Understanding Payday Loans in Jacksonville

Payday loans Jacksonville, Florida, are short-term, small-dollar loans designed to cover urgent expenses before your next paycheck. These loans are often marketed as quick cash solutions, but they come with high fees and interest rates that can trap borrowers in cycles of debt.

In Jacksonville, payday loans are regulated under Florida law, which caps fees at $10 per $100 borrowed and limits loan amounts to $500. However, even with these limits, the annual percentage rate (APR) can easily exceed 300%, making them one of the most expensive borrowing options available.

Life Example: Emily, a Jacksonville resident, took out a $300 payday loan to fix her car so she could get to work. While she intended to pay it back in two weeks, unexpected bills caused her to roll the loan over, adding extra fees that quickly made her debt $450.

The Legal Landscape for Payday Lending in Jacksonville

Florida has some borrower protections in place for payday loans, but they’re not as strict as in states that have banned them altogether. The Florida Deferred Presentment Act governs payday loans in Jacksonville, requiring lenders to be licensed and limiting borrowers to one loan at a time.

The law also mandates a 24-hour cooling-off period between loans to prevent continuous borrowing. While this does help reduce immediate re-borrowing, it doesn’t eliminate the risk of long-term debt accumulation.

Data Insight: According to the Florida Office of Financial Regulation, Jacksonville consistently ranks among the top cities in Florida for payday loan usage, with thousands of transactions monthly.

How to Qualify for a Payday Loan in Jacksonville

Eligibility for a payday loan in Jacksonville is generally straightforward: you need a steady income, a valid ID, and an active checking account. Most lenders do not require a credit check, making payday loans accessible to those with poor or no credit history.

However, this easy approval process is part of what makes payday loans risky — many borrowers qualify for loans they cannot realistically afford to repay in two weeks.

Example: Marcus, working part-time at a Jacksonville retail store, was approved for a $400 payday loan in under 30 minutes without a credit check. While this helped cover his rent temporarily, it also left him with a large portion of his next paycheck already spent.

Alternatives to Payday Loans in Jacksonville

If you’re facing a financial emergency, there are better options than payday loans. Jacksonville residents can explore:

- Credit Union Payday Alternative Loans (PALs) – Lower fees and APRs.

- Local nonprofit assistance – Food banks, utility assistance, and emergency grants.

- Employer paycheck advances – Many employers offer short-term salary advances with no interest.

- Small installment loans – Longer repayment terms and lower costs.

Life Example: Sarah avoided taking a payday loan by getting a $200 advance from her employer, which was deducted from her next paycheck without interest.

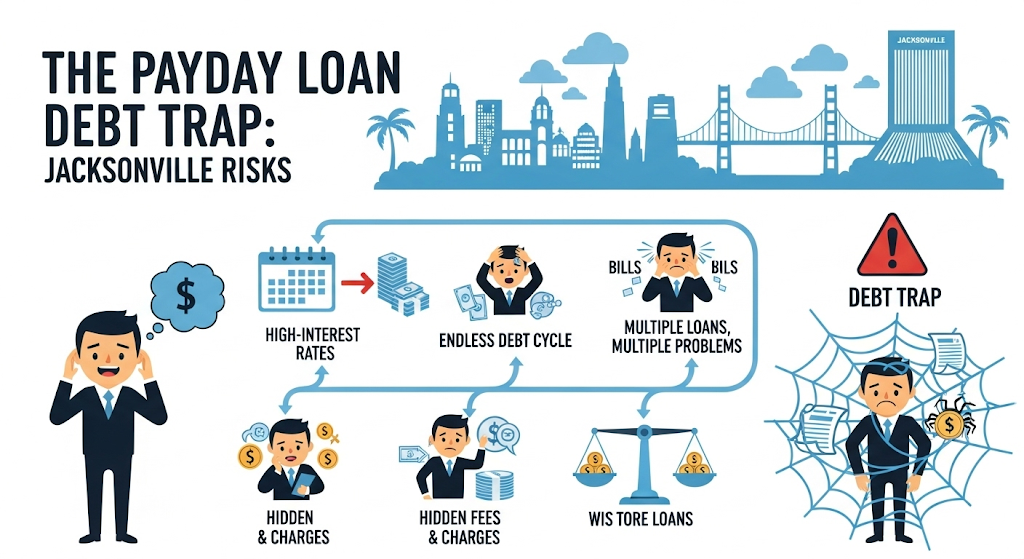

The Risks of Payday Loans in Jacksonville

The biggest risk with payday loans is the cycle of debt they often create. Many borrowers cannot repay the full amount on their next payday and must roll over their loans, incurring additional fees.

