Introduction – The Role of Payday Loans in Fort Worth’s Financial Landscape

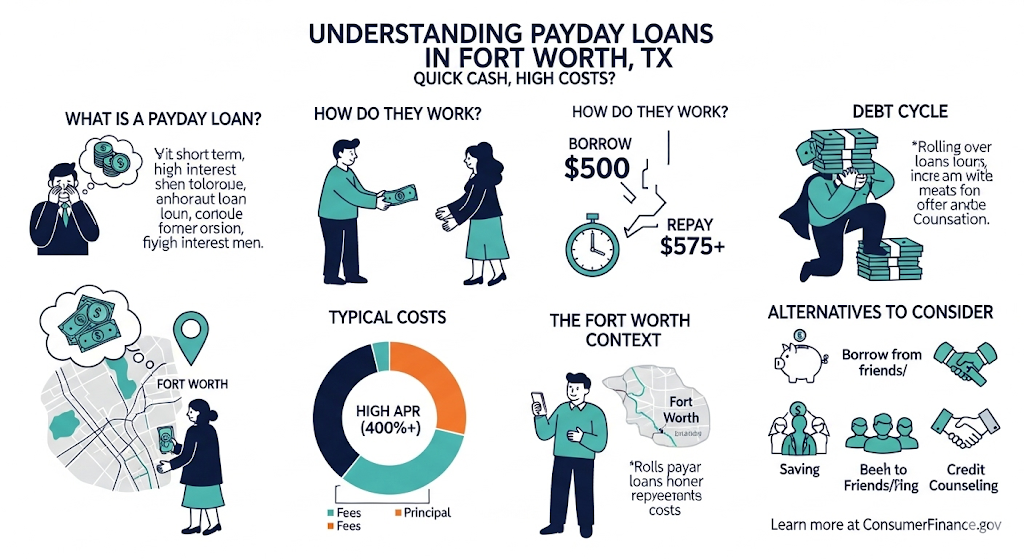

Payday Loans Fort Worth, Texas, is home to over 950,000 residents and a fast-growing economy, yet many households still face sudden financial challenges. Payday loans in Fort Worth offer fast, no-hassle cash to cover emergencies before the next paycheck. Unlike traditional loans, they often skip lengthy credit checks, focusing on income verification for same-day approval.

While these loans provide instant relief, they also come with high APRs (300–500%+), meaning borrowers should approach them as short-term solutions rather than ongoing financial support.

Key Takeaways:

