What Is a Balance Transfer in Credit Cards? Explained Simply

If you’re struggling with credit card debt and high-interest rates, you’ve probably come across the term balance transfer. But what exactly does it mean—and how can it help?

A balance transfer is a credit card feature that allows you to move your existing debt from one credit card to another—usually to take advantage of a lower interest rate. This can save you hundreds or even thousands in interest if used correctly.

In 2025, many credit card issuers offer 0% APR balance transfer offers for 12–21 months. These can be a powerful tool for getting out of debt faster, but they also come with fees, fine print, and risks if mismanaged.

In this guide, we’ll walk you through:

- What a balance transfer is (and isn’t)

- How it works step-by-step

- Pros and cons

- Common fees and mistakes

- Who should (and shouldn’t) use one

- The best strategies to maximize savings

Let’s break it down so you can make a smart, informed decision.

Chapter 1: What Is a Balance Transfer? (300–400 words)

1.1 Definition

A balance transfer is when you move an existing balance (debt) from one credit card to another card—usually one with a lower interest rate. The goal is to save money on interest and pay down debt faster.

1.2 Example

Let’s say you owe $5,000 on a credit card with a 22% APR. You apply for a new card offering:

- 0% APR for 18 months on balance transfers

- 3% balance transfer fee

You move the $5,000 to the new card, pay a $150 fee (3%), and now you have 18 months to pay off the balance interest-free.

1.3 What Can Be Transferred?

You can usually transfer:

- Credit card balances

- Some personal loan balances

- Store card debt

Transfers between cards from the same issuer (e.g., Chase → Chase) are not allowed.

Chapter 2: How Does a Balance Transfer Work? (Step-by-Step) (400–500 words)

Here’s how the process usually works:

✅ Step 1: Apply for a Balance Transfer Credit Card

Look for:

- 0% APR for 12–21 months

- Low transfer fee (3% or less)

- No annual fee if possible

Popular options in 2025 include cards from Chase, Citi, Discover, and Bank of America.

✅ Step 2: Request the Balance Transfer

Once approved, you can:

- Provide the account number and amount of the debt you want to transfer

- Transfers are often requested during the application or from the card dashboard

✅ Step 3: Wait for the Transfer to Complete

- Transfers typically take 5–10 business days

- Your old card won’t close automatically—you must pay it off or close it manually

✅ Step 4: Pay Off the Transferred Balance

- Pay it down within the 0% intro period

- Set up autopay or reminders

✅ Step 5: Avoid New Purchases

New purchases may not be covered by the 0% APR. If you don’t pay them off monthly, you’ll accrue interest again.

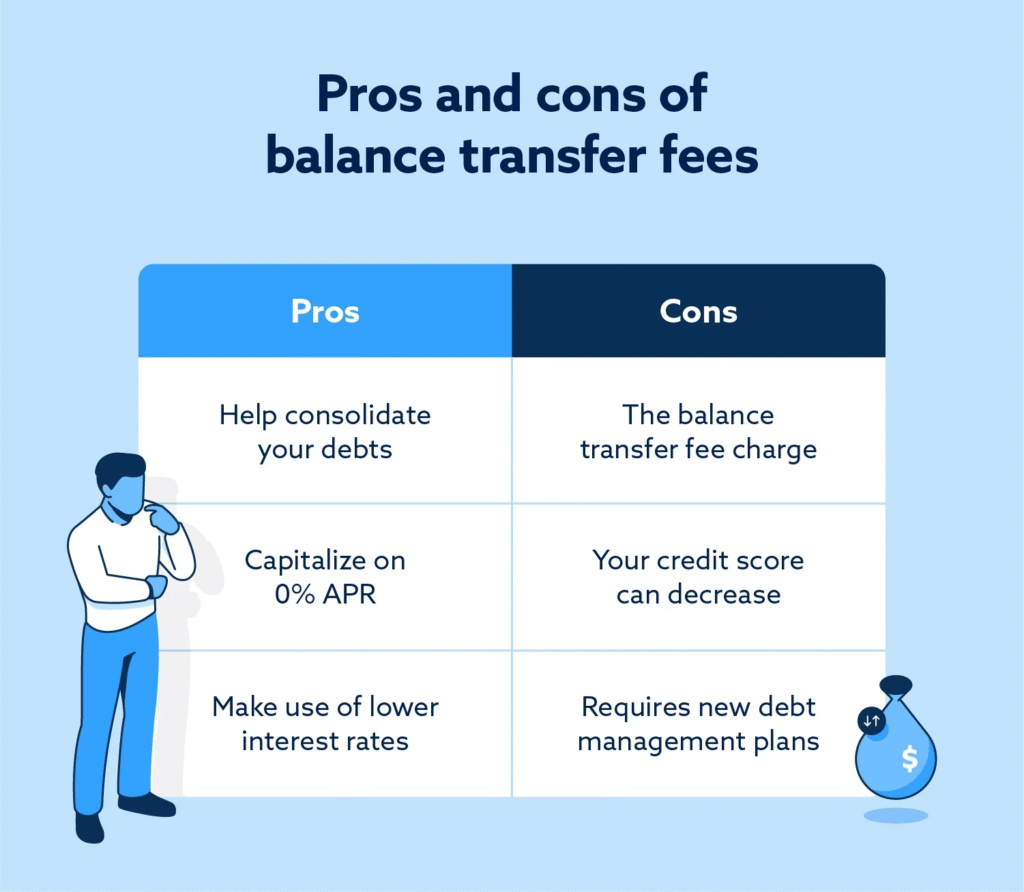

Chapter 3: Pros of Balance Transfers (400–500 words)

✅ 3.1 Save Money on Interest

At 22% APR, $5,000 in debt costs about $1,100 per year in interest. A 0% APR balance transfer can save you that money and let you pay the principal faster.