This can lead to paying several times the original loan amount in fees alone. Additionally, missed payments can result in aggressive collection tactics, overdraft fees from your bank, and even legal action.

Data Insight: The Consumer Financial Protection Bureau (CFPB) reports that 80% of payday loans are rolled over or followed by another loan within 14 days.

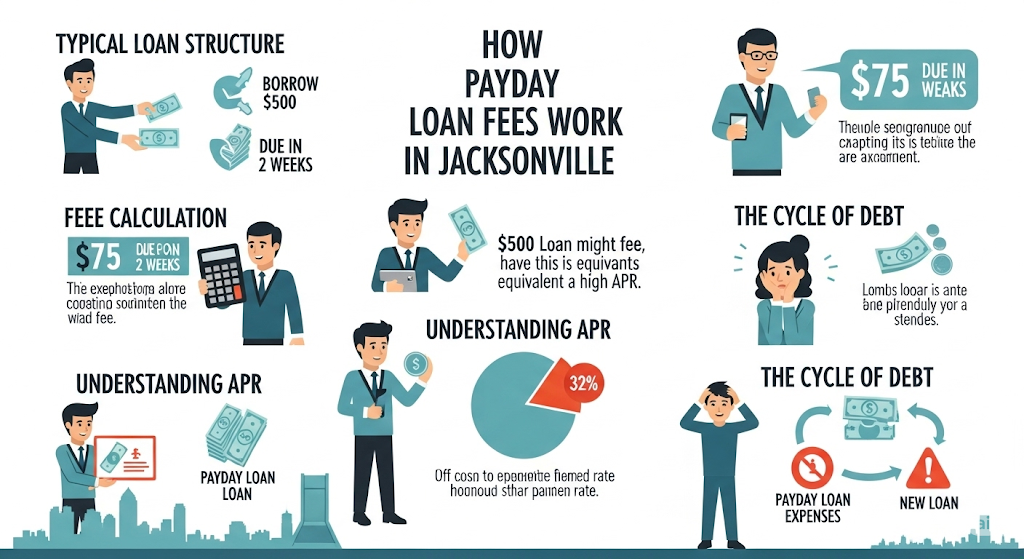

How Payday Loan Fees Work in Jacksonville

Payday loan costs in Jacksonville can be surprisingly high, especially for borrowers unfamiliar with how fees and APRs are calculated. Florida law allows payday lenders to charge up to 10% of the loan amount as a fee, plus a $5 verification fee.

While that might sound modest, the short repayment window makes the annual percentage rate (APR) skyrocket. For example, a $500 loan with a $50 fee due in two weeks has an APR exceeding 260%. Jacksonville resident Carla experienced this firsthand when she borrowed $300 to fix her car’s alternator.

She repaid $335 after just 14 days — and when another expense popped up, she had to borrow again, creating a cycle that took months to escape. Understanding the true cost before signing any agreement is crucial for avoiding long-term debt.

Payday Loan Limits and Borrowing Caps in Jacksonville

Florida law is stricter than some states when it comes to payday loan limits, which directly affects Jacksonville borrowers. The maximum loan amount is $500, and borrowers cannot have more than one active payday loan at a time anywhere in the state.

Additionally, there’s a mandatory 24-hour cooling-off period between paying off one loan and taking out another. This system is meant to prevent borrowers from “stacking” loans, which can lead to financial disaster. Still, even with these protections, lenders in Jacksonville process thousands of loans each year.

