Payday Loans in Memphis, Tennessee, is a vibrant city with a rich cultural heritage, but like many urban areas in America, it’s also a place where residents face financial challenges. From unexpected car repairs to emergency medical bills, sudden expenses can strain even the most carefully planned budget. For many Memphians, payday loans present a quick, accessible solution when cash is tight. These small-dollar, short-term loans are designed to bridge the gap between paychecks, offering immediate relief but also carrying significant financial risks if not managed wisely.

In Memphis, payday loans are readily available both online and in storefront locations. While their speed and convenience are undeniable, their high fees and short repayment terms often make them a controversial financial product. Understanding how payday loans work, the rules that govern them in Tennessee, and the potential alternatives is essential before deciding whether to borrow. This article dives deep into every aspect of payday lending in Memphis so you can make informed choices that protect your financial health.

How Payday Loans Work in Tennessee: A Step-by-Step Guide

Payday loans in Tennessee operate under rules set by the Tennessee Deferred Presentment Services Act. The process is straightforward: a borrower writes a post-dated check or authorizes an electronic withdrawal for the loan amount plus fees, which the lender holds until the borrower’s next payday. When that date arrives—typically within 14 to 31 days—the lender cashes the check or withdraws the funds directly from the borrower’s bank account.

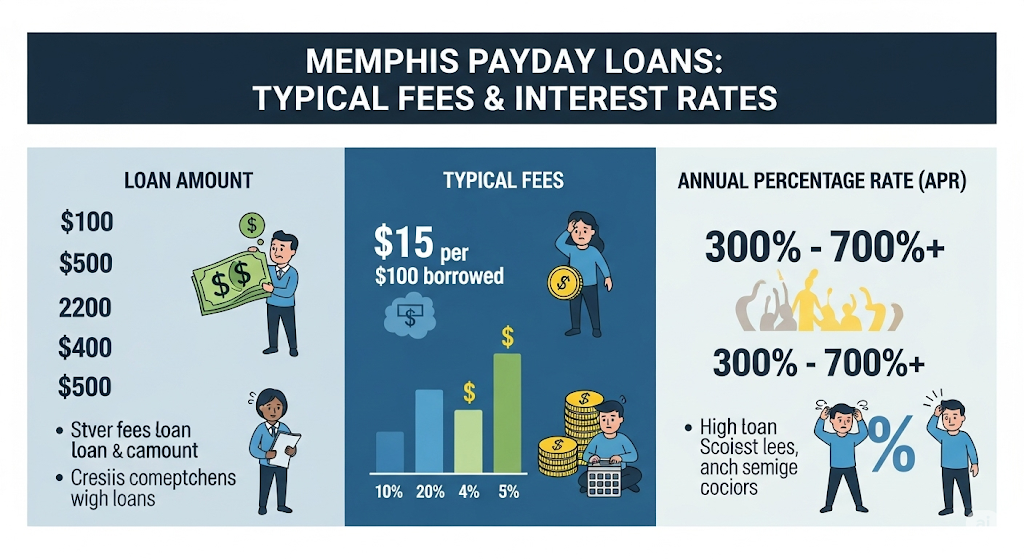

The appeal lies in the ease of access. Most lenders require only proof of income, a valid ID, and an active checking account. There’s no hard credit check, making them accessible to people with poor or no credit history. But this simplicity comes at a cost: Tennessee law allows lenders to charge up to $15 for every $100 borrowed, translating to an annual percentage rate (APR) well over 400% if the loan is rolled over or extended.

In Memphis, borrowers can have only one outstanding payday loan at a time, with a maximum principal amount of $500. While this limit is intended to prevent debt overload, the short repayment window means that many borrowers still struggle to repay on time, often leading to additional fees or refinancing.

State Laws Governing Payday Loans in Memphis

Tennessee payday loans are regulated by the Department of Financial Institutions, which enforces strict licensing requirements for lenders. Under state law:

- Maximum loan amount: $500

- Maximum loan term: 31 days

- Maximum fee: $15 per $100 borrowed

- Rollovers: Not allowed (you must repay in full before taking another loan)

These rules aim to prevent borrowers from falling into a continuous cycle of debt. However, the high cost of borrowing means payday loans should still be considered a last resort. Borrowers in Memphis should always verify that their lender is licensed by the state, as unlicensed or out-of-state lenders may operate illegally and charge excessive fees.

