What is a Pinless Debit Card Explained:

What is a Pinless Debit Card allows consumers to make debit transactions without entering a personal identification number (PIN) at the point of sale. This type of payment functions similarly to a credit card transaction, enabling quicker and more convenient checkouts while still using funds directly from a bank account.

Consumers typically swipe or tap their debit card as usual, but instead of authenticating with a PIN, the transaction is processed through specific networks that support pinless routing. These transactions often apply to smaller purchases and aim to reduce friction during checkout without compromising payment security.

Merchants benefit from faster transactions and improved customer experiences, while cardholders enjoy the simplicity of a PIN-free payment process. Understanding how pinless debit works helps both merchants and shoppers navigate the evolving payment landscape.

Understanding Pinless Debit Cards

Pinless debit cards allow users to make electronic debit payments without entering a personal identification number (PIN). This process speeds up transactions while still using the card’s funds directly from a bank account. The technology behind pinless transactions differs slightly from traditional debit processing but maintains secure authorization methods.

Definition of Pinless Debit Cards

A pinless debit card enables payments that do not require a customer to input a PIN at the point of sale. Unlike typical debit cards that need a PIN for card-present ATM or checkout use, pinless debit transactions are authorized through alternative verification, such as signatures or network routing protocols.

These cards function as electronic debit cards, linking purchases directly to a consumer’s bank account. They are common in the U.S. through networks like Visa, Mastercard, and regional systems such as Shazam and Pulse. Pinless debit is often used for lower-value purchases to reduce friction in the checkout process.

How Pinless Debit Transactions Work

When a pinless debit transaction takes place, the payment is routed through specific debit networks designed to process transactions without PIN entry. Merchants send the purchase request through networks that recognize the payment as debit but do not prompt for PIN verification.

Instead of a PIN, transactions rely on authorization codes, transaction limits, or cardholder signatures. This method is faster and can be more convenient for merchants, especially for small-value sales where entering a PIN or obtaining a signature may be impractical.

The system still verifies the availability of funds and conducts fraud checks within the electronic debit infrastructure, ensuring security despite the absence of a PIN.

Differences Between Pinless and PIN Debit Cards

The main difference lies in the requirement for a PIN during the transaction. PIN debit cards require users to enter their PIN at checkout, which validates the cardholder’s identity directly with their bank. Pinless debit cards bypass that step, often using signature or no signature for approval.

PIN debit transactions usually route through major networks like Shazam or NYCE requiring secure PIN verification. Pinless debit payments might route through major card networks (Visa or Mastercard) or regional networks allowing PIN bypass.

Another key difference is merchant cost. Pinless debit transactions may have different fee structures, sometimes offering merchants lower processing fees compared to PIN debit. However, this varies by network and merchant agreements.

| Feature | PIN Debit | Pinless Debit |

|---|---|---|

| Requires PIN at checkout | Yes | No |

| Authentication method | PIN entry | Signature or automatic approval |

| Routing network | Regional debit networks (e.g., Shazam, Pulse) | Card networks & regional networks |

| Typical fees for merchants | Higher | Often lower or comparable |

Key Features and Benefits of Pinless Debit Cards

Pinless debit cards eliminate the need for a PIN during transactions, streamlining payments without sacrificing essential security measures. They offer specific benefits over traditional debit cards, balancing convenience, security, and cost-effectiveness for both merchants and cardholders.

Advantages Over Traditional Debit Cards

Pinless debit transactions function more like credit card payments by not requiring a PIN, which can reduce wait times at checkout. This can lead to faster transaction processing and reduced friction for customers.

Merchants benefit from potentially lower processing fees, especially when payments are routed through regional networks instead of major card companies. This routing can improve success rates and lower costs compared to traditional debit card transactions.

Additionally, pinless debit transactions are considered cashless account receivables, as funds are debited directly from the cardholder’s bank. This differs from cash or credit, providing merchants with a reliable form of payment with lower risk of chargebacks compared to credit transactions.

Security Considerations

Although pinless debit cards don’t require a PIN, they still rely on other security protocols such as encryption and tokenization to protect sensitive information. Merchants and cardholders should ensure these measures are in place to prevent unauthorized use.

