Introduction to Payday Loans in Baton Rouge, LA

Baton Rouge, Louisiana’s bustling capital city, is known for its diverse economy, rich cultural heritage, and a mix of industries ranging from petrochemicals to healthcare and education. Despite the city’s economic strengths, thousands of residents face unexpected financial challenges every year.

A blown tire, sudden medical co-pay, or an overdue electric bill can quickly create a cash-flow crisis — especially for households living paycheck to paycheck. According to a Louisiana Budget Project analysis, nearly 40% of Louisiana residents lack enough savings to cover a $400 emergency.

For many in Baton Rouge, one quick-fix option is a payday loan — a small, short-term, high-interest loan designed to be repaid on the borrower’s next payday. While payday loans can provide immediate access to funds, they also come with extremely high costs that can trap borrowers in cycles of debt if not managed carefully.

In this guide, we’ll explore how payday loans work in Baton Rouge, the laws that govern them, the pros and cons, and practical alternatives that can help residents make smarter financial choices.

How Payday Loans Work in Louisiana

In Louisiana, payday loans are formally referred to as “Deferred Presentment Transactions.” This term means the borrower writes a post-dated check or authorizes an electronic bank debit for the loan amount plus fees, and the lender agrees to hold that payment until the borrower’s next payday.

In Baton Rouge, payday loans are available both in-store and online. The basic process is simple:

- You apply with proof of income, a valid ID, and an active checking account.

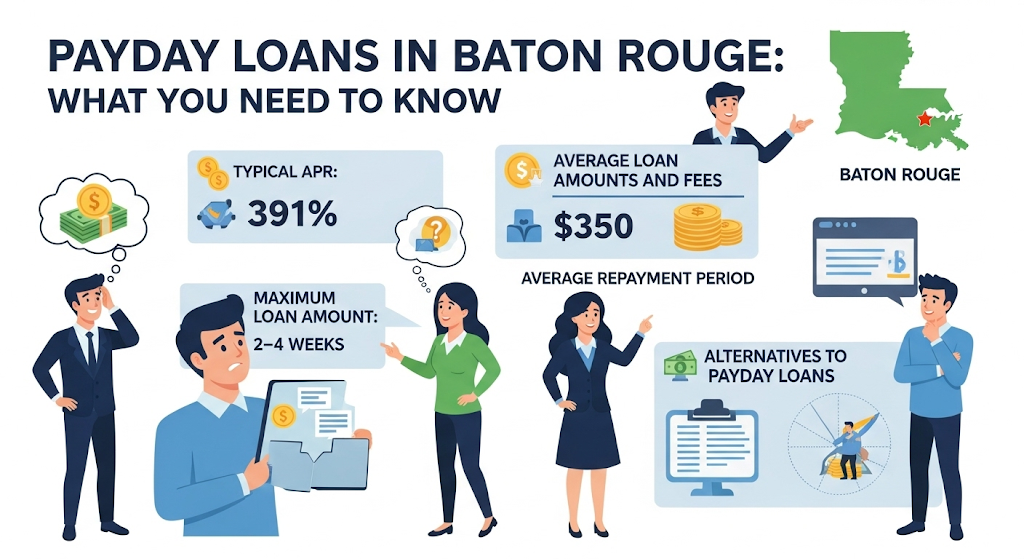

- The lender determines eligibility and loan amount (up to $350).

- You receive cash or a bank deposit, often within minutes.

- On your next payday, the lender deposits your check or processes the electronic debit.

While the process sounds straightforward, the real complexity lies in the costs and repayment terms. Louisiana law allows lenders to charge $20 per $100 borrowed plus a $10 documentation fee. On a $350 loan with a 14-day term, this equates to an APR exceeding 520% — far above typical credit card interest rates.

Louisiana-Specific Payday Loan Laws and Consumer Protections

Louisiana’s payday lending industry is regulated by the Louisiana Office of Financial Institutions (OFI), which enforces rules designed to protect consumers from the worst lending abuses.