Tennessee also requires lenders to provide clear disclosures about the total cost of the loan, including the APR and repayment terms. This transparency helps borrowers understand exactly what they’re signing up for before committing.

Eligibility Requirements for Payday Loans in Memphis, TN

Applying for a payday loan in Memphis is intentionally designed to be simple and fast, catering to those who need cash urgently. Unlike traditional bank loans, where lengthy applications and credit checks are the norm, payday loans require minimal documentation. At a minimum, you’ll need to present proof of a steady income—this could be a pay stub, a benefits statement, or any verifiable source of recurring funds. You must also provide a valid government-issued ID to confirm your identity, and an active checking account where funds can be deposited and withdrawals made.

Tennessee law requires borrowers to be at least 18 years old. While there is no specific minimum income threshold, lenders assess whether your income is sufficient to cover repayment after your regular expenses. This flexibility makes payday loans accessible to a wide range of people, including part-time workers, retirees, and those with less-than-perfect credit. However, accessibility does not equal affordability. Meeting eligibility criteria simply means you can get the loan—it doesn’t mean it’s the best financial choice for you.

How Much You Can Borrow and Repay in Memphis

In Memphis, payday loans are capped at $500 per borrower, as stipulated by Tennessee state law. This limit is designed to prevent borrowers from taking on unmanageable levels of short-term debt. While $500 may not sound like much, the quick repayment cycle—typically 14 to 31 days—can make repayment challenging if you’re already stretched thin financially.

Let’s break down the math: If you borrow $300 with the maximum allowable fee of $15 per $100, you’ll owe $345 on your next payday. For someone living paycheck to paycheck, that extra $45 can be significant. The law also prohibits partial rollovers, meaning you must pay the full amount due before taking another loan. While this rule is meant to protect consumers, it can lead to a dangerous cycle where borrowers repay one loan only to take out another soon after.

Some borrowers attempt to bypass these limits by seeking loans from multiple lenders, but the state’s database system prevents simultaneous payday loans. This safeguard helps reduce the risk of overwhelming debt, though it doesn’t eliminate the financial pressure entirely.

Typical Fees and Interest Rates for Memphis Payday Loans

The cost of payday loans in Memphis is steep, even within the legal framework set by Tennessee. Lenders can charge up to $15 per $100 borrowed, which translates to an annual percentage rate (APR) exceeding 400% when calculated over a year. This high cost is one of the main criticisms of payday lending, as it can trap borrowers in a cycle of debt if they are unable to repay promptly.

For example, a $500 payday loan at the maximum fee would carry a $75 charge, making the total repayment amount $575. While that fee may seem reasonable for short-term access to funds, the APR calculation reflects the true cost when viewed over time. Borrowers should also be aware of potential additional charges, such as late fees or returned payment fees if there are insufficient funds in the bank account on the due date.

Because these costs are fixed by state law, shopping around won’t change the basic fee structure much, but some lenders may offer promotional discounts for new customers or repeat borrowers. That said, the primary way to keep payday loan costs down is to borrow only what you need and repay it in full on time.

The Fastest Ways to Get a Payday Loan in Memphis

When time is critical, payday loans in Memphis can be processed within hours—sometimes even minutes. The fastest method depends largely on the lender and your preferred application channel. Storefront payday lenders often provide same-day cash after you complete a brief application and provide the required documents. Many of these locations are strategically placed in high-traffic areas for maximum convenience.

Online payday lenders serving Memphis offer speed and flexibility, allowing you to apply from home and often receive funds via direct deposit within 24 hours. Some fintech lenders even offer instant funding to eligible debit cards. While online applications eliminate the need for travel, they still require verification of your income and identity before approval.

The quickest approvals generally go to repeat customers with the lender, as their information is already on file. However, speed should never outweigh due diligence—ensure you’re dealing with a licensed Tennessee lender, whether in-person or online, to avoid scams and illegal terms.

Online Payday Loans vs. Storefront Payday Loans in Memphis

Both online and storefront payday loans serve the same purpose: providing fast, short-term cash. However, each comes with its own advantages and drawbacks. Storefront lenders in Memphis offer face-to-face service, immediate cash disbursement, and the ability to ask questions in person. This can be reassuring, especially for first-time borrowers.

