Introduction

Payday loans Chattanooga, TN, are a quick solution for residents who face urgent cash needs between paychecks. These short-term, high-interest loans are popular because they’re fast and require minimal qualifications. However, they also come with steep costs that can trap borrowers in debt if used carelessly.

In this comprehensive guide, we’ll break down how payday loans work in Chattanooga, local regulations, fees, benefits, risks, and smarter alternatives. We’ll also share real-life examples so you can make a fully informed decision.

Understanding Payday Loans in Chattanooga

A payday loan is a small-dollar, short-term loan—typically $100 to $500—intended to cover expenses until your next paycheck. In Tennessee, these loans are legal but heavily regulated.

Key Features:

- Loan amounts usually range from $100 to $425

- Must be repaid within 31 days or less

- High annual percentage rates (APRs), often 300%–460%

- Requires proof of income and a valid ID

Example:

Mike, a Chattanooga warehouse worker, took a $300 payday loan to repair his car. Although he repaid it in two weeks, the $45 fee translated to an APR of over 390%.

Tennessee Payday Loan Laws You Should Know

Tennessee has specific laws for payday loans—officially called “deferred presentment” transactions.

State Rules:

- Maximum loan: $425

- Term: Up to 31 days

- Finance fee: Up to $17.65 per $100 borrowed

- Rollovers: Not allowed—you cannot take a new payday loan to cover the old one

- Must have a written contract outlining terms

Why This Matters:

Without rollovers, borrowers are encouraged to pay off their debt in full rather than extend it indefinitely—a common trap in other states.

The True Cost of Payday Loans in Chattanooga

While payday loans provide instant cash, the cost is far higher than most borrowers expect.

Breakdown Example for a $300 Loan:

- Finance charge: $52.95

- Repayment in 14 days = $352.95 total

- Equivalent APR: Around 460%

Data Insight:

According to the Center for Responsible Lending, Tennessee payday borrowers spend over $400 million annually in fees, much of which could be saved through lower-cost alternatives.

When to Consider a Payday Loan

A payday loan should only be used in urgent, unavoidable situations when no cheaper option is available.

Possible Justifiable Uses:

- Medical emergency not covered by insurance

- Preventing eviction or utility shutoff

- Urgent car repairs to maintain employment

Example:

Sarah, a single mom in Chattanooga, used a payday loan to pay an overdue electric bill during winter. It prevented a shutoff, but she repaid the loan with her tax refund to avoid extra fees.

Risks of Payday Loans in Chattanooga

Despite their convenience, payday loans carry significant risks.

Major Risks:

- Debt Cycle: High fees make repayment difficult, leading to repeated borrowing.

- Budget Strain: Repaying in full on your next payday can leave you short again.

- No Credit Boost: Most lenders don’t report positive payments to credit bureaus.

- Legal Action: Nonpayment can lead to collections and potential court cases.

Impact:

Many Chattanooga residents report that after taking one payday loan, they ended up taking three or more within a year just to cover the cost of the first.

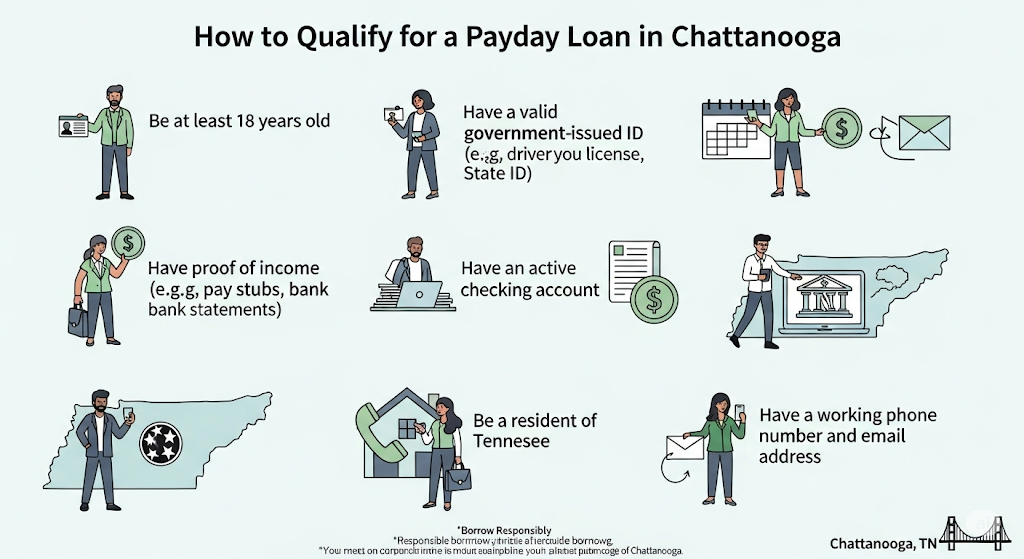

How to Qualify for a Payday Loan in Chattanooga

While payday lenders in Tennessee do not require perfect credit, they still have basic eligibility criteria.