Key Regulations:

- Maximum Loan Amount: $350

- Maximum Loan Term: 60 days

- APR Cap: No cap in percentage terms, but fees are limited to $20 per $100 borrowed + $10 documentation fee

- No Rollovers: Borrowers cannot extend the term by paying only the fees; the loan must be paid in full

- Extended Payment Plan: Once per year, a borrower who cannot repay may request a 60-day payment plan without additional fees

The law also requires lenders to provide a written contract outlining all fees, due dates, and repayment terms. In-store lenders must post their license and a fee schedule in plain sight.

For Baton Rouge residents, this means you have the right to see all charges upfront and to verify your lender’s license before signing anything. You can search the OFI’s public database to confirm a lender’s legitimacy.

Pros & Cons of Payday Loans in Baton Rouge

Like any financial product, payday loans have advantages and disadvantages.

Advantages:

Payday loans provide fast access to cash with minimal paperwork and no traditional credit check. This makes them attractive for people with poor or limited credit histories. In an emergency, when other funding sources aren’t available, they can prevent bounced checks, utility shutoffs, or late rent fees.

Disadvantages:

The biggest drawback is cost. With APRs exceeding 500%, payday loans in Baton Rouge are among the most expensive credit options available. The short repayment timeline (often just two weeks) can make repayment difficult, leading to repeat borrowing. According to the Center for Responsible Lending, the average Louisiana payday borrower takes out 8–10 loans per year, paying hundreds of dollars in fees for a few hundred borrowed

Payday Loan Statistics & Their Impact in Louisiana

The payday loan industry has a significant presence in Louisiana. Baton Rouge alone has dozens of storefront lenders, many located in low-income neighborhoods.

- Usage Rate: Nearly 12% of Louisiana adults use payday loans annually — one of the highest rates in the country.

- Repeat Borrowing: 80% of loans are taken out within two weeks of a previous loan being repaid.

- Fee Drain: Louisiana consumers pay an estimated $240 million in payday loan fees each year, much of which flows to out-of-state corporate lenders rather than staying in the local economy.

For Baton Rouge, this means millions of dollars leave the community annually — money that could otherwise be spent at local businesses, invested in savings, or used for long-term financial stability.

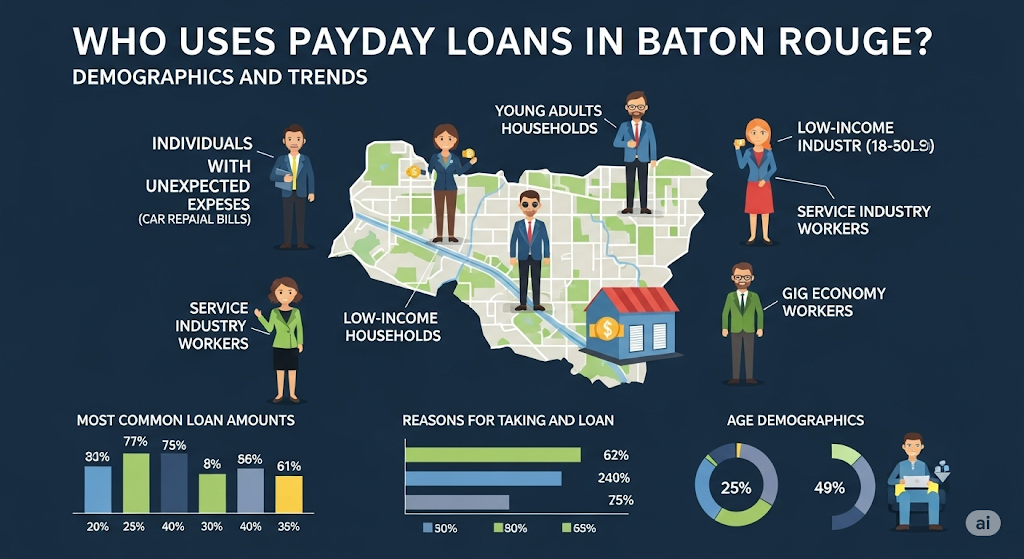

Who Typically Uses Payday Loans in Baton Rouge?

Payday loan borrowers in Baton Rouge come from diverse backgrounds, but most share a common challenge — limited access to affordable credit. Research from the Pew Charitable Trusts shows that payday loan users tend to have annual household incomes below $40,000, and many work in jobs where pay is stable but low, leaving little room for emergencies.