Online payday loans, on the other hand, offer unmatched convenience. You can apply 24/7 without leaving your home, and many lenders use electronic document verification to speed up the process. Funds are typically deposited into your bank account by the next business day, making this option ideal for those with busy schedules or transportation challenges.

Fees and repayment terms are largely the same due to Tennessee law, so the choice between online and in-person often comes down to personal preference and urgency. However, borrowers should be especially cautious with online lenders, verifying their license and ensuring they operate within Tennessee regulations to avoid predatory practices.

The Pros and Cons of Payday Loans for Memphis Residents

For many Memphis residents, payday loans offer an attractive solution to short-term cash flow issues. The biggest advantage is speed—funds are often available within the same day, allowing borrowers to address urgent expenses without waiting for their next paycheck. Additionally, the minimal requirements and absence of a traditional credit check make payday loans accessible to a broad segment of the population, including those with poor or no credit history. This accessibility is especially valuable in emergency situations when time and creditworthiness are critical factors.

However, the downsides are significant. The high cost of borrowing—often translating to APRs above 400%—means payday loans are one of the most expensive forms of credit available. In Memphis, state law limits loan amounts to $500 and terms to a maximum of 31 days, but these restrictions don’t necessarily prevent borrowers from falling into a debt cycle. The short repayment period can make it difficult to pay off the loan without reborrowing, and since rollovers are prohibited, many borrowers simply take out another loan after repaying the first, perpetuating the cycle.

For those considering payday loans, the decision should be made with full awareness of both the benefits and the risks. While they can be a financial lifeline in emergencies, they are best used sparingly and repaid as quickly as possible to avoid escalating costs.

Common Reasons People Use Payday Loans in Memphis

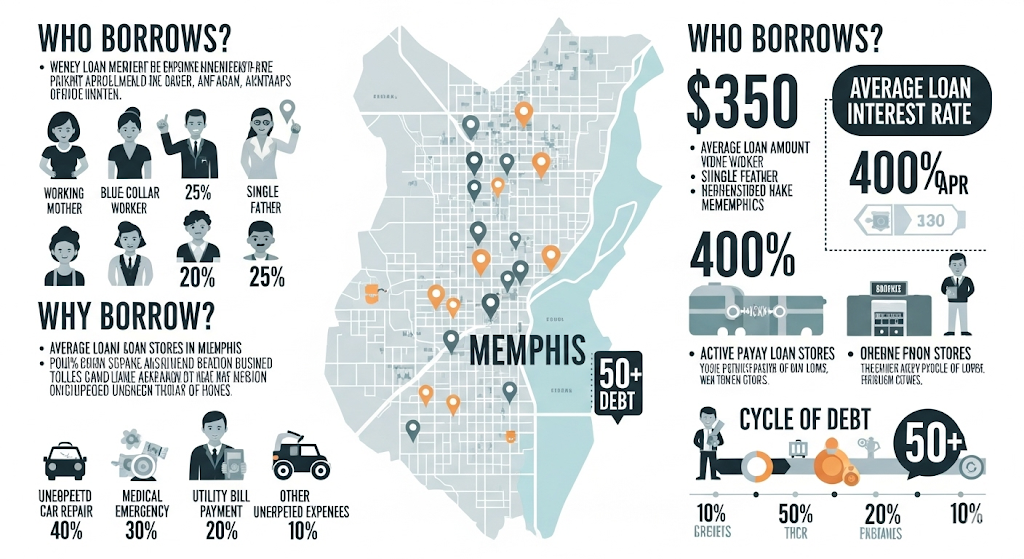

Memphis residents turn to payday loans for a variety of reasons, most of which revolve around urgent, unexpected expenses. One of the most common is covering essential bills—such as rent, utilities, or medical costs—when income falls short. For many households, even a small, unexpected expense can create financial strain, and payday loans provide a fast solution.

Another frequent reason is vehicle repairs. Memphis is a city where public transportation options are limited compared to larger metropolitan areas, making car ownership a necessity for most residents. When a vehicle breaks down, the cost of repairs can be high, and without immediate cash, people risk losing their primary mode of transportation. Payday loans offer a way to cover those costs quickly, ensuring that work and other commitments aren’t disrupted.

Additionally, some borrowers use payday loans to avoid late payment fees on bills, which can lead to higher costs or service disconnections. While using a payday loan to avoid a utility shutoff or eviction can make sense in the short term, it’s important to remember that the high repayment costs may create challenges in the following pay cycle.

