Introduction — Why Payday Loans Are a Hot Topic in Sacramento

Sacramento, the capital of California, is a fast-growing city where the cost of living has steadily risen over the past decade. From unexpected car repairs to urgent medical bills, many residents face financial emergencies between paychecks. Payday loans in Sacramento offer a quick fix — but they also come with significant costs and risks.

This comprehensive guide covers everything you need to know about payday loans in Sacramento, California — including state laws, costs, alternatives, and tips to borrow responsibly. Whether you’re considering a storefront lender on Florin Road or applying online from your apartment in Midtown, the insights here will help you make an informed decision.

Understanding Payday Loans in Sacramento

A payday loan is a small, short-term loan, typically between $100 and $300, that’s meant to be repaid on your next payday. In California, the maximum payday loan amount is $300, and state law caps the fee at $45 for that amount. This translates to an annual percentage rate (APR) of over 400%, making them one of the most expensive forms of credit available.

In Sacramento, payday lenders operate both storefronts — often in busy commercial corridors like Arden Way or Mack Road — and online platforms that serve all California residents. The process is straightforward: you write a post-dated check or authorize an electronic debit for the loan amount plus fees, due on your next payday.

California Payday Loan Laws — What Sacramento Borrowers Need to Know

The payday loan industry in Sacramento is regulated under the California Deferred Deposit Transaction Law. Key rules include:

- Maximum loan amount: $300

- Maximum fee: 15% of the loan amount (e.g., $45 for $300)

- Term length: No more than 31 days

- Rollovers prohibited: You cannot extend or “roll over” a payday loan by paying only the fee

- Licensing: Lenders must be licensed by the California Department of Financial Protection and Innovation (DFPI)

These rules are designed to prevent debt traps, but the short repayment period and high cost still make payday loans risky for many Sacramento residents.

Who Uses Payday Loans in Sacramento?

Sacramento payday loan customers come from diverse backgrounds, but certain groups are more likely to use these loans:

- Service industry workers in hospitality, food service, and retail

- Gig economy workers like Uber drivers and DoorDash couriers

- Low-income households with limited or no savings

- Renters facing sudden rent increases or utility shutoff notices

According to DFPI data, over 1.6 million payday loans were issued in California in a recent year, with Sacramento County representing a significant share. Many borrowers report using payday loans to cover recurring expenses, not just emergencies — a sign of deeper financial instability.

Online Payday Loans vs. Storefront Lenders in Sacramento

Online Lenders:

- Pros: Apply anytime, convenient for those without transportation, quick approvals

- Cons: Higher risk of encountering unlicensed lenders, potential for hidden fees

Storefront Lenders:

- Pros: Face-to-face service, immediate cash payout, clear display of fees

- Cons: Limited hours, travel required, potential embarrassment of in-person borrowing

For Sacramento borrowers, the choice often depends on urgency, access to technology, and personal comfort level.

Alternatives to Payday Loans in Sacramento

Before committing to a payday loan, explore these local and statewide alternatives:

- Credit Union Payday Alternative Loans (PALs): Sacramento credit unions like SAFE Credit Union and Golden 1 Credit Union offer small-dollar loans with lower rates and longer repayment terms.

- Utility Payment Plans: SMUD (Sacramento Municipal Utility District) and PG&E have hardship programs and flexible billing options.

- Nonprofit Assistance: Organizations like Sacramento Food Bank & Family Services provide emergency aid for essentials.

- Earned Wage Access Apps: Services like Earnin or DailyPay let you access part of your paycheck early, often with lower costs than payday loans.

How to Spot a Licensed Lender in Sacramento

In Sacramento, every payday lender is required to be licensed by the California Department of Financial Protection and Innovation (DFPI). This licensing process ensures that the lender operates within state laws, adheres to fee limits, and follows consumer protection rules.

Before signing any agreement, you should always check whether the lender’s license number is clearly displayed on their storefront signage or prominently on their website if you’re applying online. Reputable lenders take pride in showing their credentials, as it builds trust with customers.

You can also verify a lender’s status through the DFPI’s official online license database. This public tool allows you to search by business name or license number and confirm whether the lender is authorized to operate in California.

Borrowers should be cautious with any lender that fails to provide a written contract detailing loan terms, fees, and repayment schedules. Unlicensed lenders often try to bypass regulations by omitting key disclosures, charging illegal interest rates, or using aggressive collection tactics. Falling into the hands of such lenders could mean paying excessive fees, facing harassment over repayment, or losing important legal protections.