In Baton Rouge, common borrower groups include:

- Service industry workers such as waitstaff, retail clerks, and hotel employees, whose schedules and tips can be unpredictable.

- Healthcare support staff like nursing assistants or home health aides, who often face modest pay despite working long hours.

- Public sector employees such as school staff or municipal workers, who may face delays in overtime or bonus payments.

- Gig economy workers, including rideshare drivers and delivery couriers, who may not have benefits like paid sick leave or employer-based loans.

While payday loans can offer quick relief, these borrowers often find themselves borrowing again before their next paycheck, leading to a cycle of dependency that’s hard to break.

Alternatives to Payday Loans Available in Baton Rouge

Before committing to a payday loan, residents should explore safer and more affordable alternatives. Several options exist locally in Baton Rouge that can provide short-term cash without the crushing fees of payday lending.

Credit Union Small-Dollar Loans – Many Louisiana credit unions offer Payday Alternative Loans (PALs) regulated by the National Credit Union Administration (NCUA). These loans typically have APRs capped at 28% and repayment terms up to six months.

Employer-Based Advances – Some Baton Rouge employers partner with fintech services to provide earned wage access, allowing workers to access a portion of their paycheck before the official payday.

Nonprofit & Faith-Based Aid – Organizations like the Capital Area United Way and Catholic Charities of Baton Rouge offer emergency grants or zero-interest loans for rent, utilities, and other essentials.

Utility Payment Arrangements – Local utilities such as Entergy Louisiana often have hardship programs or payment extensions that can prevent shutoffs without resorting to payday borrowing.

Choosing an alternative can mean the difference between paying back a manageable amount over time and falling into a cycle of payday loan rollovers.

How to Validate a Licensed Payday Lender in Baton Rouge

One of the most important steps before taking a payday loan is verifying that the lender is licensed by the Louisiana Office of Financial Institutions (OFI). Unlicensed lenders — especially online ones — can charge illegal rates, hide fees, or use aggressive collection tactics.

Steps to Verify a Lender:

- Visit the Louisiana OFI website and search the lender’s name in the public license database.

- Check for a visible license certificate displayed at the storefront or listed on the website.

- Review the posted fee schedule; state law requires this to be in plain view for customers.

- Read reviews and complaints on the Better Business Bureau (BBB) or Consumer Financial Protection Bureau (CFPB) complaint database.

Borrowing from an unlicensed lender is risky because you may have little legal recourse if something goes wrong. In Baton Rouge, where dozens of payday shops compete for customers, sticking to a licensed provider is the safest choice.

Risks of Defaulting on a Payday Loan in Louisiana

Failing to repay a payday loan in Baton Rouge can trigger a series of expensive and stressful consequences. If the lender deposits your post-dated check and your account lacks sufficient funds, you’ll incur bank overdraft fees — often $35 or more per transaction.

Lenders may also initiate collection efforts, which can include:

- Frequent calls and letters from collection agencies

- Negative reporting to credit bureaus if the account is sold to collections

- Possible legal action in small claims court to recover the debt

It’s important to note that Louisiana law prohibits arrest or criminal charges for unpaid payday loans. However, some unscrupulous collectors have been known to threaten jail time — a tactic that is illegal under both state and federal law.

Default can create a debt spiral: as fees and interest accumulate, the borrower may feel forced to take out another payday loan to cover the original, deepening the problem.

Online vs. Storefront Payday Lenders — What Works Best for Baton Rouge Borrowers?

Baton Rouge borrowers can choose between online payday lenders and physical storefronts, each with unique pros and cons.

Online Payday Loans offer unmatched convenience — applications can be completed 24/7 from home, and funds are typically deposited the next business day. This option is especially useful for those without transportation or with irregular schedules. However, online lending carries a higher risk of encountering unlicensed operators, making verification crucial.

Storefront Lenders provide face-to-face interactions, immediate cash upon approval, and the assurance that you’re dealing with a local, licensed business. The downside is limited operating hours and the need to travel to the location, which may not be practical for everyone.