Risks of Defaulting on a Payday Loan in Tennessee

Defaulting on a payday loan in Memphis can have serious consequences. If you fail to repay the loan on time, the lender will attempt to cash your post-dated check or process an electronic withdrawal from your account. If there are insufficient funds, you’ll incur bank overdraft fees in addition to any late fees charged by the lender.

Beyond immediate financial penalties, defaulting can result in collection actions. While Tennessee law prohibits lenders from threatening criminal prosecution over unpaid loans, they can take civil action to recover the debt. This can lead to wage garnishment or liens if a court judgment is obtained. Additionally, while payday lenders typically do not report loans to credit bureaus, unpaid debts that are sent to collections can appear on your credit report and remain there for up to seven years.

The impact of default goes beyond financial consequences—it can also create significant stress and strain on personal relationships. That’s why it’s critical to borrow only what you can repay and to contact your lender immediately if you anticipate difficulty making your payment.

Payday Loan Statistics in Memphis: Who Borrows and Why

While specific Memphis-only payday loan statistics can be difficult to find, statewide data offers valuable insight. According to the Tennessee Department of Financial Institutions, tens of thousands of payday loans are issued annually across the state, with a significant portion concentrated in urban centers like Memphis.

Demographically, payday loan borrowers tend to have lower incomes, with many earning less than $40,000 annually. They are often employed in service or retail jobs with irregular hours and limited benefits, making them more vulnerable to income disruptions. The average loan amount in Tennessee hovers near the legal cap of $500, and most borrowers take out multiple loans over the course of a year, despite laws aimed at limiting concurrent borrowing.

The data also reveals a troubling pattern: many borrowers use payday loans repeatedly to cover ongoing expenses rather than true emergencies. This suggests that payday loans in Memphis are often filling a gap left by insufficient wages, lack of savings, and limited access to affordable credit alternatives.

Alternatives to Payday Loans in Memphis, TN

For residents looking to avoid the high costs of payday loans, several alternatives exist in Memphis. Credit unions often offer payday alternative loans (PALs), which allow members to borrow small amounts at significantly lower interest rates, with repayment terms extending up to six months. These loans are designed to be a safer, more affordable option for short-term borrowing.

Another option is personal installment loans from community banks or online lenders. While approval requirements may be stricter, these loans offer lower APRs and longer repayment periods, reducing the pressure on your next paycheck. Some employers in Memphis also offer paycheck advances or earned wage access programs, allowing employees to access a portion of their earned wages before the regular payday without incurring high fees.

For those facing utility shutoffs or eviction, local nonprofits and churches may provide emergency financial assistance. While these resources may not be as fast as payday loans, they can prevent the need to take on expensive debt.

How to Spot and Avoid Payday Loan Scams in Memphis

Memphis has its share of legitimate, licensed payday lenders, but scammers also target vulnerable borrowers. One red flag is a lender who does not have a Tennessee license—state law requires all payday lenders to be registered. Be wary of lenders who demand upfront fees before providing the loan, or who pressure you to act immediately without giving time to review the terms.

Another sign of a scam is refusal to provide written loan agreements or disclosure of the APR and fees. In Memphis, all licensed lenders must clearly outline the total repayment cost. Stick to well-known, state-regulated companies and verify licenses through the Tennessee Department of Financial Institutions.

Payday Loan Impact on Your Credit Score in Memphis

Payday loans in Memphis generally don’t affect your credit score—unless you default. Lenders typically don’t report timely payments to credit bureaus, so repaying on time won’t boost your score. However, if your loan goes unpaid and is sent to collections, it can appear on your credit report and damage your score for years.

This limited credit impact makes payday loans appealing to those with poor credit, but it also means they won’t help you build credit. If your goal is to improve your credit score, consider secured credit cards or small personal loans from credit unions as safer options.

Military Borrowers and Payday Loans: Special Rules in Memphis

Active-duty service members in Memphis are protected by the federal Military Lending Act (MLA), which caps the APR on payday loans at 36% and prohibits certain predatory practices. This law applies to both the service member and their dependents. Lenders must also provide clear disclosures and cannot require access to a military paycheck as loan collateral.

If you’re in the military, always confirm the lender understands and complies with MLA protections—violations can lead to the loan being voided. Many military financial assistance programs offer lower-cost alternatives, making payday loans rarely the best choice for service members.