- Quick access to cash without traditional banking delays

- Higher costs compared to credit unions or personal loans

- Works best for urgent, one-time needs

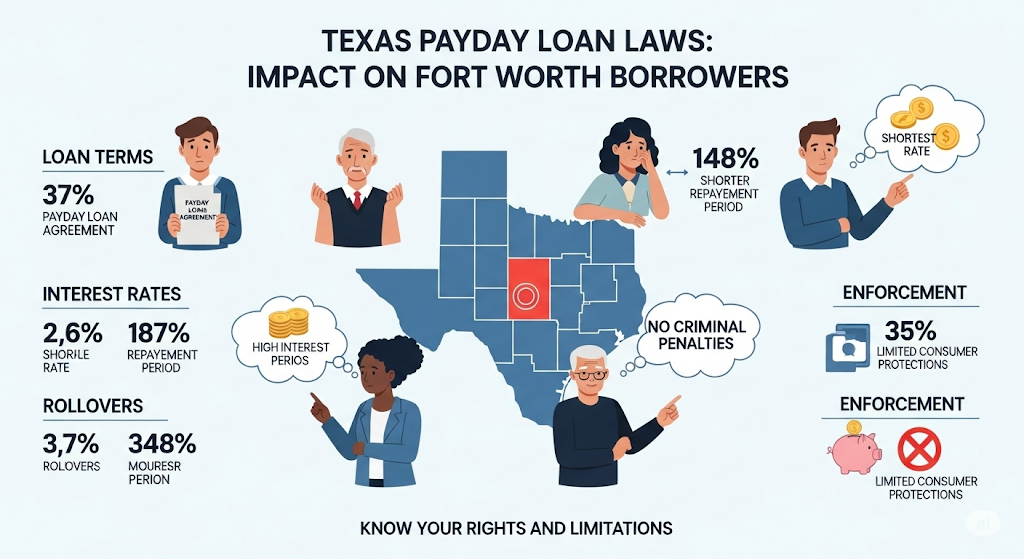

Texas Payday Loan Laws and Fort Worth Ordinances

Texas is known for having looser payday lending regulations compared to other states, but Fort Worth has set local ordinances to prevent predatory lending. These rules ensure borrowers are not trapped in endless debt cycles.

Key Fort Worth Regulations:

- Loan Amount Cap: Cannot exceed 20% of monthly gross income

- Maximum Rollovers: Only 3 allowed, with partial principal repayment each time

- Term Limits: 14–30 days, depending on lender

- No Statewide APR Cap: Rates can exceed 500% APR

Example:

Carlos, earning $2,500 monthly, could only borrow up to $500 from a Fort Worth lender due to the 20% income cap. This rule prevented him from taking out an amount he might struggle to repay.

Common Reasons Fort Worth Residents Use Payday Loans

Payday loans are often used as a financial lifeline during urgent situations. The speed and ease of approval make them appealing for short-term emergencies.

Top Borrowing Reasons:

- Emergency car repairs

- Avoiding utility shutoffs

- Medical or dental emergencies

- Rent or mortgage shortfalls

- Unexpected travel costs

Example:

James, a warehouse worker in Fort Worth, took out a $250 payday loan to repair his car’s transmission. Without it, he would have missed multiple shifts and risked losing his job.

How to Apply for a Payday Loan in Fort Worth

Applying for a payday loan in Fort Worth can be done in-store or online, often within 30 minutes.

Requirements:

- Valid government-issued photo ID

- Proof of steady income

- Proof of Fort Worth address

- Active checking account

Application Steps:

- Fill out a short application online or at a store.

- Provide verification documents.

- Review and sign the loan agreement.

- Receive funds — in cash or via direct deposit.

Example:

Maria, a college student in Fort Worth, applied online for $200 to cover rent after her roommate moved out. She received the deposit the same day, avoiding late fees.

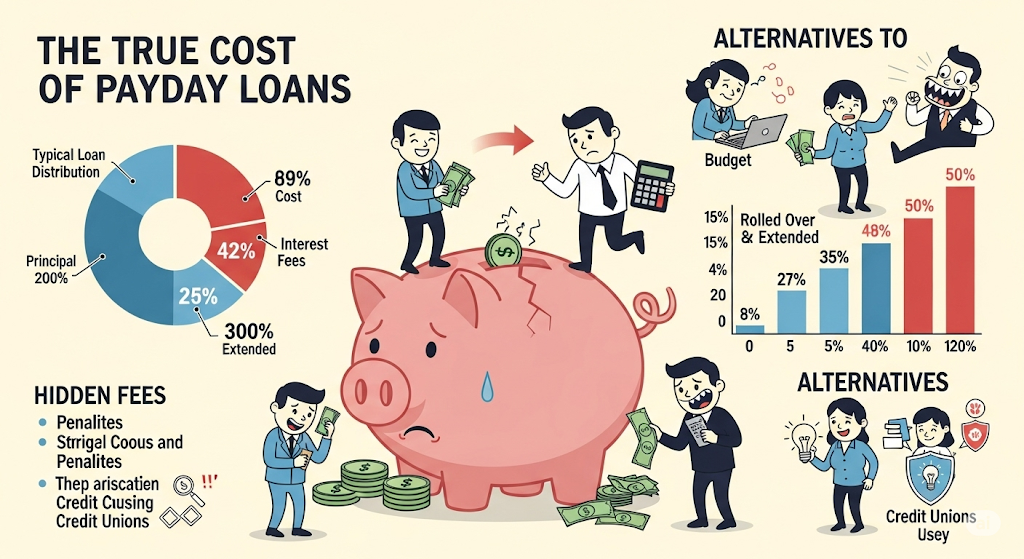

Understanding the True Cost of Payday Loans

While payday loans offer immediate access to cash, they come with significant costs.