For many in Baton Rouge, the choice depends on urgency, trust, and convenience. Those who value personal interaction and same-day cash may prefer storefronts, while those comfortable navigating online verification may opt for digital lenders.

Predatory Practices & Payday Loan Scams in Louisiana

While most licensed payday lenders in Baton Rouge follow state laws, there are still predatory practices and outright scams targeting vulnerable borrowers. These unethical tactics often exploit people in urgent financial need.

Common Predatory Behaviors:

- Loan flipping – Encouraging borrowers to immediately take out a new loan after repaying the old one, trapping them in repeated high-fee cycles.

- Hidden fees – Adding charges not disclosed in the original contract, such as processing or “membership” fees.

- Aggressive collections – Using threats of arrest, harassment at the workplace, or contacting friends and family to pressure repayment.

- Bait-and-switch – Advertising a low-interest installment loan, then switching the borrower to a high-cost payday loan upon application.

Scam Red Flags:

- Lenders who demand upfront payment before loan approval.

- Requests for sensitive personal information via email or text without secure encryption.

- Lack of a Louisiana OFI license or refusal to show proof of licensing.

Baton Rouge residents can protect themselves by using only licensed lenders, keeping written records of all agreements, and reporting suspected scams to the Louisiana Attorney General’s Consumer Protection Section.

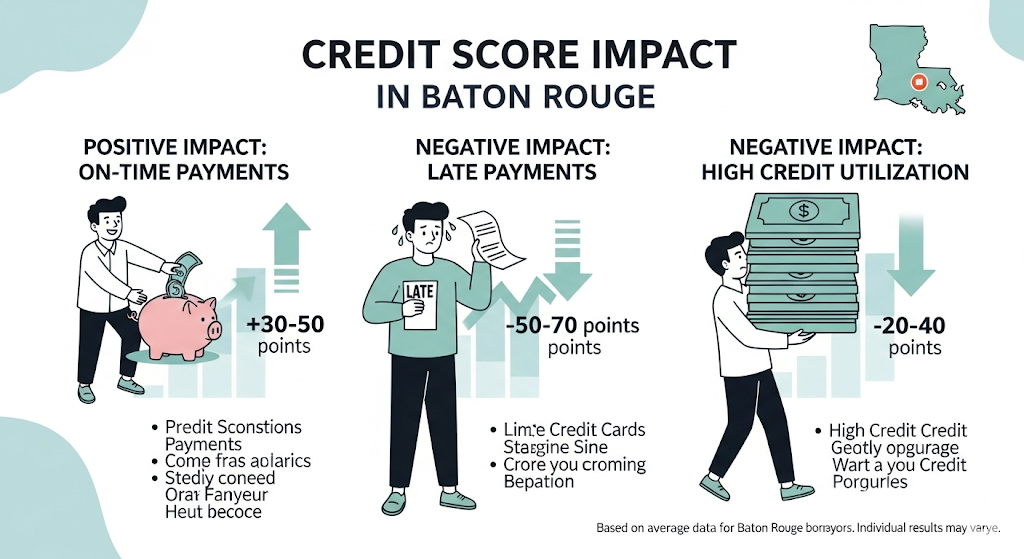

Impact on Credit Score — What Baton Rouge Borrowers Should Know

Payday loans in Louisiana generally do not improve your credit score, because most lenders don’t report on-time payments to major credit bureaus. However, they can negatively impact your credit if you default and the debt is sold to a collection agency.

Potential Credit Consequences:

- Collections accounts remain on your credit report for up to 7 years, lowering your score.

- Missed payments can lead to increased borrowing costs for future loans, as lenders see you as higher risk.

- Negative credit history can make it harder to rent an apartment or secure employment in certain industries.

If building or repairing credit is your goal, Baton Rouge borrowers may be better served by secured credit cards, credit-builder loans from local credit unions, or on-time payments for utilities and rent reported through services like Experian Boost.

Military Protections Under the Military Lending Act in Louisiana

Baton Rouge is home to many active-duty military personnel, veterans, and their families — particularly due to its proximity to bases like Camp Beauregard and other Louisiana installations. These borrowers receive additional protections under the Military Lending Act (MLA).

