Introduction – Why Payday Loans Are in High Demand in Denver

Denver, Colorado, is one of the fastest-growing cities in the U.S., with a booming population, rising living costs, and a dynamic job market. But even in a thriving economy, many residents face short-term cash crunches. From unexpected car repairs to emergency medical bills, financial surprises can disrupt even the most carefully planned budgets.

Payday loans in Denver have become a go-to solution for residents who need quick access to cash — often in as little as a few hours. While these loans offer speed and convenience, they also come with high interest rates and potential risks if not managed properly.

Data Insight: According to the Colorado Attorney General’s Office, payday loan usage in Colorado still accounts for tens of millions in lending annually, despite regulatory caps on APR and fees.

Example:

Maria, a Denver restaurant worker, found herself short on rent after an unexpected dental bill. She used a $500 payday loan to cover the gap, ensuring she avoided eviction fees — but later realized the total repayment was $615 after fees.

Understanding Payday Loans in Denver – How They Work

Before taking out a payday loan, it’s essential to understand the mechanics. In Denver, payday loans are small, short-term loans, typically between $100 and $1,000, designed to be repaid on your next payday.

Key Features of Payday Loans in Denver:

- Fast Approval: Most lenders offer approval within minutes.

- Minimal Requirements: Generally require ID, proof of income, and a bank account.

- Short-Term Repayment: Usually due in 14–30 days.

- APR Caps in Colorado: State law limits APR and fees to prevent extreme debt cycles.

How It Works:

- Apply online or in person.

- Provide income proof and banking details.

- Receive funds — often the same day.

- Repay with fees on your next payday.

Pro Tip: Colorado law now requires loans to be structured in a way that allows installment payments, reducing the “rollover” trap common in other states.

The Pros and Cons of Payday Loans in Denver

Like any financial product, payday loans have both benefits and drawbacks.

Advantages:

- Quick access to cash when emergencies strike.

- Minimal documentation compared to traditional bank loans.

- Available even with bad credit.

- Convenient online or in-store application options.

Disadvantages:

- Higher APRs compared to personal loans or credit cards.

- Short repayment windows can create repayment pressure.

- Can lead to debt cycles if borrowed repeatedly.

- Limited loan amounts may not cover larger emergencies.

Example:

James, a Denver rideshare driver, used payday loans three times in six months. While the first loan helped him cover car repairs, repeated borrowing created a cycle where he was always paying off one loan while taking another.

Payday Loan Regulations in Denver, Colorado

Colorado is one of the few states with stricter payday loan laws, aiming to protect consumers from predatory lending.

Important Colorado Payday Loan Laws:

- APR Cap: Capped at 36% for payday loans, plus allowable fees.

- Loan Term: Must be at least 6 months, allowing borrowers more time to repay.

- Rollover Limitations: Lenders cannot indefinitely roll over loans.

- Maximum Loan Amount: Generally up to $1,000.

Impact on Borrowers:

These regulations have significantly reduced the risk of borrowers falling into long-term debt. According to state data, consumer complaints about payday lenders have dropped by nearly 30% since the new laws took effect in 2010.

When to Consider a Payday Loan in Denver

Payday loans should be considered a last resort, not a primary financial tool.

Situations Where a Payday Loan Might Make Sense:

- Emergency medical expenses not covered by insurance.

- Urgent car repairs needed to keep working.

- Avoiding utility shut-offs or eviction.

- Covering essential expenses before a confirmed paycheck.

Alternatives to Consider First:

- Borrowing from friends or family.

- Using a credit card (if interest rates are lower).

- Seeking community assistance programs.

- Negotiating payment extensions with service providers.

Example:

Tina, a single mother in Denver, avoided losing her apartment by taking out a $350 payday loan to cover late rent. She repaid it within two weeks without additional fees because she budgeted carefully.

How to Find Reputable Payday Loan Lenders in Denver

Not all payday loan providers are created equal, and choosing the wrong lender can lead to unnecessary fees, aggressive collection tactics, or even scams.

PHG:

In Denver, you should only work with lenders licensed by the Colorado Department of Law – Consumer Protection Division. Licensed lenders must follow state regulations on interest rates, loan terms, and fair lending practices.

Steps to Identify a Reputable Lender:

- Verify Licensing: Search the lender’s name on Colorado’s official lender registry.

- Read Reviews: Check Google, Yelp, and Better Business Bureau ratings.