Typical Costs in Fort Worth:

- Fees: $15–$30 per $100 borrowed

- APR: 300–500%+

- Average Loan: $350–$500

- Repayment Period: 14–30 days

Example Calculation:

Borrowing $400 with a $60 fee for 14 days equals 391% APR. Rolling over twice would add $120 in fees, totaling $580 for a $400 loan.

Example:

Linda borrowed $300 for emergency vet care. Due to rolling over twice, she paid $180 in fees before clearing the balance.

Online vs. In-Store Payday Loans in Fort Worth

In Fort Worth, borrowers can choose between traditional storefront payday lenders and modern online lenders. Both have pros and cons, and understanding them can help you make the right choice.

Storefront lenders provide face-to-face service and allow you to walk out with cash the same day. Online lenders, on the other hand, offer 24/7 applications, electronic signatures, and direct deposit without leaving your home.

Advantages of Online Loans:

- Apply anytime from anywhere

- No need to travel or wait in lines

- Faster processing for repeat customers

Advantages of In-Store Loans:

- Immediate cash in hand

- Personal assistance from staff

- Easier to ask questions before signing

Life Example:

Angela, a Fort Worth resident without internet access at home, preferred visiting a local payday store. She received $300 in cash within 20 minutes. Meanwhile, her friend Michael applied online during a lunch break and had $500 deposited by the next morning.

Risks and Pitfalls of Payday Loans in Fort Worth

While payday loans can be a lifeline, they also come with significant financial risks. High APRs and short repayment terms can cause borrowers to fall into a cycle of debt if they cannot repay on time.

Common Risks:

- Debt Trap: Rolling over loans repeatedly can multiply costs.

- Overdraft Fees: Automatic withdrawals can trigger bank charges.

- Impact on Budget: A large repayment from your next paycheck can leave you short again.

- Aggressive Collections: Some lenders may use high-pressure tactics if you miss a payment.

Example:

Paul borrowed $400 for an emergency medical bill but rolled it over twice, paying an extra $240 in fees. By the time he cleared the debt, he had spent $640 for a loan that was originally $400.

Alternatives to Payday Loans in Fort Worth

Not everyone knows that safe, affordable alternatives to payday loans exist in Fort Worth. Exploring these options can save you hundreds in fees.

Better Alternatives:

- Credit Union Payday Alternative Loans (PALs): Lower fees, flexible terms

- Emergency Assistance Programs: Local charities and churches offer grants or zero-interest loans

- Salary Advance from Employer: Some companies provide early wage access

- Installment Loans: Longer repayment terms, often lower APR

Example:

Jessica needed $250 for car repairs. Instead of a payday loan, she borrowed from her credit union’s PAL program, paying just a $12 fee and repaying over 60 days — avoiding the $75 fee a payday lender quoted her.

How to Compare Payday Loan Offers in Fort Worth

With dozens of lenders competing for your business, comparing offers is crucial. The cheapest-looking loan isn’t always the best once you factor in fees, terms, and rollover policies.

Key Comparison Points:

- Total Repayment Amount — Not just the fees, but the final cost.

- APR and Finance Charges — Lower is better, even on short-term loans.

- Early Repayment Penalties — Some lenders still charge if you pay early.

- Rollover Rules — Understand if, and how, you can extend repayment.

Example:

David compared two Fort Worth payday loans for $300. One cost $45 in fees, the other $75. By choosing the cheaper one, he saved $30 — enough to pay for a week’s groceries.