The Risks of Payday Loans in Sacramento

While payday loans can be a quick solution for an urgent cash need, they come with significant financial risks that every Sacramento borrower should understand. One of the biggest dangers is the debt cycle — many borrowers find themselves taking out a new loan immediately after paying off the old one, just to cover regular expenses.

The high costs are another concern. For example, borrowing $300 in California typically comes with a $45 fee for a two-week term, which equals an annual percentage rate (APR) of over 400%. If you roll the loan over or take out multiple loans, these fees can quickly exceed the original amount you borrowed.

Another drawback is that payday loan repayments generally do not help build your credit score. Lenders do not report on-time payments to the major credit bureaus, so responsible repayment won’t improve your credit history. However, if you default, the loan could be sent to collections — and that will negatively impact your credit profile.

Military Payday Loan Protections in Sacramento

Sacramento has a strong military presence, and many active-duty service members and their families are potential targets for high-cost lending. Thankfully, the Military Lending Act (MLA) provides important safeguards for these borrowers.

Under the MLA, lenders cannot charge an APR higher than 36% on payday loans for active-duty military members and their dependents. This cap includes interest, fees, and any other charges associated with the loan. The Act also prohibits mandatory arbitration clauses, ensuring that military borrowers retain their right to take disputes to court if necessary.

Certain lending practices are outright banned under the MLA, including loan rollovers that could trap borrowers in a cycle of debt. Additionally, military families in Sacramento have access to alternative resources such as Army Emergency Relief or Navy-Marine Corps Relief Society, which provide interest-free or low-interest emergency loans.

These protections are crucial in helping service members maintain financial stability and avoid predatory lending traps while they serve the country.

The Economic Impact on Sacramento

Payday loans have a ripple effect on Sacramento’s economy. Each year, millions of dollars flow out of local communities in the form of fees paid to payday lenders. Since most of these lenders are owned by national or out-of-state corporations, this money leaves Sacramento instead of being reinvested in local businesses.

High-interest debt can also weaken household financial stability, leading to reduced consumer spending in the local economy. Struggling families may cut back on dining out, entertainment, or shopping — all of which impacts small businesses in the area.

Moreover, increased payday loan usage often correlates with higher demand for public assistance programs such as food stamps, utility subsidies, or emergency housing aid. This puts additional strain on Sacramento’s social services and taxpayer-funded resources.

Reducing reliance on payday loans could help retain more wealth within the community, strengthen household budgets, and promote long-term economic growth.

Borrowing Smarter in Sacramento

If you decide that a payday loan is your only option, it’s important to approach borrowing with a clear strategy. First, only borrow the amount you absolutely need — not the maximum you qualify for. This keeps your repayment manageable and reduces the total fees you’ll pay.

Before applying, create a realistic repayment plan. Look at your next paycheck, subtract essential expenses like rent, utilities, and groceries, and see what’s left. If you can’t cover the loan plus fees, it’s a sign that you should consider other solutions.

Avoid taking loans back-to-back, as this is a common path into the debt trap. Once the loan is repaid, focus on building a small emergency savings fund to cover future unexpected expenses.

Remember, a payday loan should be treated as a one-time emergency tool — not a recurring financial habit. The smartest borrowers use them sparingly and prioritize long-term financial health over short-term fixes.

How Much Can You Borrow with a Payday Loan in Sacramento?

In Sacramento — and across California — the maximum payday loan you can take is $300. This limit is set by the California Deferred Deposit Transaction Law and applies to both storefront and online lenders.

While $300 may sound small, the effective cost is high. Borrowing the maximum and paying the maximum fee of $45 results in a repayment amount of $345 due in 14 days. If you can’t repay, you’ll need to take another loan or risk overdraft and collection fees.