- Transparent Terms: A good lender will give you a written breakdown of APR, total repayment, and fees before you sign.

- Physical Address: Legitimate lenders have a verifiable office location, not just a PO box or vague online presence.

Example:

Aaron needed $700 for urgent plumbing repairs. He checked the Colorado lender registry, read online reviews, and chose a storefront lender in Lakewood with a clear fee structure — avoiding hidden charges.

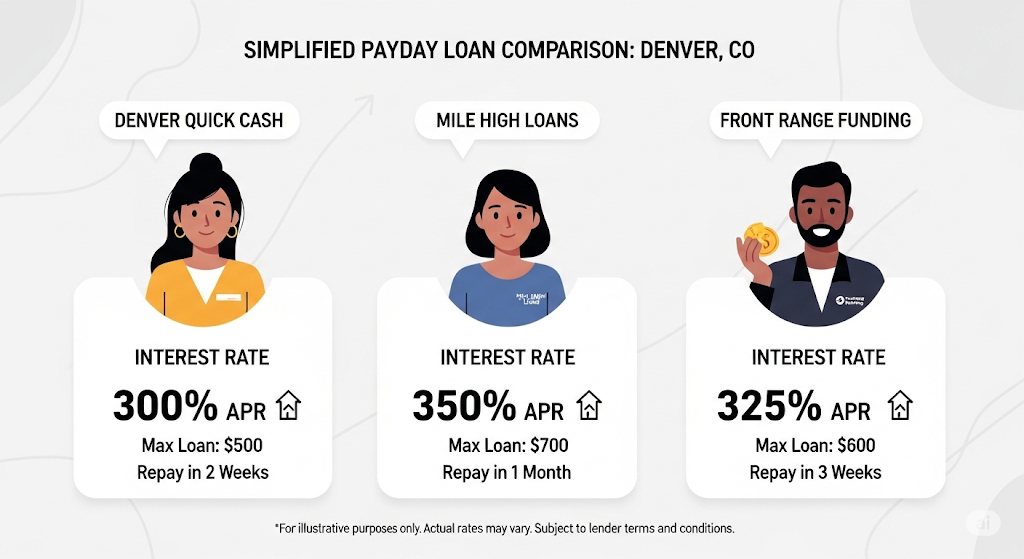

Comparing Payday Loan Offers in Denver

Choosing the first lender you find can be costly. By comparing offers, you can save money and reduce repayment stress.

Points to Compare:

- APR and Fees: Even with Colorado’s cap, fees can differ between lenders.

- Repayment Terms: Some lenders allow installment plans instead of a lump-sum payment.

- Early Repayment Penalties: Look for lenders that waive fees if you repay early.

- Loan Amount Flexibility: Some lenders allow you to borrow less than the maximum to minimize debt.

Data Insight:

A 2023 Colorado consumer finance report showed that borrowers who compared at least 3 lenders saved an average of $45 per $500 loan.

Example:

Sarah compared three Denver payday lenders. By choosing the one with the lowest fees, she repaid $560 instead of $590 for the same $500 loan.

Avoiding Payday Loan Scams in Denver

Unfortunately, the payday lending space attracts scammers looking to exploit vulnerable borrowers.

PHG – Red Flags to Watch Out For:

- Upfront Fees: Legit lenders only charge after approving and disbursing your loan.

- No Licensing Info: If a lender can’t provide their Colorado license number, walk away.

- Pressure Tactics: Pushing you to sign immediately without explaining terms.

- Email Domains That Don’t Match: e.g., a lender claiming to be in Denver using an unrelated foreign domain.

Example:

Melissa applied for an “instant approval” online payday loan. She was asked for a $50 “processing fee” via gift card — a classic scam. She lost the money and never received a loan.

Pro Tip:

Always check lender legitimacy through the Colorado Attorney General’s website before giving out personal information.

Seasonal Trends in Payday Loan Usage in Denver

Demand for payday loans in Denver fluctuates throughout the year, often tied to seasonal financial pressures.

Common Peak Periods:

- December – January: Holiday spending, heating bills, and New Year expenses.

- August – September: Back-to-school costs for families.

- April: Tax bills and federal income tax shortfalls.

Data Insight:

Denver-area lenders report a 28% spike in payday loan applications in December, making it the highest-demand month of the year.

Example:

David, a Denver HVAC technician, took out a payday loan in January to cover heating bills during a particularly cold winter. He repaid it in February after a seasonal work bonus.