Responsible Payday Loan Borrowing Strategies

If you decide to take a payday loan in Fort Worth, following responsible borrowing practices can protect your finances and reduce stress.

Smart Borrowing Tips:

- Borrow only what you can repay in full on your next payday

- Avoid multiple loans at once

- Set aside money immediately for repayment

- Treat payday loans as a last resort rather than a habit

Example:

Samantha borrowed $200 for an urgent plumbing repair. She budgeted tightly, skipping non-essential purchases, and repaid on time — avoiding rollover fees and keeping her costs at $30.

Understanding Texas Payday Loan Laws and How They Affect Fort Worth Borrowers

Texas has some of the most lender-friendly payday loan laws in the country, and Fort Worth is no exception. Unlike some states that impose strict APR caps or limit the number of rollovers, Texas allows lenders to structure loans under credit service organization (CSO) models, which can bypass traditional interest rate limits.

This means a borrower in Fort Worth could end up paying the equivalent of 400% APR or more, depending on fees and repayment terms. For many residents, the lack of regulation feels like a double-edged sword — it gives them quick access to cash but also exposes them to potentially overwhelming costs if repayment is delayed.

Local advocacy groups have been pushing for reforms to align Texas more closely with national consumer protection standards, but for now, borrowers must navigate these rules carefully and understand exactly what they are agreeing to before signing.

The Role of Payday Loans in Fort Worth’s Economy

In Fort Worth, payday loans are more than just a financial product — they’re a part of the city’s economic ecosystem. Storefront lenders and online companies collectively serve thousands of borrowers each month, many of whom use the loans to cover essential expenses like rent, utility bills, and car repairs.

The presence of payday lenders is especially pronounced in working-class neighborhoods, where access to traditional credit may be limited. Economists have noted that payday loans, while costly, can help prevent late fees, evictions, or service disconnections, indirectly supporting local commerce.

However, critics argue that the drain on household budgets from high interest rates outweighs the short-term benefits. In essence, payday loans in Fort Worth operate in a gray area — they fill an urgent gap but often at a price that perpetuates financial instability.

Emergency Situations That Commonly Lead to Payday Loan Use

One of the defining characteristics of payday loan customers in Fort Worth is the urgency of their needs. Most borrowers aren’t using payday loans for luxuries or discretionary spending — they’re responding to unexpected expenses that threaten their immediate stability.

Medical emergencies, car breakdowns, and sudden utility shutoff notices are some of the most common triggers. For instance, imagine a single parent whose car transmission fails just days before payday; without transportation, they risk losing income, so they take out a $500 payday loan to cover the repair.

While this solves the short-term problem, it creates a new obligation that must be met within two weeks. Such scenarios illustrate why payday lending remains a popular, if controversial, option in Fort Worth — it delivers immediate relief in moments when every hour counts.

How Payday Loan Cycles Start and How to Break Them

In Fort Worth, as in many other cities, one of the biggest risks associated with payday loans is becoming trapped in a cycle of debt. The process often begins innocently — a borrower takes out a small loan with the intent to repay it in full on their next payday.

But when that paycheck arrives, other obligations compete for the same funds, making repayment in full impossible. The borrower then rolls over the loan, incurring additional fees, and the cycle begins. Over time, a single $300 loan can balloon into a series of payments far exceeding the original amount.

Breaking free from this cycle requires careful budgeting, seeking lower-cost alternatives, or negotiating with lenders for extended payment plans. Financial counselors in Fort Worth often encourage borrowers to treat payday loans as a last resort and to use them sparingly to avoid falling into this repeating pattern.

The Growth of Online Payday Lending in Fort Worth

While traditional payday loan storefronts remain a familiar sight across Fort Worth, the online payday lending sector has been expanding rapidly. Digital lenders appeal to tech-savvy consumers who value the ability to apply from their phone or laptop without leaving home.

These lenders often advertise instant approval decisions, funds deposited within 24 hours, and minimal paperwork. However, the convenience of online loans also comes with heightened risks, including predatory lenders operating without proper licenses, hidden fees, and aggressive collection practices.

