What Is a Hard Money Loan

In the fast-paced world of real estate investing, time is money. Traditional bank loans often involve a long approval process, strict requirements, and rigid terms that don’t suit every investor’s needs. That’s where hard money loans come in.

Hard money loans are a type of asset-based financing used primarily in real estate. They’re fast, flexible, and ideal for short-term projects—but they come at a cost.

This comprehensive 3,000-word guide will walk you through everything you need to know: what a hard money loan is, how it works, who it’s for, its pros and cons, how to qualify, and smart tips for using them responsibly.

Chapter 1: What Is a Hard Money Loan?

1.1 Definition

A hard money loan is a short-term loan secured by real estate, typically issued by private lenders or investors—not banks. The value of the property (collateral) is more important than the borrower’s creditworthiness.

1.2 Why It’s Called “Hard Money”

The term refers to the loan being backed by a “hard” asset—real estate. Lenders focus on the asset’s value and exit strategy.

Chapter 2: How Hard Money Loans Work

2.1 Loan Structure

- Loan-to-Value (LTV): Typically 60% to 75% of the property’s value

- Term Length: Usually 6 months to 3 years

- Interest Rates: Ranges from 8% to 15%+

- Points: Upfront fees, typically 2–5% of the loan amount

2.2 Repayment Options

- Interest-only payments during the term

- Balloon payment (principal due at end of term)

2.3 Exit Strategies

Lenders want a clear plan for repayment:

- Property sale (fix-and-flip)

- Refinance into a conventional mortgage

- Rental income for long-term hold

Chapter 3: Who Uses Hard Money Loans?

3.1 Real Estate Investors

- Fix-and-flip projects

- Buy-rehab-rent-refinance-repeat (BRRRR) strategies

3.2 Property Developers

- Land purchases and new construction

3.3 Borrowers with Credit Issues

- Poor credit may still be eligible if the property has equity

3.4 Commercial Real Estate Investors

- Bridge financing or quick acquisition of retail, multifamily, or industrial assets