Key MLA Provisions:

- APR Cap of 36% — much lower than Louisiana’s typical payday loan rates.

- Ban on certain terms such as mandatory arbitration clauses and prepayment penalties.

- Mandatory disclosures to ensure military members fully understand the loan terms.

Military borrowers are also encouraged to explore alternatives like Army Emergency Relief or Navy-Marine Corps Relief Society, which offer interest-free or low-interest emergency loans for qualified expenses.

How Payday Loans Affect the Baton Rouge Economy

The payday lending industry extracts significant amounts of money from Baton Rouge each year. According to advocacy research, Louisiana borrowers pay over $240 million in payday loan fees annually, with a large share coming from the Baton Rouge metro area.

This fee drain has several consequences:

- Reduced local spending — Money that could support small businesses is instead sent to out-of-state corporate headquarters.

- Weakened community wealth — Households paying repeated fees have less to save or invest, hindering long-term financial security.

- Increased demand for public assistance — High-cost borrowing can exacerbate financial instability, pushing more residents to rely on state-funded aid.

Advocates argue that reforming payday lending laws could keep millions of dollars circulating in Baton Rouge’s economy, benefiting local growth instead of corporate profits.

The Push for Reform — Proposed Laws and Consumer Advocacy

Over the past decade, Louisiana lawmakers and consumer advocates have repeatedly proposed reforms to address payday loan costs and abusive practices. One prominent proposal has been to cap interest rates at 36% APR, similar to the MLA protections for military members.

Notable Reform Efforts:

- HB 675 (2021) — Proposed stricter rate caps and longer repayment terms but stalled in committee.

- Community advocacy from groups like the Louisiana Budget Project and Together Louisiana, which lobby for lower fees and expanded alternatives.

- Faith-based campaigns calling for ethical lending practices as part of broader anti-poverty initiatives.

While these reforms have faced strong opposition from payday lending lobbyists, public pressure continues to grow in Baton Rouge and across the state. The outcome of future legislative sessions could dramatically reshape the payday lending landscape in Louisiana.

Responsible Borrowing Tips for Baton Rouge Residents

If you decide to take out a payday loan in Baton Rouge, using it responsibly can make the difference between short-term relief and long-term debt. The most important principle is to borrow only what you can repay on your next payday without sacrificing essentials like rent, food, or utilities.

Start by creating a repayment plan before you even apply. Calculate your upcoming paycheck, subtract fixed expenses, and see if the loan amount plus fees fit into your budget. If it doesn’t, consider requesting a smaller loan or exploring other options.

Avoid back-to-back borrowing, as this is the fastest way to fall into a debt cycle. Instead, use payday loans as a one-time emergency tool and work toward building a small emergency savings fund for future crises.

Digital Trends in Payday Lending in Louisiana

In recent years, payday lending in Baton Rouge has increasingly moved online. According to industry data, over 40% of payday loans in Louisiana are now originated digitally, with borrowers applying from smartphones or computers.

Benefits of Digital Lending:

- 24/7 access to applications

- Faster approval times, often within minutes

- No need to visit a physical location

Risks:

- Higher exposure to unlicensed lenders operating from outside the U.S.

- Increased risk of data breaches if sites lack strong security

- Less personal interaction, which can make it harder to clarify loan terms

For Baton Rouge residents, the convenience of online lending is undeniable — but it’s critical to verify a lender’s license and read all terms carefully before submitting sensitive information.

Baton Rouge Case Study — Payday Loan Cycle Example

Consider the case of “Maria,” a Baton Rouge retail worker earning $12 an hour. When her car broke down, she took a $300 payday loan to cover repairs. The lender charged $60 in fees, due in 14 days.

When payday arrived, Maria found she couldn’t cover the $360 repayment without missing her rent. She rolled the loan over, paying another $60 fee. Within three months, Maria had paid $240 in fees — almost as much as she borrowed — and still owed the original $300.

This example highlights how quickly costs can spiral, especially when borrowers lack alternative credit options. Maria eventually sought help from a local credit union offering a small installment loan with a lower interest rate and longer repayment term.