Fort Worth residents are advised to verify the legitimacy of any online lender before applying, checking for state registration and customer reviews. The rise of online payday lending has undoubtedly increased access, but it has also introduced new challenges for regulators and borrowers alike, especially in distinguishing between reputable companies and scams.

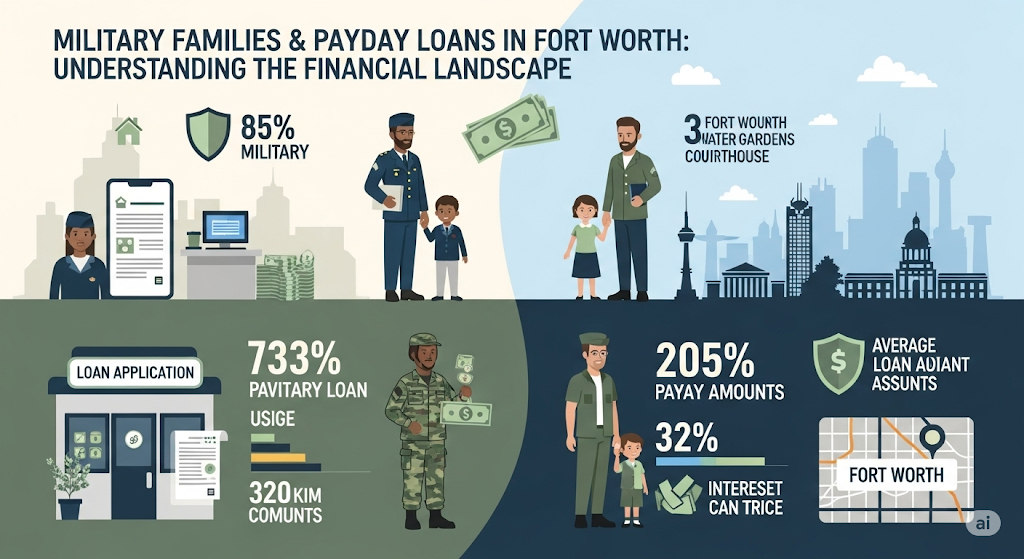

Military Families and Payday Loans in Fort Worth

Fort Worth has a significant military presence due to its proximity to several bases and its strong veteran community. While active-duty service members have some protection under the Military Lending Act, which caps payday loan APRs at 36%, veterans and their families are not always covered by the same safeguards.

This means that a veteran facing an emergency expense — such as a sudden home repair or medical bill — might still turn to a payday loan and face steep repayment costs. Military-focused advocacy groups in Fort Worth often highlight that these loans can create financial stress that undermines the stability of military households.

By promoting alternative programs such as zero-interest military relief loans, local nonprofits aim to provide safer, more affordable solutions for those who have served.

Payday Loan Alternatives Gaining Ground in Fort Worth

In recent years, Fort Worth residents have seen an expansion in payday loan alternatives designed to be more affordable and sustainable. Credit unions, for example, have begun offering small-dollar emergency loans with interest rates far below those of payday lenders.

Earned wage access programs — where employees can access a portion of their earned pay before payday — are also becoming popular among local workers. Nonprofits and faith-based organizations frequently run emergency assistance funds to help cover utility bills, rent, or essential purchases.

These alternatives not only reduce the financial burden but also help break the cycle of dependency that can come with payday loans. By making these resources more visible, Fort Worth could significantly cut down on high-interest borrowing.

How Economic Shifts Influence Payday Loan Demand

The demand for payday loans in Fort Worth often fluctuates with broader economic trends. During times of rising inflation, stagnant wages, or sudden job losses, more residents may turn to payday loans as a stopgap measure.

For example, during the COVID-19 pandemic, many households in Fort Worth saw their incomes drop sharply, leading to a surge in applications for payday loans — both online and in storefronts. Conversely, in periods of economic growth and low unemployment, demand for these loans tends to ease slightly, though never disappearing entirely.

