loans allow repayment over months or years, with predictable monthly payments that combine principal and interest. They are far better for budgeting and usually carry lower interest rates.

Revolving credit offers the flexibility to borrow, repay, and reborrow up to a set credit limit, making it ideal for ongoing expenses. However, it requires discipline to avoid high-interest balances.

Quick Comparison Table

| Feature | Payday Loan | Installment Loan | Revolving Credit |

|---|---|---|---|

| Repayment Structure | Lump sum | Equal installments | Flexible payments |

| Term Length | 14–31 days | Months–years | Ongoing |

| Average APR | 300–500% | 6–36% | 12–25% |

| Credit Check Required | Minimal or none | Usually required | Required |

| Reuse of Funds | No | No | Yes |

Pros and Cons of Each Loan Type for Borrowers

Every loan type has its place — but the suitability depends on the borrower’s financial habits, urgency, and repayment ability.

Payday Loans — Best for:

- Extreme emergencies when other credit options are unavailable

- Borrowers with very poor credit history

Pros:

- Fast approval and funding (same-day possible)

- Minimal paperwork

- Accessible to most borrowers

Cons:

- Extremely high APR and fees

- Single lump-sum repayment creates repayment pressure

- High rollover rates lead to long-term debt cycles

Installment Loans — Best for:

- Larger expenses that need structured repayment

- Borrowers seeking predictable budgeting

Pros:

- Lower interest rates compared to payday loans

- Improves credit score with timely payments

- Longer repayment periods reduce financial strain

Cons:

- Stricter eligibility criteria

- May take longer for approval and funding

Revolving Credit — Best for

- Ongoing or variable expenses

- Borrowers who can manage balances responsibly

Pros:

- Flexible use of funds

- Ability to reuse available credit without reapplying

- Often comes with rewards or benefits

Cons:

- Encourages overspending if not disciplined

- Interest accumulates quickly on carried balances

Why Payday Loans Are Riskier Than Other Types

The main reason payday loans carry more risk is their short repayment window combined with triple-digit APRs. Unlike installment loans, there’s no gradual repayment — the entire amount plus fees is due at once.

Example:

Borrow $400 at a $15 fee per $100 borrowed. In 14 days, you owe $460. If you can’t pay, rolling it over adds another $60 in fees, raising the cost to $520 within a month. That’s an effective APR of over 400%.

Data Insight:

The CFPB reports that 70% of payday loan borrowers take out a second loan within a month because they couldn’t repay the first one in full. This creates a cycle of dependency, often leading to multiple loans being active at the same time.

Are There Safer Alternatives to Payday Loans?

Before committing to a payday loan, consider these less risky alternatives:

- Credit Union Payday Alternative Loans (PALs): Capped at 28% APR, repayable over 1–6 months.

- Personal Loans from Online Lenders: Some approve small amounts for borrowers with fair credit at much lower rates.

- Earned Wage Access Apps: Get a portion of your paycheck early for a small flat fee.

- Negotiating with Creditors: Some utility companies and medical providers offer short-term payment plans without interest.

Maria, a Baton Rouge resident, needed $500 for emergency dental work. Instead of a payday loan, she used her credit union’s PAL program. She repaid the loan over three months at 24% APR, paying only $18 in interest — saving over $100 compared to a payday lender.

How the Loan Type Affects Your Credit Score

Payday loans generally do not report positive payment history to credit bureaus. However, if you default, the debt may be sent to collections, which will appear on your credit report and significantly lower your score.

Installment loans and revolving credit accounts can help build credit if payments are made on time. Maintaining a low credit utilization ratio on revolving accounts is one of the fastest ways to improve your score.

Regulatory Landscape for Payday Loans in the U.S.

Payday loan regulations vary widely by state. Some states, like New York, effectively ban them by capping APRs at 25%. Others, like Texas and Mississippi, allow high-cost payday lending with few restrictions.

In California, payday loans are capped at $300, with a maximum fee of $45 — yet this still results in APRs over 400% due to the short repayment term. Federal protections like the Military Lending Act cap APRs at 36% for active-duty service members.

Key Takeaways for Borrowers

- Payday loans are neither installment loans nor revolving credit — they’re a separate, high-cost category.

- Their lump-sum repayment and high APRs make them risky for long-term financial health.

- Safer alternatives exist, including PALs, personal loans, and earned wage access services.

- Always understand the loan’s structure, costs, and repayment terms before signing.

Conclusion — Borrow Smarter, Not Harder

Knowing whether a loan is installment or revolving isn’t just trivia — it’s the foundation of borrowing wisely. Payday loans may offer fast cash, but their structure makes them more expensive and riskier than most alternatives.

If you need predictability, go for an installment loan. If you want flexibility, revolving credit might be the better choice. And if you’re considering a payday loan, weigh all your other options first — your future self will thank you.

FAQs — Is a Payday Loan Installment or Revolving?

1. Is a payday loan considered an installment loan?

No. Payday loans are short-term, lump-sum repayment loans due by your next paycheck. Unlike installment loans, they don’t allow gradual repayment over months. You must repay the full principal plus fees in one payment, making them riskier for borrowers with tight budgets.

2. Is a payday loan revolving credit?

No. Revolving credit lets you borrow, repay, and reborrow up to a set limit. Payday loans are a one-time cash advance that must be repaid in full. You cannot reuse funds without taking out a new loan and paying additional fees.

3. What’s the main difference between payday loans and installment loans?

Installment loans offer fixed monthly payments over months or years, often at lower APRs. Payday loans require full repayment within 14–31 days and have much higher APRs, often over 300%. This makes installment loans better for budgeting and affordability.

4. Can a payday loan improve my credit score?

Generally, no. Payday lenders typically don’t report on-time payments to credit bureaus. However, missed payments or defaults may be sent to collections, which can harm your credit score for up to seven years.

5. Are there payday loans with installment payments?

Some lenders offer “installment payday loans,” but they still have high APRs and shorter terms than regular installment loans. While payments are spread out, costs remain much higher compared to traditional personal loans from banks or credit unions.

6. Why are payday loans more expensive than other loan types?

Payday loans charge a flat fee per $100 borrowed, which translates into triple-digit APRs because of the short repayment term. High default risks and lack of collateral also contribute to higher costs compared to installment or revolving loans.

7. Which loan type is better for emergencies?

If you qualify, a small personal installment loan or a credit union Payday Alternative Loan (PAL) is safer and cheaper than a payday loan. Revolving credit, like a credit card, can also be a good option if you can repay quickly.

8. Do payday loans have interest rates or just fees?

Payday loans typically list costs as a flat fee, but when calculated as an annual percentage rate (APR), it often exceeds 300–500%. This is much higher than rates for installment loans or revolving credit.

9. Can payday loans be refinanced into installment loans?

Yes, some borrowers refinance payday loans into longer-term installment loans to reduce payment pressure. However, this may involve new fees or higher total interest over time, so it’s important to compare costs before refinancing.

10. Are payday loans legal in all U.S. states?

No. Some states ban payday loans entirely, while others cap fees or set maximum loan amounts. Regulations vary, so it’s important to check your state’s laws before borrowing. For example, New York prohibits payday lending, but Texas and Mississippi allow it.