The Role of Fintech in Denver’s Payday Loan Market

Technology is reshaping how payday loans are accessed in Denver. Many lenders now operate fully online or through mobile apps, streamlining the borrowing process.

Advantages of Fintech Payday Lending:

- Faster Approvals: AI-driven underwriting can approve loans in under 15 minutes.

- 24/7 Applications: No need to wait for business hours.

- Automated Repayments: Payments deducted automatically on due dates.

- Better Tracking: Borrowers can view real-time balances and repayment schedules.

Example:

Carlos applied for a $400 payday loan on his lunch break using a mobile app. The funds hit his account within 30 minutes, avoiding an overdraft fee on his checking account.

Future of Payday Loan Regulations in Denver

Colorado’s payday loan laws have already gone through major reforms — and more changes could be on the horizon.

PHG:

State regulators have been exploring additional consumer protections to further reduce debt traps. Proposed ideas include lower APR caps, mandatory installment repayment options, and limits on the number of payday loans a borrower can take per year.

Potential Impacts:

- Pros for Consumers: Lower costs and fewer rollovers, making loans more manageable.

- Cons for Lenders: Possible reduction in store locations or tighter qualification standards.

Example:

Back in 2019, when Colorado reduced the maximum APR, several high-fee lenders closed their Denver branches — but community credit unions stepped in with more affordable short-term loan alternatives.

Payday Loans and Your Credit Score

Many Denver borrowers believe that payday loans help build credit, but this is rarely the case.

PHG – The Truth:

- Most payday lenders don’t report positive payment history to major credit bureaus.

- If a loan goes unpaid and gets sent to collections, your credit score can drop significantly.

- Lenders may check your bank activity, but they rarely perform hard credit pulls.

Pro Tip:

If your goal is credit improvement, consider secured credit cards, credit-builder loans, or small installment loans from local Denver credit unions.

Example:

Jake took three payday loans over six months and paid them all on time — but his credit score stayed the same. When one loan payment was late and sent to collections, his score dropped by 58 points.

How to Compare Denver Payday Loan Offers the Smart Way

Before you commit, comparison shopping can save you significant money.

Key Factors to Compare:

- Total Repayment Amount: Not just the fee — the final figure you’ll pay.

- Loan Term: Shorter terms mean faster payoff but higher per-payment costs.

- APR vs. Flat Fees: Know exactly how fees translate into annual percentage rates.

- Repayment Flexibility: Some lenders allow partial payments or extensions without penalties.

Data Insight:

Denver borrowers who compare at least 3 different offers save an average of $40–$60 per loan.

Example:

Sandra needed $350 quickly. By comparing 4 lenders, she chose one with an APR 10% lower than the highest offer — saving $18 in fees.

Community and Nonprofit Loan Assistance in Denver

Denver is home to several organizations offering low-interest or no-interest loan alternatives to payday lending.

Examples Include:

- Denver Community Credit Union: Offers Payday Alternative Loans (PALs) with much lower APR.

- The Salvation Army Emergency Assistance Program: Helps with utility bills, rent, and food.

- Mile High United Way: Provides referrals for emergency financial aid.

PHG – Why Use These Programs:

They reduce the need for high-cost payday loans, help you avoid debt spirals, and often include financial counseling for long-term stability.

Example:

Deborah avoided a $500 payday loan by getting a PAL from her local credit union for just a $10 application fee and zero interest.

Smarter Borrowing: When a Payday Loan in Denver Makes Sense

While payday loans are high-cost, they can still serve a purpose if used strategically.

When It May Be Justified:

- Covering urgent bills to avoid costly late fees or utility shut-offs.

- Bridging a very short gap before a guaranteed source of income.

- Emergency travel or unexpected car repairs that can’t wait.

Smart Borrowing Tips:

- Only borrow what you can repay on your next payday.

- Avoid rollovers — they multiply costs quickly.

- Have a clear repayment plan before signing.

Example:

Mark borrowed $300 to cover a late rent fee to avoid eviction. He repaid it within two weeks when his overtime paycheck arrived, preventing any long-term financial damage.

Payday Loan Alternatives in Denver That Save You Money

Instead of locking yourself into high-interest payday debt, Denver offers multiple low-cost loan options.

PHG – Top Alternatives:

- Credit Union PALs: Payday Alternative Loans capped at low APRs.

- Employer Salary Advances: Many Denver employers offer interest-free paycheck advances.

- Local Nonprofits: Organizations like Mile High United Way help cover bills directly.