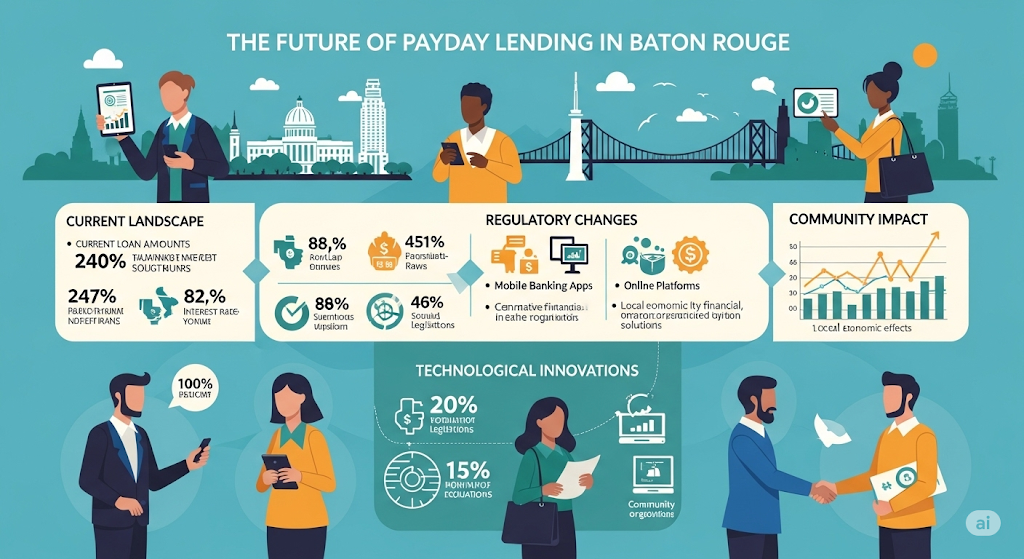

The Future of Payday Loans in Baton Rouge

The payday lending industry in Baton Rouge faces significant change over the next few years. Several factors will likely shape its future:

- Regulatory reforms — Pressure is mounting for Louisiana lawmakers to lower rates and expand repayment options.

- Fintech competition — Apps offering earned wage access and small-dollar installment loans are already cutting into payday lenders’ market share.

- Consumer education — Public awareness campaigns by nonprofits and state agencies are helping residents make more informed borrowing decisions.

If reforms succeed, Baton Rouge borrowers could soon see lower-cost, more transparent short-term lending options that provide financial flexibility without the high risk of debt traps.

Final Thoughts — Borrowing Smarter in Baton Rouge

Payday loans in Baton Rouge, LA, are a double-edged sword — they can be a quick solution in a cash crunch but come with sky-high costs that can create lasting financial strain. By understanding Louisiana payday loan laws, recognizing the risks, and exploring safer alternatives, residents can make informed choices that protect their long-term financial health.

The smartest approach is to view payday loans as an absolute last resort and to actively build a safety net through savings, credit union membership, or employer assistance programs. In a city as vibrant and resourceful as Baton Rouge, there are always better paths to financial stability than falling into the payday loan cycle.

FAQs About Payday Loans in Baton Rouge, LA

1. What is the maximum payday loan amount in Louisiana?

The maximum allowed is $350 per loan under state law.

2. How long do I have to repay a payday loan in Baton Rouge?

Loan terms are typically between 14 and 60 days.

3. Can I get more than one payday loan at a time?

Yes, but doing so increases your risk of falling into a debt cycle.

4. What fees can lenders charge in Louisiana?

Up to $20 per $100 borrowed, plus a $10 documentation fee.

5. Do payday loans affect my credit score?

Not usually, unless you default and the debt goes to collections.

6. Are online payday lenders legal in Baton Rouge?

Yes, if they are licensed by the Louisiana OFI.

7. Can military members take payday loans in Louisiana?

Yes, but they are protected by the MLA’s 36% APR cap.

8. What happens if I can’t repay on time?

You may face overdraft fees, collections, and legal action in civil court.

9. Are there safer alternatives to payday loans?

Yes — credit union PALs, employer advances, and nonprofit aid.

10. How can I check if a payday lender is licensed?

Search the lender’s name on the Louisiana OFI public license database.