This pattern underscores how payday loans are tightly linked to financial vulnerability, often serving as a financial lifeline when other forms of credit are unavailable.

The Cultural Perception of Payday Loans in Fort Worth

In Fort Worth, payday loans carry a complex cultural reputation. For some, they are seen as a necessary tool — a quick, no-questions-asked way to solve an urgent financial crisis. For others, they represent predatory lending that takes advantage of the most vulnerable.

Stories of neighbors, friends, and family members being trapped in cycles of debt have created a cautious awareness among many residents. Yet, in communities where banking access is limited, payday lenders are sometimes perceived as friendlier and more approachable than traditional banks.

This duality shapes public opinion and influences how people approach their own borrowing decisions, often with a mix of skepticism and necessity.

The Future of Payday Lending in Fort Worth

Looking ahead, the future of payday lending in Fort Worth will likely be shaped by a mix of regulatory changes, technological innovation, and consumer demand. If Texas lawmakers move toward tighter lending caps, traditional payday loan models could shrink, giving way to more regulated, lower-cost alternatives.

At the same time, fintech solutions — from AI-driven risk assessments to blockchain-based lending — could offer faster, more transparent options for borrowers. Community education efforts will also play a key role, ensuring residents understand both the benefits and risks of payday loans.

Ultimately, whether payday lending continues to thrive or gradually declines in Fort Worth will depend on how well the city balances the need for quick credit with the importance of long-term financial health.

FAQ – Payday Loans Fort Worth

1. What’s the maximum payday loan amount I can get in Fort Worth?

Most payday lenders in Fort Worth allow borrowing between $100 and $1,500, depending on your income and repayment ability. Some may offer slightly higher amounts for repeat customers with good repayment history.

2. How quickly can I get the money?

In most cases, storefront lenders can provide cash on the spot after approval, while online lenders can deposit funds into your account as soon as the same business day or within 24 hours.

3. Are payday loans legal in Fort Worth?

Yes, payday loans are legal in Texas, including Fort Worth. However, there’s no state-wide cap on APRs, meaning costs can be very high. Fort Worth also has local ordinances to limit excessive rollovers and encourage partial repayments.

4. Will a payday loan affect my credit score?

Generally, on-time payments are not reported to credit bureaus. However, if you default, the lender may send your account to collections, which will hurt your credit score and remain on your report for up to seven years.

5. Can I have more than one payday loan at a time?

It’s possible, but highly discouraged. Having multiple payday loans increases your risk of falling into a debt cycle, where most of your paycheck goes to repaying loan fees instead of covering living expenses.

6. What’s the average APR for payday loans in Fort Worth?

While rates vary, most payday loans in Texas have annual percentage rates (APRs) of 300% to 500%. That means a $500 loan could cost $75–$125 in just two weeks.

7. What happens if I can’t pay on time?

If you miss your payment, lenders may charge late fees, NSF (non-sufficient funds) fees, and attempt to withdraw funds from your bank account multiple times. This can also trigger overdraft charges from your bank.

8. What are the safest alternatives to payday loans in Fort Worth?

Safer alternatives include:

- Credit Union Payday Alternative Loans (PALs) with low APRs

- Employer paycheck advances

- Local nonprofits and charities offering emergency grants or no-interest loans

- Negotiating payment extensions with utility or medical providers

9. Do online payday loans follow the same rules as storefront loans?

Yes — any payday lender serving Fort Worth residents must be licensed in Texas. However, online lenders often have different fee structures and may charge additional service or transfer fees, so read the terms carefully.

10. How can I avoid getting trapped in payday loan debt?

The best strategies include:

- Borrowing only the amount you can repay in full on time

- Exploring alternative funding sources first

- Avoiding rollovers or extensions

- Creating a monthly emergency fund to reduce future reliance on payday loans