Typical Requirements:

- Proof of steady income (pay stubs, bank statements, or government benefits)

- Valid government-issued photo ID

- Active checking account

- Be at least 18 years old

- Tennessee residency proof

Example:

David, a Chattanooga truck driver, qualified for a $250 payday loan by showing his pay stub and driver’s license. Even though he had a low credit score, the lender approved his application within 30 minutes.

Application Process – Step-by-Step

Applying for a payday loan in Chattanooga can be done in-store or online, with online applications becoming more popular for speed and convenience.

Step-by-Step Process:

- Fill Out an Application – Provide your personal, banking, and employment details.

- Submit Documentation – Upload or present proof of ID and income.

- Loan Review – Lenders verify your information and assess risk.

- Approval & Agreement – If approved, you sign a loan agreement outlining repayment terms.

- Funding – Receive cash instantly in-store or via direct deposit within hours.

Pro Tip:

Avoid lenders who ask for excessive personal data beyond what is required, as this may be a scam.

Costs and Fees – The Hidden Price of Fast Cash

The most important factor to understand is how much a payday loan truly costs.

Breakdown for a $400 Loan in Chattanooga:

- Finance Fee: $70.60

- Total Repayment in 14 Days: $470.60

- APR: Over 450%

Data Insight:

According to the Tennessee Department of Financial Institutions, the average payday borrower in the state takes out 7 loans per year, paying hundreds in cumulative fees.

Example:

Linda took a $400 payday loan to cover medical bills. She couldn’t repay it on her next payday, so she borrowed again—paying $141 in fees over two months.

Alternatives to Payday Loans in Chattanooga

Before turning to payday loans, it’s worth exploring lower-cost options that can provide similar relief without the high interest.

Possible Alternatives:

- Credit Union Payday Alternative Loans (PALs) – Lower fees and longer repayment terms.

- Employer Cash Advance – Some Chattanooga companies offer paycheck advances without interest.

- Installment Loans – Spread repayment over months, not weeks.

- Local Assistance Programs – Nonprofits like the United Way offer emergency financial help.

Example:

Maria avoided a payday loan by getting a $200 PAL from her credit union, repaid over three months at a fraction of the cost.

Common Mistakes Chattanooga Borrowers Make

Payday loans can cause more harm than good if not used wisely.

Mistakes to Avoid:

- Borrowing Without a Repayment Plan – Leads to multiple loans in a cycle.

- Ignoring the APR – Many focus only on the fee amount, not the annualized cost.

- Using Loans for Non-Essentials – Borrowing for shopping or entertainment adds unnecessary debt.

- Not Reading the Contract – Some borrowers miss important clauses about fees and collections.

Example:

Tom borrowed for a vacation, thinking he’d repay quickly. He ended up juggling two payday loans for months, paying more in fees than the original loan amount.

Legal Protections for Payday Loan Borrowers in Tennessee

Tennessee has specific regulations designed to protect payday loan customers from excessive debt traps.

Key Legal Rules:

- Loan Amount Limit: Up to $500 per loan.

- Maximum Term: 31 days.

- Rollovers: Only two renewals allowed.

- Fee Cap: $15.50 per $100 borrowed.

- Cooling-Off Period: After 3 consecutive loans, borrowers must wait until the first loan is fully paid before taking another.

Example:

Sarah in Chattanooga had already renewed her loan twice. Thanks to state rollover limits, the lender couldn’t extend her debt cycle further — forcing her to settle the balance and avoid paying hundreds more in fees.

Payday Loan Scams in Chattanooga – How to Stay Safe

Scams are a growing risk, especially with online payday loan offers targeting financially stressed residents.

Red Flags:

- Requests for upfront “processing” fees

- Lenders with no physical address in Tennessee

- Unverified licenses or no registration with the state

- Demands for payment via gift cards or wire transfers

Example:

Marcus applied for an “instant approval” loan online. After paying a $50 fee, the website vanished — leaving him without the loan or his money.

Pro Tip:

Verify any lender through the Tennessee Department of Financial Institutions before applying.

The Impact of Payday Loans on Chattanooga’s Economy

While payday loans can help individuals in emergencies, they drain money from the local economy.

Data Insight:

According to consumer advocacy reports:

- Tennessee payday loan borrowers pay over $100 million annually in fees.

- In Chattanooga’s lower-income neighborhoods, payday storefronts are often more common than grocery stores.

Economic Effects:

- Less disposable income for local shopping

- Higher reliance on public aid due to debt strain

- Reduced financial stability in affected communities

Example:

A local Chattanooga small business saw a 15% sales drop in an area where payday loan usage was high — as customers spent more on fees than goods.

Seasonal Demand for Payday Loans in Chattanooga

Demand for payday loans spikes during certain times of the year due to seasonal expenses.

Peak Periods:

- December–January: Holiday spending + heating bills

- August: Back-to-school costs

- April: Tax bills and IRS payments

Data Insight:

Local lenders report a 30% increase in payday loan applications in December alone.

Example:

In December, Jessica borrowed $300 for Christmas gifts but had to roll it over twice in January due to high winter utility costs — ending up repaying $480.