Why These Work Better:

- Lower fees mean more savings.

- No risk of falling into a debt cycle.

- Often paired with financial counseling for long-term improvement.

Example:

Lisa needed $400 for urgent dental work. Instead of a payday loan, she got an employer advance, repaid interest-free over two months.

How Denver Borrowers Can Avoid the Debt Trap

A payday loan should be a bridge — not a pit you fall into.

PHG – Debt Avoidance Strategies:

- Budget for Emergencies: Set aside at least $25–$50 per paycheck.

- Negotiate With Creditors: Many utilities and landlords in Denver offer payment plans.

- Seek Financial Counseling: Denver Public Library and nonprofits offer free sessions.

Key Warning Signs of a Debt Trap:

- Needing a new loan to pay off the old one.

- Loan fees exceeding the original borrowed amount.

- Skipping essential expenses to make repayments.

Seasonal Payday Loan Trends in Denver

Payday loan demand in Denver spikes at certain times of year due to seasonal financial pressures.

Peak Borrowing Seasons:

- December–January: Holiday shopping and high heating bills.

- August–September: Back-to-school expenses.

- April: Tax deadlines and IRS payments.

Data Insight:

Local lenders report a 30% surge in loan applications during December alone.

Example:

In December, Kelly borrowed $300 for gifts but rolled it over twice due to heating costs — ending up paying $480 total.

Digital Payday Lending in Denver – Pros and Cons

Fintech has made payday loans more accessible, but also riskier in some cases.

PHG – Pros:

- Fast online approval (often under 1 hour).

- No need for physical visits.

- Convenient mobile repayment tracking.

PHG – Cons:

- Easier access can encourage impulse borrowing.

- Some online lenders are out-of-state and not bound by Colorado laws.

- Higher risk of scams without proper verification.

Pro Tip:

Only borrow from lenders licensed by the Colorado Department of Law – Consumer Protection Division.

Conclusion – The Smarter Path Forward for Denver Borrowers

Payday loans in Denver should be treated as a last-resort financial tool. While state laws protect consumers from extreme fees, the high cost still makes them risky.

Key Takeaways:

- Always explore low-interest alternatives first.

- Borrow only if repayment is guaranteed within your next paycheck.

- Compare multiple lenders to minimize costs.

- Verify licenses to avoid scams.

Final Word:

Financial emergencies are stressful — but with planning, resource awareness, and smart decision-making, you can avoid high-cost debt and keep more money in your pocket.

Frequently Asked Questions – Payday Loans in Denver

1. Are payday loans legal in Denver, Colorado?

Yes. Payday loans are legal in Denver, but they are regulated under Colorado’s Deferred Deposit Loan Act. This law sets maximum loan amounts, fee limits, and repayment terms to protect borrowers from excessive costs.

2. How much can I borrow with a payday loan in Denver?

In Colorado, payday loans are generally capped at $500. However, repayment terms are longer than in many states — often allowing up to six months to repay.

3. What is the maximum interest rate for payday loans in Denver?

Colorado law caps the annual percentage rate (APR) on payday loans at 36%, plus a small origination fee. This is much lower than the 300–500% APR seen in unregulated states.

4. Can I get an online payday loan in Denver?

Yes, but it’s important to verify that the online lender is licensed to operate in Colorado. Many out-of-state lenders are not bound by local regulations and may charge illegal rates.

5. What do I need to qualify for a payday loan in Denver?

Typical requirements include:

- Valid government-issued ID

- Proof of income or employment

- Active checking account

- Being at least 18 years old

6. How quickly can I get a payday loan in Denver?

Most storefront lenders offer same-day cash. Online applications can fund within 24 hours, sometimes in as little as one hour if approved early in the day.

7. Can payday loans in Denver help build my credit?

Usually no. Most payday lenders do not report positive repayment history to credit bureaus — but late or unpaid loans sent to collections can damage your score.

8. What happens if I can’t repay my payday loan in Denver?

If you can’t pay, the lender may offer a repayment plan, but rolling over the loan adds more fees. Default could result in collections, additional charges, and negative credit reporting.

9. Are there safer alternatives to payday loans in Denver?

Yes, such as:

- Credit union Payday Alternative Loans (PALs)

- Employer paycheck advances

- Nonprofit emergency assistance programs

10. How can I check if a payday lender is licensed in Colorado?

You can verify a lender’s license through the Colorado Department of Law – Consumer Protection Division website.