Tips for Borrowing Responsibly in Memphis’s Payday Loan Market

If you must take a payday loan, borrow only what you absolutely need and create a repayment plan before accepting the funds. Avoid taking back-to-back loans, as this can trap you in a cycle of debt. Pay the loan off on time to minimize fees and protect your bank account from overdraft charges.

Also, keep an emergency fund—even a small one—to reduce future reliance on payday loans. Regularly review your budget to identify areas where expenses can be cut, freeing up cash for savings and emergencies.

The Growing Trend of Online Lending in Memphis

Online payday lending is rapidly gaining popularity in Memphis due to its convenience and speed. Borrowers can apply anytime, receive instant decisions, and often get funds within a day. However, this growth has also brought more unlicensed operators into the market.

To stay safe, always verify that an online lender is licensed in Tennessee. Read reviews, check for secure website connections (HTTPS), and confirm all fees and terms before committing.

The Future of Payday Lending in Memphis, TN

The payday lending industry in Memphis may face changes as lawmakers consider stronger consumer protections. Trends indicate increased adoption of digital lending platforms and potential regulations that could cap fees further or extend repayment periods.

Borrowers should stay informed about these changes, as they could make loans safer and more affordable—or restrict access entirely.

Conclusion: Making Smarter Short-Term Borrowing Decisions in Memphis

Payday loans in Memphis can provide quick relief in emergencies but come with high costs and risks. By understanding Tennessee’s regulations, knowing your alternatives, and borrowing responsibly, you can avoid the debt trap many fall into.

The smartest approach is to view payday loans as a last resort. Build a financial cushion, explore lower-cost credit options, and if you must borrow, repay as quickly as possible. Financial stability comes not from quick fixes, but from consistent, informed decision-making.

FAQ : payday loans memphis tn

1. Are payday loans legal in Memphis, TN?

Yes, payday loans are legal in Memphis under Tennessee law. Lenders must be licensed by the Tennessee Department of Financial Institutions and follow state limits—maximum $500 loan amount, up to 31 days term, and a fee cap of $15 per $100 borrowed.

2. What is the maximum payday loan amount in Memphis?

In Memphis, the maximum payday loan you can borrow is $500. This limit is set by state law to help prevent borrowers from accumulating unmanageable debt. You can only have one active payday loan at a time in Tennessee.

3. How quickly can I get a payday loan in Memphis?

Many Memphis lenders offer same-day funding for in-store applications. Online payday loans often deposit funds within 24 hours after approval. Speed depends on your bank, the lender’s processing times, and how quickly you submit required documents.

4. Do payday loans in Memphis require a credit check?

No, most payday lenders in Memphis do not perform hard credit checks. Instead, they verify your income, ID, and bank account. This makes them accessible to borrowers with poor or no credit history, though it also means higher fees due to increased lending risk.

5. What happens if I can’t repay a payday loan in Memphis?

If you can’t repay, the lender may attempt to cash your post-dated check or withdraw funds electronically. This can lead to overdraft fees, late charges, and potential collection actions. While criminal prosecution is prohibited, unpaid loans sent to collections can harm your credit.

6. Can I renew or roll over a payday loan in Memphis?

No, Tennessee law prohibits rollovers on payday loans. You must repay your loan in full before taking another. This rule is intended to reduce the debt cycle but can still leave borrowers vulnerable if they reborrow immediately after repayment.

7. Are online payday loans available to Memphis residents?

Yes, many licensed Tennessee lenders offer online payday loans to Memphis residents. However, you must ensure the lender is licensed in Tennessee to avoid scams or illegal terms. Always verify licensing through the Tennessee Department of Financial Institutions.

8. Do payday loans affect my credit score in Memphis?

Payday loans typically don’t affect your credit score unless you default. If unpaid, the debt may be sent to collections, and that account can appear on your credit report for up to seven years, damaging your score significantly.

9. What alternatives to payday loans exist in Memphis?

Alternatives include payday alternative loans (PALs) from credit unions, personal installment loans, paycheck advances from employers, and assistance from nonprofits. These options often have lower interest rates, longer repayment terms, and fewer risks than payday loans.

10. How do I check if a Memphis payday lender is licensed?

You can confirm a lender’s license by visiting the Tennessee Department of Financial Institutions’ website and searching their database. Licensed lenders must follow all state laws on loan limits, terms, and fees, providing greater borrower protection.