One Jacksonville Beach borrower, Michael, found himself waiting for that cooling-off period before reapplying — only to realize it gave him enough time to find a cheaper solution through a local credit union.

Common Reasons People Use Payday Loans in Jacksonville

While emergencies are the most common reason people turn to payday loans, Jacksonville has its own unique financial pressures that contribute to high demand. Many residents work in hospitality, shipping, and seasonal industries, where income can fluctuate.

Rent increases, hurricane preparedness costs, and sudden car repairs are frequent triggers for payday borrowing. For instance, after Hurricane Ian’s outer bands caused flooding in her Riverside neighborhood, Sarah took out a $400 payday loan to replace damaged appliances quickly.

Without it, she would have had to wait weeks for her insurance claim to process. While payday loans can provide immediate relief, they’re often a stopgap rather than a long-term fix.

Payday Loan Storefronts vs. Online Lenders in Jacksonville

Borrowers in Jacksonville have a choice between traditional storefront payday lenders and online payday loan providers. Storefronts offer face-to-face service, immediate cash, and clear visibility of loan terms, while online lenders provide convenience, 24/7 access, and direct bank deposits.

However, online loans can sometimes come from out-of-state companies that don’t follow Florida’s consumer protection laws. John, a Jacksonville construction worker, applied online for a $400 payday loan during a weekend emergency.

The loan was approved instantly, but the lender charged fees beyond Florida’s legal limits, leaving him in a dispute that took weeks to resolve. Choosing a licensed Florida lender — whether online or in person — is the safest approach.

The Impact of Payday Loans on Jacksonville’s Economy

Payday lending in Jacksonville has both immediate and long-term economic effects. In the short term, it injects liquidity into households that need quick cash, allowing them to meet urgent expenses like rent, car repairs, or utility bills. However, the high fees drain millions from the local economy annually.

According to consumer advocates, much of this money flows out to corporate headquarters rather than staying in Jacksonville’s neighborhoods. This loss reduces spending power at local businesses, affecting everything from grocery stores to small service providers.

One Springfield shop owner noted that many of his customers delay purchases when payday loan repayments are due, impacting his weekly revenue. This illustrates how individual borrowing decisions can ripple through the community.

Payday Loan Regulations Unique to Florida and Jacksonville

Florida’s payday lending laws are designed to protect borrowers, and Jacksonville lenders must comply with these regulations. Unlike in some states where payday loans can be rolled over indefinitely, Florida bans rollovers entirely. Instead, if you cannot repay on time, you may qualify for a 60-day grace period — but only if you request it before your due date and agree to attend credit counseling.

This safeguard helps prevent debt spirals, but not all borrowers are aware it exists. Angela, a Jacksonville nurse, found herself unable to repay a $450 loan on time. When she learned about the grace period, she avoided late fees and received budgeting advice that ultimately helped her save money each month. Understanding these local laws can make a significant difference in managing payday debt.

Risks of Taking Multiple Payday Loans in Jacksonville

Even though Florida law prevents borrowers from having more than one active payday loan, some Jacksonville residents still attempt to take additional loans from out-of-state or unlicensed online lenders. This creates a dangerous financial trap.

These loans often come with higher fees, no repayment protections, and aggressive collection tactics. For example, Darnell, a Jacksonville father of three, had a legal in-state loan and then accepted a $300 online payday loan from a Nevada-based company.

When he missed a payment, the out-of-state lender debited his account multiple times, causing overdraft fees and a cascade of bounced bills. This shows why sticking with licensed Florida lenders — and only one loan at a time — is critical for financial stability.

The Role of Payday Loans in Emergency Situations

For many in Jacksonville, payday loans serve as a financial lifeline during emergencies. Whether it’s covering medical expenses, urgent car repairs, or unexpected utility bills, the speed of payday loans can be lifesaving.

Jacksonville’s large commuter population means that vehicle repairs are one of the most common reasons people borrow. In one case, Tony, a rideshare driver from the Southside, needed $400 to replace a transmission sensor immediately or risk losing his income.

While the payday loan came with high fees, it allowed him to get back on the road the same day and keep earning. This highlights the balance borrowers must strike between urgent needs and long-term financial impact.