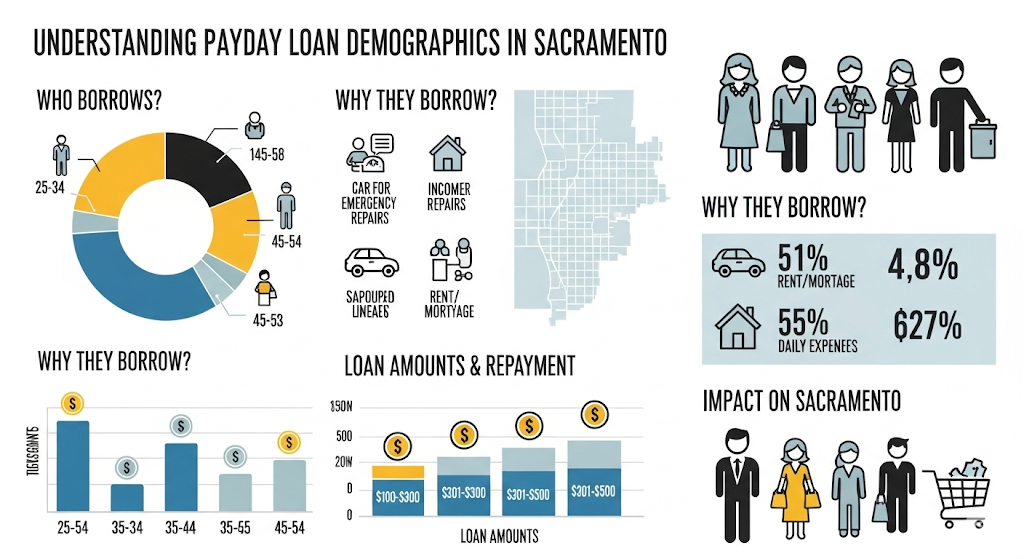

Understanding Sacramento’s Payday Loan Demographics

Payday loan use in Sacramento spans multiple age groups, but research by the California Department of Financial Protection and Innovation (DFPI) reveals some trends:

- Median borrower age: 35–44 years old

- Top employment sectors: Service industry, healthcare support, and retail

- Average number of payday loans per borrower annually: 6–8

- Main loan purpose: Covering recurring expenses like rent, bills, and groceries

This shows payday loans are often not a one-time emergency fix, but part of a recurring financial gap problem.

Comparing Payday Loan Fees Across California Cities

Although payday loan laws are the same statewide, borrowing costs can feel different depending on the local economy.

For example:

| City | Max Loan | Max Fee | Median Household Income | Impact Level* |

|---|---|---|---|---|

| Sacramento | $300 | $45 | $79,100 | High |

| Los Angeles | $300 | $45 | $76,135 | High |

| Fresno | $300 | $45 | $63,780 | Very High |

*Impact Level = How heavily fees affect average local income

This table highlights that while the legal cost is the same, Sacramento borrowers with slightly higher incomes may feel the impact less than lower-income cities — but it still strains budgets.

Payday Loan Scams to Watch Out for in Sacramento

With so much online lending, scams have increased. Sacramento borrowers should watch for:

- Unlicensed lenders claiming “state-approved” status without a license number

- Requests for upfront fees before funding a loan

- Pressure tactics demanding immediate agreement without time to review terms

- Fake collection calls threatening legal action for loans never taken

If you suspect a scam, report it to the DFPI Consumer Services Office or the Federal Trade Commission (FTC).

How Payday Loans Affect Sacramento’s Economy

Every year, payday lenders collect millions in fees from Sacramento borrowers. According to DFPI reports, in a recent year:

- Over 1.6 million payday loans were issued statewide

- Sacramento County ranked among the top 10 counties for payday loan volume

- An estimated $20+ million in fees left the local economy

These numbers reveal a wealth drain effect — money spent on payday loan fees is money not spent on rent, groceries, or local businesses.

The Role of Credit Unions in Sacramento

Many Sacramento credit unions offer Payday Alternative Loans (PALs), which are regulated by the National Credit Union Administration (NCUA). These loans typically have:

- Maximum APR of 28%

- Loan amounts up to $2,000

- Repayment terms of 1–12 months

- Lower fees than payday loans

Institutions like SAFE Credit Union and Golden 1 Credit Union are leading this effort to provide safer, more affordable credit options to Sacramento residents.

The Impact of California’s New Lending Regulations

California has been tightening rules on small-dollar lending. The Fair Access to Credit Act (AB 539), effective January 2020, capped interest rates at 36% APR for loans between $2,500 and $10,000 — but payday loans under $300 remain exempt and can still have APRs over 400%.

This means that while larger installment loans have become significantly more affordable for borrowers in Sacramento, payday loans are still one of the most expensive credit options available. The exemption leaves a major gap in consumer protection for individuals who rely on small-dollar loans for emergencies like car repairs or utility bills.

Many consumer advocacy groups in Sacramento argue that this loophole creates a situation where the most vulnerable borrowers — often those with the smallest loan needs — face the highest relative costs.