✅ 3.2 Consolidate Debt

If you’re juggling multiple cards, a balance transfer can help:

- Combine debts into one payment

- Reduce mental load

- Stay organized

✅ 3.3 Pay Off Debt Faster

With no interest, every dollar goes toward your principal, making it easier to:

- Stick to a budget

- Create a debt payoff plan

- Achieve financial freedom faster

✅ 3.4 Improve Credit Utilization

By reducing balances on high-interest cards, you can improve your credit utilization ratio, which boosts your credit score.

Chapter 4: Cons and Risks of Balance Transfers (400–500 words)

❌ 4.1 Balance Transfer Fees

Most cards charge a 3%–5% fee on the amount transferred.

- $5,000 transfer at 3% = $150 upfront

- Some cards have no fee, but shorter 0% terms

❌ 4.2 Temporary Relief

Once the promo ends, the standard APR kicks in—often 18%–29%. If you don’t pay off the full balance, you could be back where you started.

❌ 4.3 New Purchases May Incur Interest

Intro APR often applies only to transferred balances, not new charges. If you make new purchases and don’t pay them off, they’ll accrue interest immediately.

❌ 4.4 Can Hurt Your Credit Score (Short-Term)

- Applying triggers a hard inquiry

- Opening a new account lowers your average credit age

- Closing old accounts (if you do) may affect your score

❌ 4.5 Mismanagement = More Debt

If you don’t make a solid repayment plan, you might:

- Fail to pay off the balance

- Start using the old card again

- Accumulate more debt across two cards

Chapter 5: Who Should Consider a Balance Transfer? (300–400 words)

A balance transfer makes sense if:

✅ You have high-interest credit card debt

✅ You can qualify for a 0% APR card

✅ You’re confident you can pay off the debt in 12–21 months

✅ You want to consolidate multiple cards into one

✅ You have a plan to avoid using old cards again

Who Should Avoid It?

❌ You have poor credit (below 650)

❌ You can’t pay off the balance within the promo window

❌ You’re prone to overspending

❌ You don’t understand the fine print or hidden fees

Chapter 6: Tips for Using Balance Transfers Wisely (400–500 words)

✅ 6.1 Compare Multiple Cards

Look at:

- Intro APR duration

- Balance transfer fee

- Ongoing APR after the promo

- Credit score requirements

✅ 6.2 Use a Debt Payoff Strategy

Try methods like:

- Debt snowball (smallest debt first)

- Debt avalanche (highest interest first)

- Pay fixed amounts monthly to hit your goal before promo ends

✅ 6.3 Don’t Use the Old Card Again

Temptation is real. To avoid digging a deeper hole:

- Freeze the card (literally or digitally)

- Pay it off and close it—only if it won’t hurt your credit score too much

✅ 6.4 Read the Fine Print

Look for:

- When the promo APR starts and ends

- What triggers loss of 0% (e.g., late payments)

- Whether purchases are included or excluded

✅ 6.5 Automate Your Payments

Set up autopay for at least the minimum due. A missed payment:

- Ends your 0% APR

- Triggers penalty APR

- Lowers your credit score

Chapter 7: FAQs About Balance Transfers (300–400 words)

1. Is a balance transfer bad for my credit?

It can cause a small temporary dip, but paying off debt can improve your score in the long term.

2. How long does a balance transfer take?

Usually 5–10 business days, depending on the banks involved.

3. Can I transfer more than my credit limit?

No. You can only transfer up to your available credit—often less than your total limit.

4. What happens if I don’t pay it off in time?

You’ll be charged the regular APR on the remaining balance after the intro period.

5. Can I transfer multiple balances?

Yes—if your credit limit allows it. Consolidating balances can help streamline your payoff plan.

Conclusion: Is a Balance Transfer Right for You?

A balance transfer can be a smart, strategic move—or a slippery slope. It all depends on how you use it.

It’s a great fit if you:

- Have high-interest debt

- Qualify for a good 0% APR offer

- Have a clear plan to pay it off

- Avoid running up new debt

But it’s risky if you:

- Rely on it without budgeting

- Ignore fees and timelines

- Use it as a temporary Band-Aid

Used wisely, a balance transfer card can save you hundreds in interest, speed up your debt-free journey, and even improve your credit score.

✅ Key Takeaways:

- A balance transfer helps you move high-interest debt to a lower-rate card

- Most cards offer 0% APR for 12–21 months with a 3%–5% fee

- Success depends on discipline, planning, and avoiding new debt

- Not all cards—or consumers—are eligible

- Used strategically, it’s one of the most effective ways to escape credit card debt