The Role of Fintech in Chattanooga’s Payday Loan Market

Fintech is transforming payday lending by making the process faster, more transparent, and more accessible.

Advantages of Fintech Payday Lenders:

- Mobile apps with same-day approval

- Direct deposit within hours

- AI-based risk assessment for tailored loan terms

- Real-time repayment tracking

Example:

Alex used a payday loan app during his lunch break. He applied, got approved, and had funds in his account in under 45 minutes — without visiting a store.

The Future of Payday Loan Regulation in Chattanooga

Tennessee lawmakers continue to debate whether stricter rules should be applied to payday loans, similar to other states.

Possible Future Changes:

- Lower APR caps to reduce borrower costs

- Longer repayment terms with installment options

- Limits on total annual borrowing per individual

- Mandatory financial counseling before approval

Potential Impact:

If stricter laws pass, consumers may benefit from safer lending, but some high-cost lenders could exit the market — potentially reducing immediate access to quick cash.

Example:

When Arkansas capped payday loan APRs at 17%, most payday lenders left the state — but credit unions stepped in with small-dollar alternatives.

Payday Loans and Your Credit Score

Many borrowers assume payday loans can help build credit — but in most cases, they don’t.

Key Facts:

- Most payday lenders don’t report on-time payments to credit bureaus.

- Missed payments that go to collections do appear and hurt your score.

- Payday loan debt can indirectly harm credit by increasing overall debt load.

Pro Tip:

If your goal is credit improvement, consider a secured credit card or credit-builder loan instead.

Life Example:

James paid off three payday loans on time, but his credit score didn’t change. However, one late payment sent to collections dropped his score by 70 points.

How to Compare Payday Loan Offers in Chattanooga

Comparing payday loan offers can save significant money in fees and interest.

Comparison Checklist:

- Total repayment amount (not just the fee)

- APR and finance charges

- Early repayment penalties

- Rollover policies and limits

Example:

Maria compared two $300 loan offers — one had a $45 fee, the other $60. Choosing the cheaper lender saved her $15, enough to cover part of her utility bill.

Community-Based Alternatives in Chattanooga

Several nonprofits and credit unions in Chattanooga offer low- or no-interest emergency loans to reduce reliance on payday lenders.

Examples:

- Chattanooga Neighborhood Enterprise – Small-dollar loan programs

- TVA Community Credit Union – Payday Alternative Loans (PALs)

- Local churches & charities – Emergency bill assistance

Example:

Deborah avoided a payday loan by getting a $250 PAL from her credit union with just a $6 fee — saving over $60 compared to a payday lender.

Conclusion – Borrowing Smarter in Chattanooga

Payday loans in Chattanooga can serve as emergency financial tools, but they’re best used as a last resort.

Key Takeaways:

- Always compare offers and check lender licenses.

- Explore alternatives like PALs, credit unions, or local aid programs.

- Treat payday loans as short-term fixes, not long-term solutions.

- Know your rights under Tennessee law to avoid predatory practices.

Final Thought:

The smartest financial move is to prepare for emergencies before they happen — but if you must borrow, do it with full awareness of costs, risks, and safer options.

Frequently Asked Questions – Payday Loans in Chattanooga

1. Are payday loans legal in Chattanooga?

Yes. Payday loans are legal in Tennessee, including Chattanooga. Lenders must be licensed by the Tennessee Department of Financial Institutions and follow state laws on fees, terms, and rollovers.

2. What is the maximum amount I can borrow?

In Tennessee, payday loan amounts are typically capped at $500 per loan. This limit is set by state law to reduce excessive borrowing.

3. How much will a payday loan cost me in Chattanooga?

Tennessee law allows lenders to charge up to 15% of the loan amount as a fee. For example, a $300 loan could have a $45 fee, which must be repaid within the loan term.

4. How long do I have to repay a payday loan in Chattanooga?

Most payday loans in Chattanooga must be repaid in no more than 31 days. However, some lenders may offer installment options if you qualify.

5. Can I renew or roll over my payday loan?

Tennessee limits loan rollovers to two times. However, interest and fees still apply on each renewal, so costs can add up quickly.

6. Will taking a payday loan affect my credit score?

Generally, payday lenders do not report on-time payments to credit bureaus. But if you default and the loan goes to collections, it can negatively impact your credit score.

7. Are there alternatives to payday loans in Chattanooga?

Yes. Local credit unions, community development financial institutions (CDFIs), and nonprofits often offer Payday Alternative Loans (PALs) or small-dollar loans at much lower rates.

8. How can I check if a lender is legitimate?

You can verify a lender’s license on the Tennessee Department of Financial Institutions website or call their office before applying.

9. Can military members take payday loans in Chattanooga?

Active-duty military personnel are protected by the Military Lending Act, which caps the APR at 36% and prohibits certain predatory practices.

10. What should I do if I’m struggling to repay my loan?

Contact your lender immediately to discuss repayment plans. You may also seek help from credit counseling agencies in Chattanooga, such as the Consumer Credit Counseling Service of the Southeast.