Proper security also includes monitoring account activity for suspicious transactions and enabling alerts. Cardholders should treat pinless debit cards like traditional debit cards by regularly reviewing statements and reporting anomalies immediately.

Despite no PIN entry, these transactions use secure payment networks and comply with industry standards to minimize fraud risk. This helps maintain confidence in the payment method while allowing ease of use.

Convenience of Use

Pinless debit cards simplify payment by removing the PIN step, thereby speeding up purchases at point of sale or online. This makes them especially useful for recurring payments and subscriptions where repeated PIN entry would be cumbersome.

Use with contactless payments and QR codes further enhances convenience, allowing quick, secure transactions without physical card handling. Cardholders don’t need to remember or input a PIN, making the experience smoother.

For merchants, enabling pinless debit acceptance broadens customer options and can increase sales conversion by reducing checkout friction. This convenience aligns well with modern consumer preferences for fast and easy payment methods.

Typical Use Cases for Pinless Debit Transactions

Pinless debit transactions allow fast, secure payments without requiring a PIN entry. This method fits well in situations where convenience and speed are priorities, especially in both physical and digital payment environments.

Everyday Purchases

Pinless debit is frequently used for everyday retail purchases. It enables consumers to buy items quickly without pausing to enter a PIN, which speeds up checkout in grocery stores, gas stations, and convenience shops.

Merchants benefit from reduced friction at checkout and lower operational costs in fast-paced environments. This method also suits small-ticket transactions where customers prefer hassle-free payments. Many regional networks support these transactions, offering merchants competitive processing fees.

Bill Payments

Consumers often use pinless debit for recurring payments such as orthodontist payment plans or root canal dentist Seattle payment plans. These transactions are generally set up through automatic payment pools.

Pinless debit facilitates convenient monthly bill payments without the need for users to re-enter details or PINs each time. It supports reliable timely payments and improves cash flow management for service providers and patients alike.

Online and Mobile Transactions

Pinless debit transactions function similarly to credit card payments in online or mobile environments. They allow users to complete purchases without entering a PIN, making them suitable for e-commerce and app-based shopping.

This setup can include Supernova payment options that streamline customer experiences. However, pinless debit cannot be used for ATM cash withdrawals, such as withdrawing cash from an HSA debit card, where PIN authentication remains mandatory.

Pinless Debit Card Processing and Networks

Pinless debit card transactions bypass the need for a personal identification number (PIN), allowing faster checkout while relying on specific networks for routing and settlement. Merchants benefit from lower processing fees and vendors must understand the involved networks and timelines for transaction completion.

Role of Card Networks

Pinless debit transactions use networks distinct from traditional debit card routes. Instead of routing solely through Visa or Mastercard, these payments often go through regional EFT networks like Star, Pulse, NYCE, or Shazam Debit Card networks.

These networks operate the behind-the-scenes authorization and clearing processes. Because they are designed for non-PIN debit transactions, they can handle transactions more efficiently and at lower costs for merchants. Pinless debit routing allows payment to be directed through these networks regardless of the card’s brand.

This method reduces fees associated with credit card network routes and helps facilitate more seamless payment experiences, especially for businesses looking to speed up checkouts without compromising security.

Merchant Acceptance

Merchants processing debit payments increasingly adopt pinless debit acceptance to gain cost and speed advantages. Accepting pinless debit involves working with payment providers and POS systems that support routing payments through regional networks like Shazam.

Merchants must verify their systems can interface properly with networks like Star or Pulse to ensure transactions authorize without PIN entry. Post-2023 regulatory clarifications have made pinless debit more attractive by prohibiting issuers from adding fees that discourage its use.

By integrating pinless debit, merchants often see faster transaction approval and reduced chargeback risks, improving both customer experience and operational efficiency.

Transaction Settlement Times

Settlement for pinless debit card transactions typically follows schedules managed by the specific EFT network used. Networks such as Shazam or NYCE settle funds quicker than some credit card networks due to streamlined processing for debit types.

These EFT networks often settle transactions within one to two business days. This speed ensures merchants receive funds promptly while minimizing the hold periods common with credit card settlements.

Pinless debit’s faster settlement supports better cash flow management, especially useful for small to medium businesses that operate on tighter margins and require quicker access to sales proceeds.