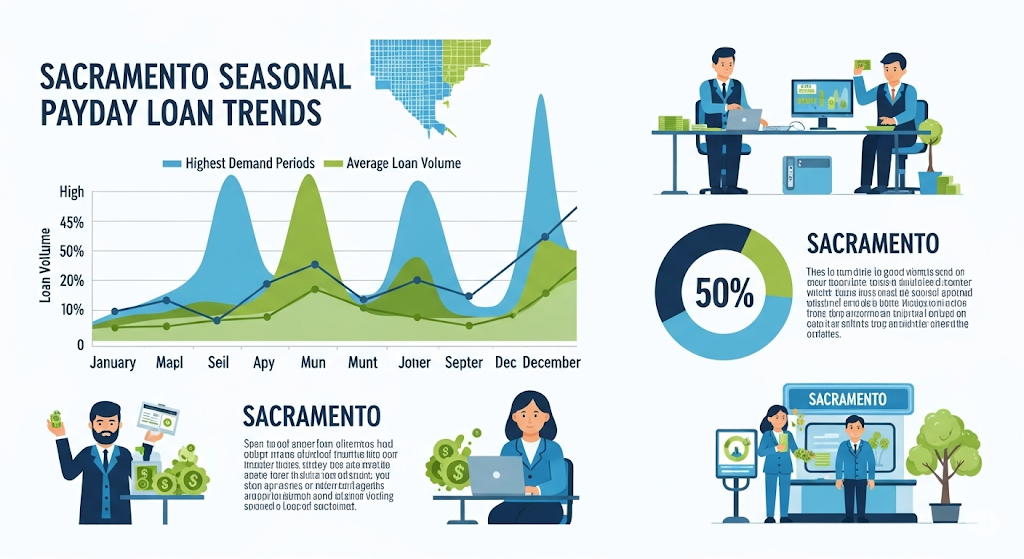

Seasonal Payday Loan Trends in Sacramento

Payday loan demand spikes at certain times of year:

December–January: Holiday shopping debt and high utility bills

This is the most common peak period. Sacramento households often overspend during the holidays, and when credit card bills arrive in January alongside higher winter heating costs, many turn to payday loans to bridge the gap until their next paycheck.

August–September: Back-to-school costs

Parents and students face expenses for tuition, supplies, clothing, and technology. In Sacramento’s public school districts and local colleges, these costs can add up quickly, leading many to seek short-term loans.

April: Tax preparation and payment deadlines

Tax season often brings unexpected bills for those who owe state or federal taxes. While some Sacramento residents receive refunds and have extra cash, others face sudden obligations they cannot meet without borrowing.

Understanding these trends can help policymakers and nonprofits time financial assistance programs for maximum impact. For example, community organizations could schedule financial literacy workshops or offer small-dollar loan alternatives in these months.

The Future of Payday Lending in Sacramento

With the rise of fintech lenders, Sacramento’s payday loan market is changing. Earned wage access services, AI-powered underwriting, and blockchain-based lending platforms could eventually compete with or replace traditional payday loans. These new technologies promise faster processing times, lower fees, and more personalized repayment options — features that could make them more attractive to borrowers who currently rely on high-cost payday loans.

However, until laws change, payday loans will remain a quick — but costly — cash option for many residents. Traditional lenders still hold an advantage in terms of brand recognition and physical presence in Sacramento neighborhoods, especially for customers who prefer face-to-face transactions. In the meantime, borrowers should watch how these emerging tools develop, as they may soon offer a bridge between immediate access to cash and the affordability that payday loans currently lack.

Conclusion — Borrowing Smarter in Sacramento

Payday loans in Sacramento, CA, can be a financial lifeline in urgent situations, but they come at a steep cost. By knowing the laws, recognizing risks, and considering alternatives, you can make smarter borrowing decisions that protect your financial future.

The best strategy is to treat payday loans as an absolute last resort, and to work toward building a small emergency savings buffer for the future.

FAQs About Payday Loans in Sacramento, CA

1. What’s the maximum payday loan in Sacramento?

$300 under California law.

2. How much does a $300 payday loan cost?

Up to $345 due in 14 days, including fees.

3. Are payday loans legal in Sacramento?

Yes, if the lender is licensed by the DFPI.

4. Can I get more than one payday loan at a time?

Yes, but it’s risky and can lead to a debt cycle.

5. Are online payday lenders safe?

Only if licensed in California.

6. Do payday loans build credit?

No, unless you default, which can harm credit.

7. What happens if I don’t repay?

You could face collections, overdraft fees, and legal action.

8. Are there safer alternatives?

Yes, such as credit union PALs, earned wage access apps, and nonprofit aid.

9. Can military members take payday loans?

Yes, but the MLA caps APR at 36%.

10. Where can I report a payday loan scam?

To the DFPI or the FTC.