How Payday Loans Affect Your Bank Account

Payday loans in Jacksonville are almost always repaid through automatic bank withdrawals, which can cause serious issues if the account doesn’t have enough funds. When payments bounce, borrowers face overdraft fees from their bank on top of the lender’s penalties.

According to local financial counselors, many borrowers underestimate the timing of withdrawals, especially when payday falls on a weekend or bank holiday. Jessica, a Jacksonville resident, repaid a $300 loan, but because her paycheck cleared a day late due to a holiday,

The automatic debit triggered two $35 overdraft fees. Understanding your bank’s processing schedule and keeping a cushion in your account can prevent this costly mistake.

Alternatives to Payday Loans in Jacksonville

While payday loans are quick and accessible, Jacksonville residents have other options that may be more affordable. Local credit unions offer Payday Alternative Loans (PALs) with much lower fees. Nonprofits like United Way of Northeast Florida provide short-term assistance for rent, utilities, and food, reducing the need for high-cost borrowing.

In some neighborhoods, community churches also run emergency fund programs. For instance, Marcus from Arlington was able to avoid a payday loan altogether by getting a $250 PAL from his credit union with just a $12 fee, giving him 60 days to repay instead of two weeks. These alternatives not only save money but also reduce the risk of debt cycles.

The Impact of Payday Loans on Credit Health in Jacksonville

In Jacksonville, payday loans rarely help build your credit score because most lenders do not report on-time payments to the major credit bureaus.

However, they can harm your credit significantly if you default. Once a payday loan goes into collections, it can stay on your credit report for up to seven years, making it harder to get affordable financing in the future.

For example, Lisa, a Jacksonville retail worker, repaid several payday loans on time with no change to her credit score. But when she missed one payment that was sold to a collection agency, her score dropped by nearly 80 points in a single month. This underlines the importance of knowing how these loans interact with credit reporting before borrowing.

The Cost of Rolling Over Payday Loans in Jacksonville

Although Florida law bans official rollovers, some borrowers still extend their loans by paying only the fees and re-borrowing the same amount after a short gap.

This is essentially a rollover by another name — and it can be financially devastating. Data from the Florida Office of Financial Regulation shows that the average payday borrower takes out eight loans per year. In Jacksonville, this means hundreds of dollars lost in fees for a loan that never seems to go away.

One borrower, Daniel, paid over $500 in fees in just six months for a $300 loan he kept renewing, which he could have avoided by arranging an installment plan instead.

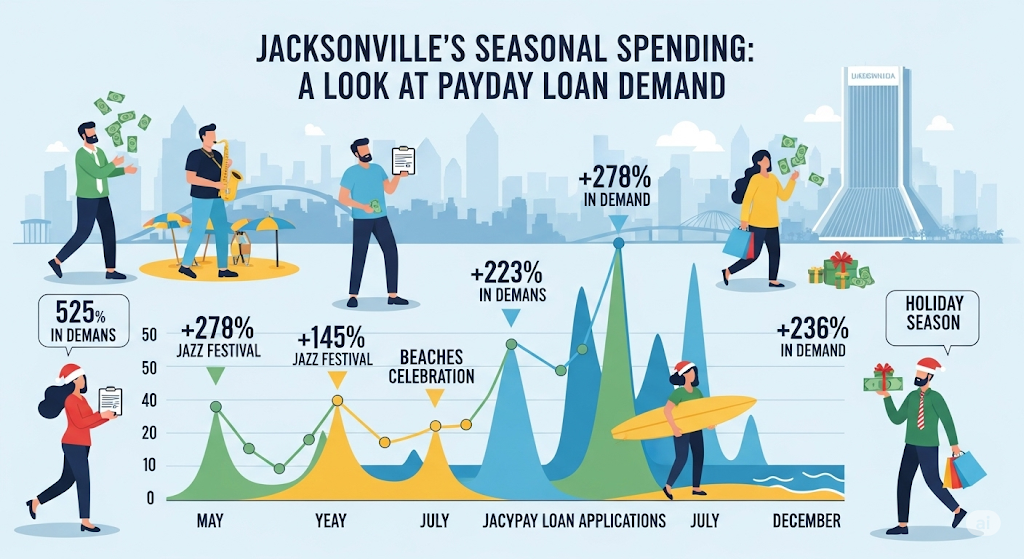

Payday Loan Demand During Seasonal Events in Jacksonville

Seasonal expenses play a major role in payday loan usage patterns across Jacksonville. Demand spikes during the holiday season when gift purchases and high electric bills hit at the same time.