Security, Risks, and Fraud Prevention

PINless debit cards provide convenience by allowing transactions without a PIN, but this also changes how risks and security measures apply. There are increased chances of unauthorized use, especially when card details are compromised. Proper security practices and monitoring are essential to reduce potential fraud and financial loss.

Fraud Risks in Pinless Transactions

PINless debit transactions lack the additional verification of a PIN or signature. This absence makes them more vulnerable to fraud, including unauthorized purchases made without physical possession of the card.

Fraudsters may use stolen card information obtained through data breaches, card skimming, or online theft. They do not need the card itself, raising concerns about how someone can use a debit card without having it physically.

Chip malfunction on a debit card does not typically increase fraud risk on PINless transactions but can cause declined transactions, prompting consumers to attempt alternative payment methods, potentially exposing more data.

Merchants and banks face financial exposure due to unauthorized transactions. They often implement fraud detection systems that analyze spending patterns and transaction amounts to flag suspicious activity immediately.

Best Practices for Cardholders

Cardholders should regularly monitor their account activity to detect unrecognized transactions early. Setting up real-time alerts for purchases can provide immediate notification of any unusual spending.

Using strong, unique passwords for online banking and avoiding public Wi-Fi during transactions reduces the chance of interception. They should also report lost or stolen cards promptly to minimize unauthorized use.

Proper security measures include enabling two-factor authentication if available and never sharing card details online or over the phone without verification.

If chip malfunction occurs, cardholders should contact their financial institution to request a replacement and avoid using a card that may expose account information through repeated attempts at malfunctioning terminals.

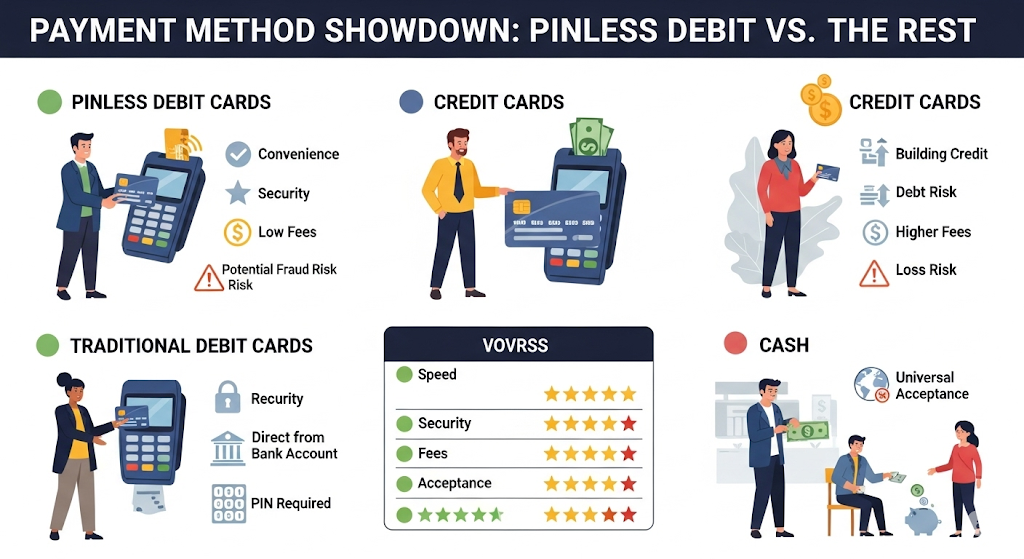

Comparing Pinless Debit Cards With Other Payment Methods

Pinless debit cards differ notably from other payment options in terms of security, cost, and transaction process. Understanding the nuances helps businesses and consumers decide when to use them effectively.

Credit Cards vs. Pinless Debit Cards

Credit cards allow users to borrow funds up to a credit limit and typically require a signature or PIN for verification. They often come with rewards but can carry higher processing fees for merchants, such as businesses like credit unions offering business credit cards. Pinless debit cards, on the other hand, use funds directly from a checking account without requiring a PIN or signature. This lowers transaction friction but may have fewer fraud protections compared to credit cards.

For merchants, pinless debit may reduce costs since it often bypasses some credit card processing fees. However, credit card abuse charges and declines—both soft and hard—remain important risk factors primarily associated with credit card transactions, not pinless debit. Customers paying for elective procedures like LASIK often prefer credit cards for rewards or financing, whereas pinless debit suits everyday purchases with a lower risk profile.