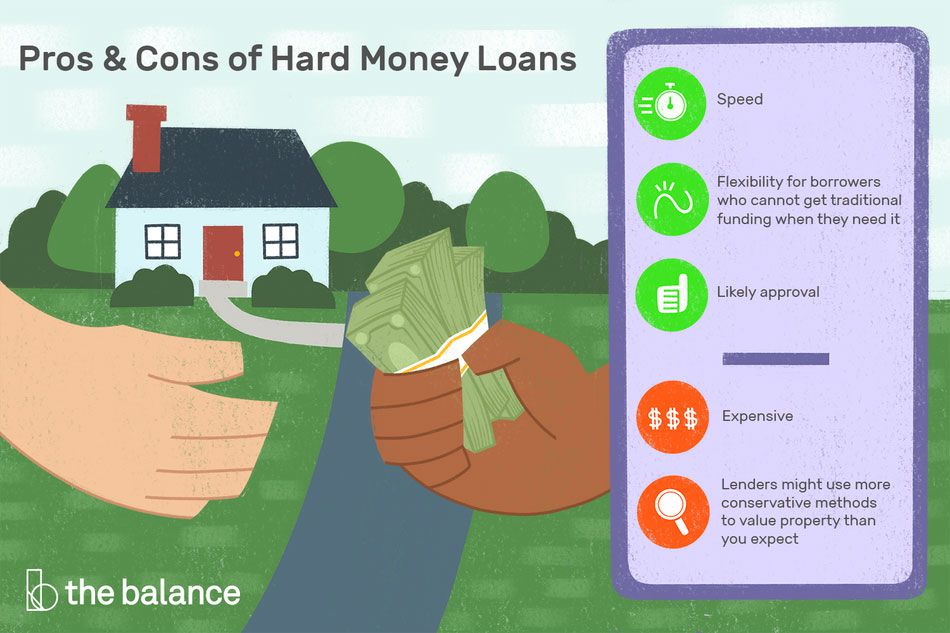

Chapter 4: Pros and Cons of Hard Money Loans

4.1 Pros

- Fast Approval: Funds in days, not weeks

- Flexible Terms: Negotiable structure and conditions

- Credit-Friendly: Based more on collateral than credit score

- Short-Term: Ideal for temporary financing needs

4.2 Cons

- High Interest Rates: Compared to conventional loans

- Short Repayment Terms: Balloon payments can be risky

- Risk of Foreclosure: Asset-based lending means the property can be seized

- Fees and Points: Upfront costs can be substantial

Chapter 5: How to Qualify for a Hard Money Loan

5.1 Property Value Matters Most

Lenders care about the current or after-repair value (ARV) of the property

5.2 Down Payment Requirements

You’ll typically need to bring 25%–40% of the property value to the table

5.3 Credit Score Still Counts (But Less)

Some lenders have minimum requirements (e.g., 600+), but it’s not the deciding factor

5.4 Clear Exit Strategy

Lenders want to see how you’ll repay the loan—sale, refi, or rental income

Chapter 6: Where to Find Hard Money Lenders

6.1 Local Hard Money Lenders

Real estate investor meetups, referrals, and real estate attorney recommendations

6.2 National Hard Money Companies

- LendingHome

- Kiavi

- Lima One Capital

- RCN Capital

6.3 Private Investors

Friends, family, or high-net-worth individuals offering short-term private lending

Chapter 7: Hard Money vs. Other Loan Types

7.1 Hard Money vs. Conventional Loan

| Feature | Hard Money | Conventional Loan |

|---|---|---|

| Approval Speed | Days | Weeks to months |

| Credit Score | Less important | Very important |

| Interest Rate | Higher (8%–15%+) | Lower (4%–8%) |

| Term | Short (6–36 months) | Long (15–30 years) |

| Use Case | Investment properties | Owner-occupied homes |

7.2 Hard Money vs. Private Money

- Hard money is more formal, through established lenders

- Private money is informal and from personal contacts

7.3 Hard Money vs. Bridge Loan

Bridge loans are a type of short-term financing like hard money, but often from banks and used for different purposes (like buying a new home before selling your old one)

Chapter 8: Costs and Fees Breakdown

8.1 Interest Rates

- Range from 8% to 15%

- Paid monthly (interest-only in many cases)

8.2 Points and Origination Fees

- 1–5% of loan amount

- Paid upfront at closing

8.3 Other Fees

- Appraisal fees

- Underwriting fees

- Legal/document fees

8.4 Example Calculation

For a $200,000 loan:

- Interest rate: 10%

- Term: 12 months

- Points: 3% = $6,000 upfront

- Monthly interest: $1,666

- Total interest over 12 months = $20,000

- Total cost = $26,000

Chapter 9: Using a Hard Money Loan Effectively

9.1 Ideal Projects

- Distressed property flips

- Time-sensitive deals

- BRRRR projects needing rehab funds fast

9.2 Planning Your Exit

Have your strategy ready before you apply—especially if you plan to refinance or sell quickly

9.3 Budget for Fees

Factor in all upfront costs and interest when analyzing your deal

Chapter 10: Risks and How to Avoid Them

10.1 Defaulting on the Loan

- Could lose the property

- Damaged credit and reputation

10.2 Overestimating After-Repair Value

- Leads to smaller loan amounts or project losses

10.3 Underestimating Rehab Costs

- Project delays and cash flow issues

10.4 Not Having a Backup Exit Plan

- Always have Plan B in case your primary strategy fails

Conclusion

Hard money loans can be an excellent tool for real estate investors who need speed, flexibility, and asset-based lending—but they’re not for everyone. With higher interest rates, short terms, and significant fees, these loans require strategic planning and sound project analysis.

If you’re considering a hard money loan, be sure to compare lenders, understand your exit strategy, and budget accordingly. Used wisely, hard money financing can help you scale your real estate investments faster and more efficiently than traditional financing ever could.