Back-to-school months in August and September also see more borrowers, particularly parents who need extra cash for supplies, clothes, and school fees. Even tax season can bring an uptick in borrowing, as some residents use payday loans to cover their tax payments or preparation costs while waiting for refunds.

Last year, Maria, a Westside resident, took out a payday loan in December for holiday gifts, but ended up in financial trouble when her January utility bills were higher than expected.

How to Spot and Avoid Payday Loan Scams in Jacksonville

Jacksonville residents need to be especially cautious about online payday loan scams. Fraudsters often impersonate legitimate lenders, using professional-looking websites to trick borrowers into providing personal and banking information.

Warning signs include requests for upfront fees, vague or missing contact information, and promises of “guaranteed approval” without any credit or income verification.

In one case, a Jacksonville man lost $150 in “processing fees” to a fake lender that disappeared after collecting his details. Always verify that a lender is licensed through the Florida Office of Financial Regulation before proceeding.

Conclusion – Making Smarter Payday Loan Choices in Jacksonville

Payday loans in Jacksonville can be a quick solution in emergencies, but they come with serious risks if not handled carefully. By understanding Florida’s payday loan laws, knowing the true costs, and being aware of seasonal borrowing trends, residents can make better financial decisions.

Exploring alternatives like credit union PALs, nonprofit assistance, and personal budgeting can help reduce dependency on high-cost short-term loans. The bottom line: payday loans should be a last resort — not the first choice — for Jacksonville borrowers aiming for long-term financial stability.

Frequently Asked Questions – Payday Loans Jacksonville FL

1. Are payday loans legal in Jacksonville, Florida?

Yes. Payday loans are legal in Jacksonville under Florida state law, regulated by the Florida Office of Financial Regulation. Lenders must be licensed, follow a $500 maximum loan limit, and cap terms at 31 days.

2. How much can I borrow from a payday lender in Jacksonville?

Florida law sets the payday loan limit at $500. This includes both the principal amount and any outstanding payday loans you may already have.

3. What is the maximum interest or fee for payday loans in Jacksonville?

The maximum fee allowed is 10% of the loan amount plus a $5 verification fee. While this seems small, the annual percentage rate (APR) can exceed 300% for short-term loans.

4. Can I have more than one payday loan at a time in Jacksonville?

No. Florida’s statewide database prevents borrowers from holding multiple payday loans at once. This system helps reduce over-borrowing and debt cycles.

5. How soon do I have to repay a payday loan in Jacksonville?

Repayment is due on your next payday or within 31 days, whichever comes first. Most loans are structured for a single payment rather than installments.

6. What happens if I can’t repay my payday loan in Jacksonville?

If you can’t repay, you may request a 60-day grace period under Florida law — but only if you contact the lender before the due date and agree to credit counseling.

7. Are there alternatives to payday loans in Jacksonville?

Yes. Alternatives include Credit Union Payday Alternative Loans (PALs), installment loans, nonprofit financial assistance programs, and personal loans from banks.

8. Can payday loans in Jacksonville affect my credit score?

Most lenders don’t report on-time payments to credit bureaus, so they won’t help build credit. However, unpaid loans sent to collections can harm your score.

9. How do I verify if a payday lender in Jacksonville is licensed?

You can confirm a lender’s license through the Florida Office of Financial Regulation’s public license search tool, available online.

10. Is there a cooling-off period between payday loans in Jacksonville?

Yes. Florida law requires a 24-hour cooling-off period between payday loans. This prevents back-to-back borrowing without a short break.