ATM Debit vs. Pinless Debit

An ATM debit transaction requires a Personal Identification Number (PIN) at the point of sale, adding a layer of security through cardholder verification. These transactions usually route through major debit networks and may involve higher interchange fees for merchants.

Pinless debit does not require entering a PIN and processes transactions much like credit cards, using signature or zero-PIN authorization depending on purchase size. This can speed up checkout and increase approval rates but reduces the security tied to PIN verification.

Consumers using ATM debit for routine withdrawals appreciate the security and control it offers, while pinless debit is often preferred for low-value or routine retail payments, benefiting from lower fees and faster checkouts.

Mobile Wallets and Alternative Payments

Mobile wallets store credit, debit, or prepaid card information, allowing contactless payments via smartphones or smartwatches. They provide convenience and encryption, reducing physical card misuse risks.

Pinless debit cards can be part of these wallets, but not all pinless debit transactions occur this way. Compared to alternative payments, pinless debit is straightforward, using traditional card networks with lower processing costs, but lacks the multi-factor protections mobile wallets offer.

For merchants like AAMCO with credit card terminals, integrating mobile wallets expands payment options. However, pinless debit remains a cost-effective choice for many small to medium transactions, complementing mobile and alternative payment solutions.

Limitations and Considerations

PINless debit cards provide faster checkout experiences but come with specific boundaries that impact how and where they are used. These include both merchant acceptance and transaction value limits, which can affect usability and cost-effectiveness for businesses and consumers.

Merchant and Geographic Limitations

Not all merchants accept PINless debit transactions. Some prefer traditional PIN-based transactions for security reasons or due to incompatible payment systems. For example, smaller or regional merchants may lack the infrastructure to process pinless debit payments.

Geographic constraints also play a role. Pinless debit card usage can be limited internationally, particularly outside networks supporting routing flexibility. While the Bank of Bhutan’s international debit card features might allow global transactions, pinless debit routing may not always be available in every country or merchant location.

Merchants must verify their payment processors support PINless debit transactions. Otherwise, they risk losing potential cost savings and customer convenience these transactions offer. This limitation is especially relevant for businesses expanding into diverse markets.

Transaction Amount Restrictions

Many PINless debit transactions have limits on the maximum amount permitted without a PIN. These limits vary by payment network and issuing bank, often capping at low to moderate spending levels.

Such limits are designed to reduce fraud risk since PINless transactions lack the additional layer of personal identification. Large purchases, even when using a debit card, often require entering a PIN to complete the transaction.

For those wondering, “can I use my business debit card for personal use,” handling large transactions under PINless debit rules may complicate matters if spending exceeds these limits or involves strict business account policies. Users should understand their card’s terms to avoid declined payments or unexpected fees.

Trends and Future of Pinless Debit Cards

Pinless debit cards are seeing increasing use due to their ability to simplify transactions and reduce friction at checkout. Innovations in payment routing and growing acceptance across merchant platforms drive their expanding role in retail and online payments.

Adoption and Market Growth

Pinless debit transactions are growing quickly, especially in the U.S. merchant space. Debit cards account for roughly half of eCommerce volume, and more merchants now have routing options for these transactions, which encourages broader adoption.

Merchants value pinless debit for lower processing friction and potential cost benefits versus traditional debit methods. The payment networks Visa and Mastercard, along with smaller regional networks, are expanding pinless debit solutions to improve transaction speed and approval rates.

This growth also responds to consumer demand for faster checkout. Merchants offering pinless debit improve the user experience by allowing purchases without PIN entry or signature, making it a favored method for low to mid-value transactions.

Emerging Technologies

Advances in payment technology are shaping pinless debit’s future. Improved routing systems enable merchants to select networks that optimize costs and acceptance rates, increasing competitiveness among providers.

Tokenization and biometric authentication technologies are also enhancing security for pinless debit without reverting to PIN entry. These technologies allow safer in-person and card-not-present transactions by confirming the cardholder’s identity discreetly.

Additionally, integration with mobile wallets and contactless payments extends pinless debit’s convenience for consumers. This supports evolving behaviors like using smartphones for payments, including buying proxies with credit cards, where similar transaction methods reduce the need for traditional PIN verification.